Financial Health Score Calculator India

In today’s fast-paced world, tracking individual mutual fund returns, SIP performance, or even your CIBIL score is common, but very few people truly understand the overall strength of their financial life. Wealthpedia’s Financial Health Score changes that by delivering a single, easy-to-understand number from 0 to 100 that summarizes your entire financial picture — income stability, spending habits, savings discipline, debt burden, emergency preparedness, investments, net worth, and risk protection through insurance.

Think of it as a “credit score for your whole financial life”, not just borrowing ability. This tool is especially relevant for Indian users dealing with unique challenges like high EMIs on home or car loans, volatile business income, rising lifestyle expenses in cities like Ahmedabad, Mumbai, or Bangalore, and the need to balance short-term goals with long-term wealth building for retirement or children’s education.

By the end, you’ll know exactly how to leverage this free or accessible tool to gain clarity, track progress, and make smarter financial decisions.

What Is the Financial Health Score by Wealthpedia?

The Financial Health Score is an interactive online tool available on Wealthpedia.in that evaluates your personal finances holistically and outputs a score between 0 and 100. A higher score indicates stronger overall financial well-being, while lower scores highlight areas needing immediate attention.

Unlike fragmented metrics — such as tracking only your savings rate in a budgeting app or net worth in a spreadsheet — this tool integrates multiple pillars of personal finance into one actionable metric. It acts as a financial mirror, revealing not just where you stand today but also which levers (like reducing debt or boosting savings) will deliver the biggest improvements.

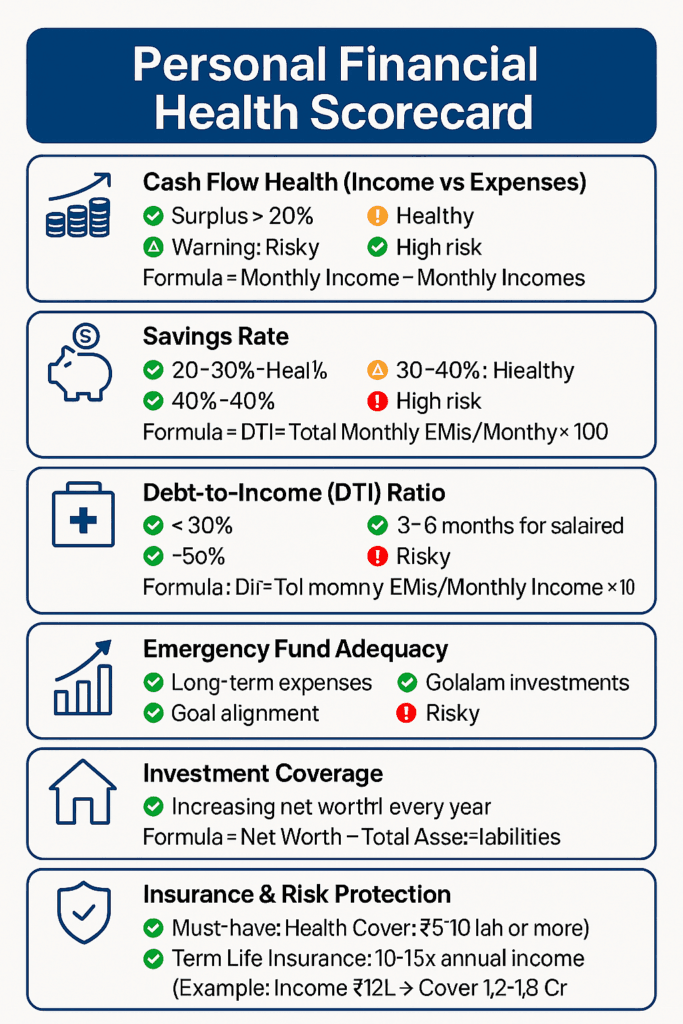

Core components assessed include:

- Cash flow health: Monthly income versus expenses (surplus or deficit).

- Savings rate: Percentage of income saved or invested.

- Debt-to-income (DTI) ratio: How much of your income goes toward debt repayments.

- Emergency fund adequacy: Liquid savings covering 3–6 months of expenses.

- Investment coverage: Consistency, diversification, and goal alignment of investments (mutual funds, stocks, PPF, EPF, etc.).

- Net worth position: Assets minus liabilities.

- Insurance and risk protection: Adequacy of health and term life insurance to prevent financial shocks.

The tool uses a multi-factor scoring model based on industry standards and real-life calculations employed by SEBI-registered investment advisors. It applies weighted scoring similar to illustrative breakdowns: Savings Rate (~25%), Debt Ratio (~20%), Emergency Fund (~15%), Investments (~15%), Cash Flow (~10%), Net Worth (~10%), and Insurance (~5%). Each factor is scored individually before combining into the final 0–100 result.

