A SIP Calculator with Inflation is an advanced online financial planning tool that estimates the future value of your Systematic Investment Plan (SIP) investments while adjusting for the erosive impact of inflation. Unlike basic SIP calculators that only show nominal (face-value) growth, this tool reveals the real purchasing power of your accumulated corpus in today’s rupees.

What Exactly is a SIP Calculator with Inflation?

A Systematic Investment Plan (SIP) lets you invest a fixed amount regularly (usually monthly) in mutual funds, benefiting from rupee cost averaging and the power of compounding. A standard SIP calculator computes the total corpus based on your monthly investment, expected annual return rate, and tenure. It answers: “If I invest ₹X every month for Y years at Z% return, how much will I have?”

A SIP Calculator with Inflation takes this further by incorporating an inflation rate (typically 5-7% in India). It calculates two key figures:

- Nominal Future Value: The raw amount your SIP will grow to.

- Inflation-Adjusted (Real) Value: What that future amount will actually be worth in today’s purchasing power after accounting for rising prices.

This adjustment uses the concept of real returns: roughly, Real Return ≈ Expected Return – Inflation Rate. Over long periods, inflation significantly reduces what your money can buy— a ₹1 crore corpus in 20 years might feel like only ₹50-60 lakh in today’s terms at 6% inflation.

Why does this matter? Inflation in India has historically averaged around 6% (CPI-based), though it fluctuates. Essentials like education, healthcare, and weddings often inflate faster (8-12%). Planning without it leads to underestimating required investments, resulting in shortfalls for major life goals.

This tool helps you answer realistic questions like:

- Will my current SIP actually fund my child’s education or my retirement dream lifestyle?

- How much more do I need to invest today to maintain my future purchasing power?

- What step-up rate in my SIP is needed to beat inflation comfortably?

How is a SIP Calculator with Inflation Different from Other Tools?

Many investors use generic calculators, but they often miss the full picture. Here’s a clear comparison:

| Feature | Basic SIP Calculator | Step-Up SIP Calculator | SIP Calculator with Inflation | Goal-Based SIP Calculator |

| Monthly Investment | Fixed amount | Increasing annually | Fixed or variable | Backward calculation for target goal |

| Inflation Adjustment | No | Sometimes optional | Yes — core feature | Often includes it |

| Shows Nominal Value | Yes | Yes | Yes | Yes |

| Shows Real Purchasing Power | No | Partial | Yes — detailed | Yes |

| Best For | Quick estimates | Income growth alignment | Realistic long-term planning | Specific targets (e.g., ₹5 Cr retirement) |

| Realism Level | Low (overly optimistic) | Medium | High | Highest |

Key Differences Explained:

- Vs. Regular SIP Calculator: Basic tools ignore inflation, showing impressive numbers that look great on paper but disappoint in reality. The inflation-adjusted version prevents “illusion of wealth” by displaying both nominal and real values side-by-side.

- Vs. Step-Up SIP Calculator: Step-up tools assume your investment amount rises (e.g., 10% annually with salary hikes). Adding inflation makes it even more powerful, showing if your stepped-up contributions truly preserve purchasing power.

- Vs. Lumpsum or FD Calculators: These are static; SIP with inflation accounts for regular investing and rupee cost averaging while adjusting for time-value erosion.

- Vs. Retirement or Education Calculators: Many goal calculators now embed inflation, but a dedicated SIP + Inflation tool offers flexibility for any goal without locking into one scenario.

The biggest differentiator is psychological and behavioral: Seeing the inflation-adjusted figure motivates investors to increase SIPs, choose higher-return equity funds, or add step-ups—actions that basic tools don’t prompt as strongly.

Who Should Use a SIP Calculator with Inflation?

This tool is ideal for almost every disciplined investor in India, but especially valuable for:

- Young Professionals (25-35 years): Starting early gives time for compounding, but inflation over 20-30 years is massive. Use it to set aggressive yet realistic SIPs for wealth creation.

- Mid-Career Individuals (35-50 years): With rising income but also rising expenses (kids’ education, home loans), it helps balance current lifestyle with future security. Perfect for reviewing if existing SIPs are on track.

- Parents Planning Child’s Future: Education and marriage costs inflate rapidly (often 10%+). This calculator shows exactly how much SIP is needed today for a goal 15 years away.

- Pre-Retirees (50+ years): Assess if your corpus will sustain retirement expenses that rise with inflation. It helps decide safe withdrawal rates and debt vs. equity allocation.

- First-Time Mutual Fund Investors: It builds confidence by showing realistic scenarios rather than hype.

- Anyone with Long-Term Goals: Retirement, buying a house, dream vacation, or financial independence (FIRE). If your horizon is 5+ years, inflation matters.

Not ideal for: Ultra-short-term parking (under 1-2 years) where inflation impact is negligible, or pure debt investors expecting returns below inflation.

In India’s context, with volatile inflation, rupee depreciation, and rising aspirations, this tool is essential for anyone serious about beating the “inflation tax.”