Benchmarks provided on the page help contextualize your score:

- Savings rate: 10–20% (average), 20–35% (good), 35%+ (excellent).

- DTI: Below 30% (healthy), 30–50% (risky), above 50% (dangerous).

- Emergency fund: Minimum 3 months, ideally 6 months of expenses.

A score above 70 is generally good, while 80+ is excellent. The output typically includes the overall score, a breakdown of strengths and weaknesses, and personalized suggestions for improvement.

This makes the Wealthpedia Financial Health Score more than a simple quiz — it’s a practical diagnostic tool tailored for the Indian context, where factors like joint family expenses, gold investments, or festival spending can skew traditional Western models.

How Is Wealthpedia’s Financial Health Score Different from Other Tools?

Many financial tools exist, but most are narrow in scope or survey-based rather than data-driven with actual numbers. Here’s how Wealthpedia’s tool stands out:

- Holistic vs. Fragmented Metrics:

- Traditional tools often focus on one area: credit score (repayment history), net worth calculators (assets – liabilities only), or budgeting apps (expenses tracking). Wealthpedia combines seven key pillars into one score, addressing Indian realities like heavy reliance on EMIs, inconsistent freelance/business income, and the importance of insurance amid rising healthcare costs.

- Quantitative Data Input vs. Subjective Surveys:

- Many global or Indian tools or simple 8-question quizzes from banks) rely on self-reported feelings or multiple-choice answers like “Do you spend less than you earn?” or “Do you plan ahead?” These are quick but less precise because they depend on perception.

- Wealthpedia requires specific numerical inputs (monthly income, expenses, total savings, investments, debt, emergency fund, insurance details). This leads to more objective, personalized calculations grounded in your actual finances, similar to how SEBI advisors analyze client portfolios.

- Actionable Recommendations vs. Generic Scores:

- Some calculators give a number and broad categories (vulnerable/coping/healthy). Wealthpedia goes further by identifying weak areas and offering targeted suggestions, such as “Build emergency fund first” or “Reduce high-interest debt.

- India-Specific Tailoring:

- Existing tools with different benchmarks for spending, borrowing, and planning. Indian alternatives like some bank “financial fitness” quizzes or apps may exist but often feel more promotional or less comprehensive. Wealthpedia emphasizes local pain points: high salary but poor savings discipline, strong investments without emergency buffers, or heavy home loans impacting cash flow. It avoids over-relying on income level alone, stressing financial discipline instead.

- Simplicity and Tracking:

- Unlike complex financial planning software used by advisors, this is initially free/accessible for individuals. It encourages re-checking every 6–12 months to track progress, turning it into a habit-building tool rather than a one-off assessment.

In short, while credit scores tell lenders if you repay loans well, and net worth shows your balance sheet snapshot, Wealthpedia’s Financial Health Score gives a dynamic, forward-looking health check of your financial ecosystem. It’s not a replacement for professional advice but an excellent starting point or ongoing monitor.

Who Should Use the Wealthpedia Financial Health Score Tool?

This tool is versatile and beneficial for a wide range of users, particularly in India:

- Salaried Professionals (20s–40s): Those with steady income but rising expenses (rent, EMIs, lifestyle inflation) in metros or Tier-1/2 cities. It helps assess if you’re truly building wealth or just maintaining status.

- Business Owners and Freelancers: With irregular income, the tool highlights cash flow vulnerabilities and the need for stronger emergency funds or insurance.

- Young Earners and Millennials/Gen Z: Starting careers, managing first salaries, student loans (if any), or early investments. It prevents common mistakes like overspending on gadgets or travel without savings discipline.

- Families and Married Couples: Planning for children’s education, weddings, or parental healthcare. It evaluates joint finances, insurance adequacy, and goal alignment.

- FIRE Aspirants (Financial Independence, Retire Early): Those aiming to retire early need to monitor savings rate, investment consistency, and debt reduction rigorously.

- Anyone Feeling Financially Overwhelmed: If you track returns but still feel anxious about money, or wonder “Can I afford a home/car?” or “Am I on track for retirement?”, this provides clarity without judgment.

It’s especially useful for beginners who find personal finance intimidating — the tool simplifies complexity into one number. Even experienced investors benefit from periodic checks to ensure balance across all areas, not just portfolio performance.

People in locations like Ahmedabad, Gujarat (with its mix of business and salaried communities), or other growing Indian cities will find it relevant due to local cost-of-living pressures and investment options like PPF, NPS, or mutual funds.

Avoid relying solely on the score for major decisions like large loans or investments — pair it with advice from a certified financial planner.

Key Benefits of Using the Wealthpedia Financial Health Score

- Instant Clarity and Awareness:

- Replaces vague feelings (“I think I’m okay with money”) with a concrete number and breakdown. Many users discover hidden issues, like insufficient emergency funds despite good investments.

- Prioritization of Improvements:

- By highlighting weak pillars (e.g., high DTI or low savings rate), it shows where effort yields the highest ROI on your time and money. Paying off high-interest credit card debt might boost your score more than adding another SIP.

- Better Decision-Making:

- Answers practical questions: “Should I take that new loan?”, “Is my savings rate sufficient for FIRE?”, or “Do I need more term insurance?” It supports goal-based planning for home purchase, marriage, education, or retirement.

- Progress Tracking Over Time:

- Reassess every 6–12 months. Major positive changes (debt repayment, emergency fund buildup, income increase with controlled expenses) can quickly lift your score, providing motivation like a fitness tracker for finances.

- Risk Mitigation:

- Emphasizes insurance and emergency funds, protecting against life’s shocks (job loss, medical emergencies, market downturns) common in India.

- Behavioral Change and Discipline:

- Higher income doesn’t guarantee a high score — discipline does. The tool promotes better habits: budgeting, saving first, borrowing wisely, and investing consistently.

- Free/Low-Barrier Entry:

- Accessible online, no complex software or advisor fees needed initially. It democratizes professional-level insights for everyday Indians.

- Educational Value:

- Learning about the weighted factors educates users on what truly drives long-term wealth: consistent savings rate often outperforms chasing hot stocks.

Overall, users report greater confidence, reduced financial stress, and a roadmap toward financial independence.

Step-by-Step Guide: How to Use the Wealthpedia Financial Health Score Tool

10 Mins.

Gather Your Financial Data

Collect accurate, up-to-date information. Use bank statements, salary slips, loan statements, investment apps (Groww, Zerodha, MF Central), and insurance policies.

Key items: Monthly income: Salary + business/freelance + other (rentals, dividends).

Monthly expenses: Fixed (rent, EMIs, utilities, groceries) + variable (dining out, travel, shopping).

Total savings: Bank balances, liquid funds.

Total investments: Mutual funds, stocks, PF/EPF, PPF, NPS, gold, real estate value (if applicable).

Total debt: Outstanding home/car/personal loans, credit card balances, any other liabilities.

Emergency fund: Specifically liquid cash or savings easily accessible (not locked in FDs or investments).

Insurance: Sum assured for health insurance (self + family) and term life insurance.

Tip: Be honest. Rounding numbers is okay for a quick check, but precision gives better insights. For couples, consider combining or calculating separately then averaging.

Visit the Tool Page

Go to https://www.wealthpedia.in/financial-health-score/. The interface is clean and form based.

Enter Income Details

Input primary monthly income (salary/business) and any additional sources. The tool may calculate gross or take-home — follow on-screen prompts.

Enter Expense Details

Break down fixed and variable expenses. Accurate expense tracking here is crucial as it directly impacts cash flow and savings rate calculations.

Add Savings and Investments

Provide totals for current savings and broader investments. Some breakdowns (e.g., equity vs. debt) might be optional but improve accuracy for the investment pillar.

Input Liabilities (Debt)

Enter total outstanding debt and/or monthly EMI amounts. This feeds into the DTI ratio.

Add Emergency Fund and Insurance Information

Specify liquid emergency savings (in months of expenses equivalent if prompted).

Enter details on health and term insurance coverage.

Review and Calculate

Double-check entries for errors.

Click the “Calculate” button.

Review your score (0–100), category (if shown), pillar-wise breakdown, and personalized recommendations.

Interpret Results and Take Action

Note strong areas to maintain and weak ones to target.

Save or screenshot the results. Create an action plan (e.g., “Cut variable expenses by 10% to boost savings rate”).

Implement changes and re-test after 3–6 months.

Pro Tips for Best Results

Use the tool on a desktop for easier data entry if you have many numbers.

If self-employed, average income over 6–12 months for stability.

Update insurance and investment values periodically as markets fluctuate.

Combine with budgeting tools (like Excel or apps) for ongoing expense tracking.

The entire process is user-friendly, with no login required in most cases, ensuring privacy for your sensitive financial data (though always review the site’s privacy policy).

How to Improve Your Financial Health Score: Actionable Strategies

Once you have your score, focus on high-impact areas:

- Boost Savings Rate: Automate transfers to savings/investments on payday. Aim for 20%+ initially.

- Reduce Debt Burden: Prioritize high-interest debt (credit cards > personal loans). Use debt snowball or avalanche methods.