Key Benefits of Using a SIP Calculator with Inflation

Using this tool delivers tangible and intangible advantages:

- Realistic Goal Setting: Avoid under-saving. A nominal ₹2 crore corpus might only buy what ₹80 lakh does today prompting you to act now.

- Better Investment Decisions: Compare different return assumptions (equity 12-15%, hybrid 10-12%, debt 7-8%) against inflation to choose the right fund category.

- Motivation for Step-Ups: Visualizing how increasing your SIP by 10-15% annually dramatically improves real returns encourages habit formation.

- Risk Awareness: Understand volatility—higher equity returns come with ups and downs, but they are often necessary to outpace inflation.

- Tax and Expense Planning: Some advanced versions factor post-tax real returns, helping optimize for LTCG tax on equity funds.

- Behavioral Finance Edge: It counters optimism bias and present bias (preferring spending now over saving). Seeing “real value” graphs fosters discipline.

- Portfolio Review Tool: Run scenarios for your existing SIPs to decide whether to continue, increase, or reallocate.

- Family Financial Discussions: Easy-to-understand outputs (charts, tables) make conversations with spouse or parents about money goals productive.

- Long-Term Wealth Preservation: Helps ensure your money works harder than inflation, preserving lifestyle across generations.

Studies and investor experiences show that those who plan with inflation in mind accumulate significantly higher real wealth over decades.

How Does Inflation Impact Your SIP Returns? (With Examples)

Inflation quietly eats into returns. Suppose you invest ₹10,000 monthly for 20 years at 12% expected return:

- Without Inflation Adjustment: Corpus ≈ ₹1.0+ crore (impressive!).

- With 6% Inflation: Real value in today’s terms ≈ ₹50-60 lakh (still good, but a reality check).

If inflation averages 7%, the real corpus drops further. Equity SIPs historically deliver 12-15% CAGR over long periods in India, offering a real return of 6-9% after inflation—enough to build meaningful wealth if started early and maintained.

Higher inflation scenarios (e.g., during economic stress) highlight the need for diversified, growth-oriented investments. Conversely, low-inflation periods reward even moderate returns.

Pro Tip: Use historical Indian inflation data (around 5.5-6.5% long-term average) but stress-test with 4%, 6%, and 8% to prepare for different economic cycles.

Step-by-Step Guide: How to Use a SIP Calculator with Inflation

Most online tools (available on mutual fund platforms, banks, or independent sites) follow a similar simple interface. Here’s a detailed walkthrough:

Access the Tool

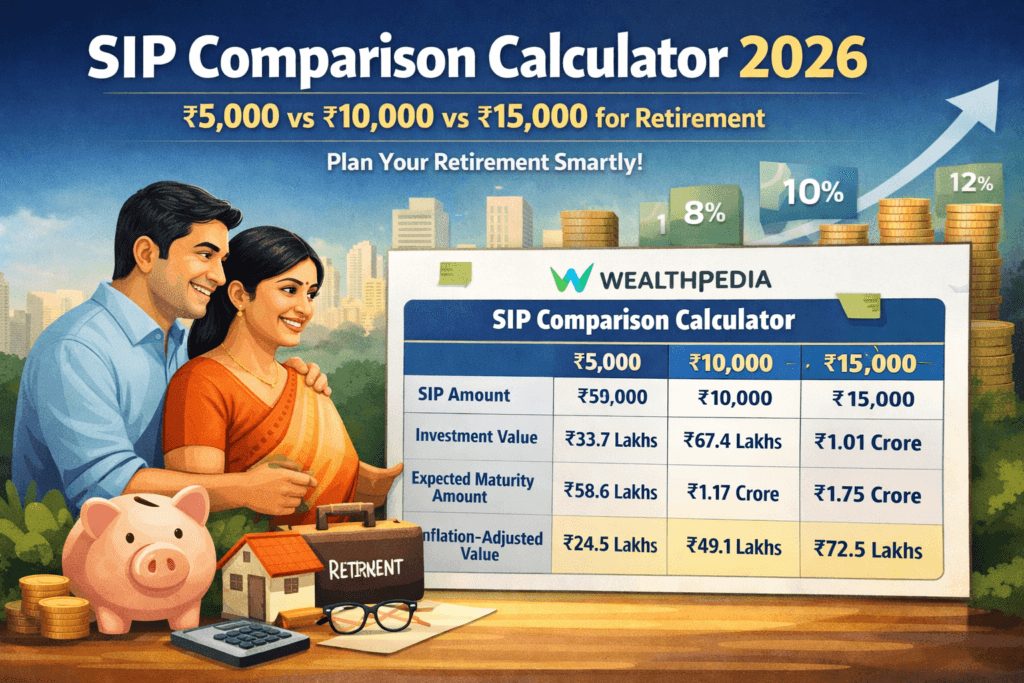

Here is the direct link for SIP Comparison Calculator.

Enter Monthly SIP Amount

Start with your affordable amount (e.g., ₹5,000, ₹10,000, or ₹25,000). Many tools let you use sliders for quick adjustments. Begin conservatively and increase later.

Input Expected Annual Return Rate

Equity funds: 12-15% (long-term historical).

Hybrid/Balanced: 10-12%.

Debt: 6-8%. Be realistic—past performance isn’t a guarantee. Use conservative estimates (e.g., 10-12%) for safety.

Specify Investment Tenure (in Years)

Enter the horizon: 5, 10, 15, 20, or 30 years. Longer periods amplify both compounding and inflation effects.

Enter Expected Inflation Rate

Default/Realistic: 5-7% for India.

Conservative: 4%.

Aggressive test: 8%. Some calculators auto-suggest based on current CPI.

Optional Inputs (Advanced Tools)

Step-up percentage (annual increase in SIP, e.g., 10%).

Lump sum initial investment.

Tax rate or post-tax returns.

Frequency (monthly/quarterly).

See The Result

The tool instantly shows the SIP’s targeted corpus at the given return percentage. You can tweak the return % or SIP amount as per your wish.

What Results You’ll See:

Total Amount Invested.

Expected Nominal Corpus.

Estimated Gains.

Inflation-Adjusted Corpus (real value).

Analyze and Iterate

Play with variables: Increase SIP by ₹2,000 and see impact.

Test different returns and inflation rates.

Compare scenarios: “What if I start today vs. delay by 2 years?”

Take Action

Export results, set reminders to review annually, and start or increase your SIP via your AMC/app. Link it to a specific goal for better commitment.

Advanced Tips for Maximizing the Tool

- Combine with Step-Up: Aim for 10-15% annual step-up to match salary growth and inflation.

- Goal-Based Planning: Work backwards—input desired future real amount and solve for required SIP.

- Diversify Assumptions: Run optimistic, base, and pessimistic cases.

- Review with Actuals: After investing, compare real performance against calculator projections and rebalance.

- Integrate with Overall Portfolio: Use alongside retirement, insurance, and emergency fund calculators.

- Mobile Apps: Many broker apps now offer in-built versions with charts.

For even better accuracy, consider tools that also factor taxes (equity SIPs enjoy favorable LTCG treatment after 1 year).

Frequently Asked Questions (FAQs) about SIP Calculator with Inflation

What is the ideal inflation rate to use in India?

Use 5-7% as a baseline. For specific goals like education or healthcare, consider 8-10%. Always stress-test higher rates.

Can this calculator predict exact future returns?

No. It provides estimates based on assumed rates. Actual returns depend on market performance, fund selection, and economic factors. Use it for planning, not guarantees.

Is SIP with inflation adjustment only for equity funds?

No. It’s useful for any SIP (equity, debt, hybrid). However, debt SIPs may struggle to beat high inflation, so the tool often highlights the need for growth assets in long-term plans.

How accurate is the inflation adjustment?

It uses standard financial formulas for future value and present value discounting. Accuracy depends on how close your assumptions (return & inflation) are to reality. It’s directionally very helpful.

Should I increase my SIP every year?

Yes—most experts recommend step-up SIPs. The calculator helps quantify how much (e.g., 10%) to stay ahead of inflation and lifestyle creep.

Does it account for taxes?

Basic versions don’t; advanced ones might. For equity mutual funds, LTCG tax above ₹1.25 lakh (at 12.5%) has minimal impact on long-term SIPs. Factor it manually for precision.

What if inflation is higher than expected?

Your real returns shrink. Mitigate by increasing SIP amount, extending tenure, or shifting to higher-growth assets. Regular reviews help.

Is there any cost to using these calculators?

Almost all are completely free on platforms like Wealthpdia, Groww, Zerodha, Dhan, or bank sites.

How often should I use this tool?

At least once a year, or whenever your income changes, goals shift, or inflation spikes noticeably.

Can beginners use it effectively?

Absolutely. The interface is user-friendly with sliders and instant visuals. Start with default values and learn by tweaking.

Does it work for international investments or NRI SIPs?

Some tools do, but adjust for currency inflation and different return expectations. For rupee-based SIPs in Indian funds, domestic tools suffice.

What return rate is realistic for SIPs?

Long-term equity SIPs in India have delivered 12-15% CAGR, but assume 10-12% for conservative planning to account for volatility.

Conclusion: Make Informed Investing a Habit

A SIP Calculator with Inflation transforms vague saving into precise, goal-oriented wealth building. It bridges the gap between optimistic projections and real-life purchasing power, empowering you to make smarter decisions today for a secure tomorrow.

In an economy where inflation is a constant companion, ignoring it is costly. By regularly using this tool, you gain clarity, stay motivated, and align your investments with actual life needs—whether it’s funding higher education, enjoying a comfortable retirement, or achieving financial freedom.

Actionable Next Step: Open a SIP Calculator with Inflation today. Input your current plan, then experiment with increased SIPs or step-ups. You’ll likely discover you need to invest a bit more or start sooner than you thought—but the power of compounding will reward you handsomely over time.

Start small, stay consistent, review annually, and let time and discipline work in your favor. Your future self (and family) will thank you for planning with inflation in mind.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up