- Build Emergency Fund: Target 3–6 months’ expenses in liquid assets (savings account, liquid mutual funds).

- Optimize Cash Flow: Track expenses for 1–2 months; cut non-essential spending.

- Strengthen Investments: Ensure consistent SIPs aligned with goals; review asset allocation.

- Secure Insurance: Adequate term life (10–15x annual income) and comprehensive health cover.

- Increase Income: Side hustles or skill upgrades can help without proportionally increasing expenses.

Small, consistent changes compound. Many users see score improvements of 10–20 points within a year by focusing on 1–2 weak pillars.

FAQs About Wealthpedia Financial Health Score

What is a good Financial Health Score?

Above 70 is considered good; 80+ is excellent. Scores below 50 indicate significant vulnerabilities needing urgent attention. Context matters — compare against benchmarks for your age and income level.

How often should I check my score?

Every 6–12 months, or after major life events (job change, marriage, loan repayment, inheritance). More frequent checks (quarterly) during active improvement phases help maintain momentum.

Is this the same as a credit score (CIBIL)?

No. CIBIL/credit score focuses on your credit history and repayment behavior for lenders. The Financial Health Score evaluates your overall financial wellness, including savings, investments, and protection — areas credit scores ignore.

Can my score change quickly?

Yes. Positive actions like paying off a large debt chunk, building an emergency fund, or significantly increasing savings can boost it noticeably in months. Negative changes (new high debt or job loss) can lower it too.

Is the score 100% accurate?

It uses robust, advisor-aligned calculations based on your inputs, but it’s not a substitute for personalized professional advice. It’s a strong indicative tool and starting point. Factors like future market returns or unexpected expenses aren’t fully predictable.

Does higher income guarantee a higher score?

Not necessarily. A high earner with poor saving habits, heavy lifestyle expenses, and high debt can score lower than a moderate earner with excellent discipline. The tool rewards behavior over raw income.

Is it useful for beginners?

Absolutely. It simplifies complex finance concepts into one number and clear recommendations, making it ideal for those new to personal finance.

Should I base all financial decisions only on this score?

No. Use it as a diagnostic and tracking tool alongside budgeting, goal planning, tax advice, and consultation with SEBI-registered advisors or certified planners for major moves.

Does the tool store my data?

No, it doesn’t store your financial data. Check the site’s privacy policy. The calculator processes data client-side and there is no login/sign up is required to access the tool.

Are there similar tools in India?

Yes, some banks and apps offer variants (e.g., financial fitness quizzes), but Wealthpedia’s stands out for its data-driven, multi-pillar approach tailored to Indian users.

What if my score is low?

Don’t panic — it’s an opportunity. Start with the biggest pain point (often debt or emergency fund) and build habits gradually. Many improve dramatically over time.

Conclusion: Take Control of Your Financial Future Today

Wealthpedia’s Financial Health Score is a powerful, user-friendly tool that brings professional-level insight to everyday Indians. By distilling your financial life into one meaningful number and highlighting actionable steps, it empowers better habits, smarter decisions, and long-term prosperity.

Whether you’re a young professional in Ahmedabad managing your first serious salary, a business owner balancing cash flows, or a family planning for multiple goals, this calculator provides the clarity most people lack. It differs from narrower tools by being comprehensive yet simple, quantitative yet practical, and focused on discipline over mere accumulation.

Ready to start? Visit https://www.wealthpedia.in/financial-health-score/, gather your numbers, and calculate your score in minutes. Revisit this guide for interpretation and strategies. Track your progress quarterly, adjust as life changes, and consult professionals when needed.

Financial health, like physical health, improves with regular check-ups and consistent effort. Use this tool as your monthly or quarterly “financial health check-up” and move closer to stability, growth, and peace of mind.

Methodology & Data

Our tools and calculators are built using a robust combination of historical data, well-established financial models, and user-defined inputs to ensure relevance and practicality. Each tool incorporates carefully selected datasets—such as market returns, inflation trends, and regulatory frameworks—paired with proven methodologies like rolling return analysis, withdrawal rate modelling, and rule-based calculations.

To ensure reliability, every model undergoes rigorous design validation and back-testing against historical scenarios. We simulate real-world conditions across different market cycles to evaluate consistency and accuracy. Additionally, assumptions are regularly reviewed and refined to reflect changing financial environments.

We encourage users to explore the underlying methodology and assumptions behind each tool to better understand how results are generated, enabling more informed and confident financial decision-making.

Disclaimer: This guide is for educational and informational purposes. Financial decisions should consider your personal situation; consult qualified advisors. Scores and recommendations are indicative based on provided data. Always verify latest details directly on the Wealthpedia website.