Multi Goal FIRE Planner India

Are you trying to save for your child’s education, a house down payment, your marriage, and retirement — all at the same time? Most calculators force you to plan one goal at a time. That’s unrealistic.

The Wealthpedia Multi-Goal FIRE Planner is a powerful, completely free interactive calculator that does something no other tool in India does: it takes one single monthly SIP (plus your current portfolio) and automatically distributes it across multiple financial goals + your FIRE (Financial Independence, Retire Early) target using smart priority-based waterfall allocation.

It also includes step-up SIP, inflation adjustment, LTCG tax on withdrawals, and a beautiful full-journey chart from today until age 100.

In this complete 4000+ word professional guide, you will learn every single feature, how to use the calculator step-by-step, why it is far superior to every other multi-goal or FIRE calculator available in 2026, and how it can transform your financial planning.

What Exactly is the Wealthpedia Multi-Goal FIRE Planner?

This is not just another SIP calculator.

It is a complete financial life simulator that answers the most important question every middle-class Indian family asks:

“I can only save ₹60,000 per month. How do I fund my child’s education in 10 years, buy a house in 5 years, and still retire at 55 with dignity?”

Instead of giving you separate answers for each goal, the calculator treats your entire financial life as one portfolio and allocates money intelligently using:

- Priority ranking (you decide which goal is most important)

- Sequential “waterfall” funding (highest priority gets funded first)

- Real-time growth with monthly compounding

- Step-up SIP every year

- Accurate inflation adjustment

- Post-retirement withdrawal simulation with LTCG tax

Result? You get exact monthly SIP allocation, projected corpus, shortfall/surplus, and a visual journey of your wealth till age 100.

All Features Explained (One by One)

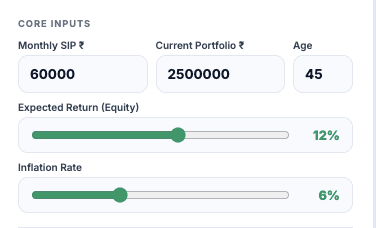

Core Inputs Section

- Monthly SIP ₹ — The single amount you can invest every month (this is the only money the calculator uses for all goals + FIRE).

- Current Portfolio ₹ — Your existing mutual funds, stocks, PPF, etc. The tool automatically grows this corpus every year.

- Current Age — Used for timeline calculations and the journey chart till age 100.

- Expected Equity Return (8–15%) — Realistic long-term return slider.

- Inflation Rate (4–10%) — Affects every future target and expense.

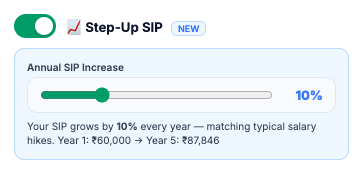

Step-Up SIP (One of the Rarest Features)

Toggle ON and choose annual increase (5–25%). The calculator automatically increases your SIP every year (exactly like salary hikes). You get a live preview: “Year 1: ₹60,000 → Year 5: ₹87,000”. Most calculators ignore step-up. This one models real life.

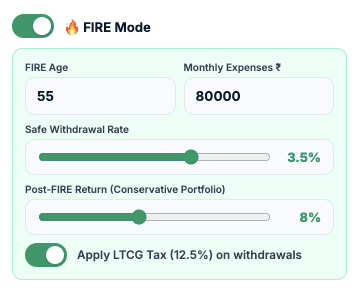

FIRE Mode (Fully Integrated with Goals)

Toggle ON and fill:

- Desired FIRE Age

- Current Monthly Expenses

- Safe Withdrawal Rate (2.5–4%)

- Post-FIRE Conservative Return (5–12%)

- LTCG Tax Toggle (12.5%) — Extremely rare. The calculator gross-up the withdrawal amount so you actually receive the required money after tax.

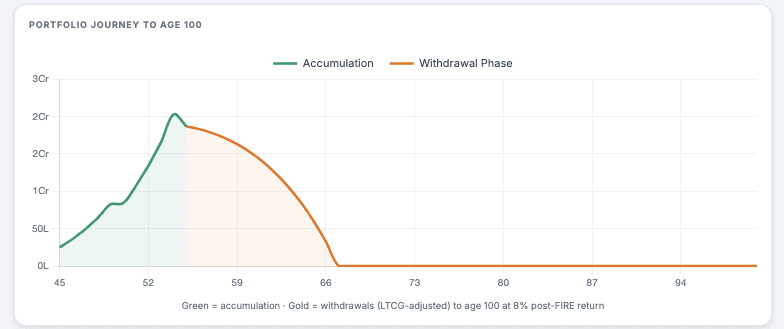

When FIRE mode is active, your FIRE corpus becomes the last goal in the waterfall and the chart shows both accumulation phase (green) and decumulation phase (gold) till age 100.

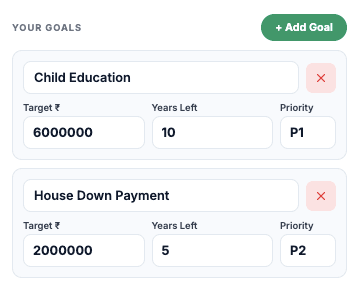

Multiple Goals with Priority Ranking

- Click + Add Goal any number of times.

- For each goal you enter: Name, Target Amount, Years Left, Priority (P1 = highest).

- Default goals: Child Education (P1) and House Down Payment (P2).

- You can delete or reorder priorities instantly.

The calculator automatically sorts goals by priority and funds them sequentially.

Smart Waterfall Allocation Engine (Heart of the Tool)

This is the most advanced part:

- Every year the portfolio grows with monthly compounding + step-up SIP.

- When a goal’s year arrives, the tool tries to fund it fully from the current corpus.

- If corpus is not enough, it shows shortfall and moves to the next goal.

- Higher priority goals are protected first.

- Leftover money continues growing for lower-priority goals and FIRE.

No other free Indian calculator does true sequential waterfall funding with existing corpus.

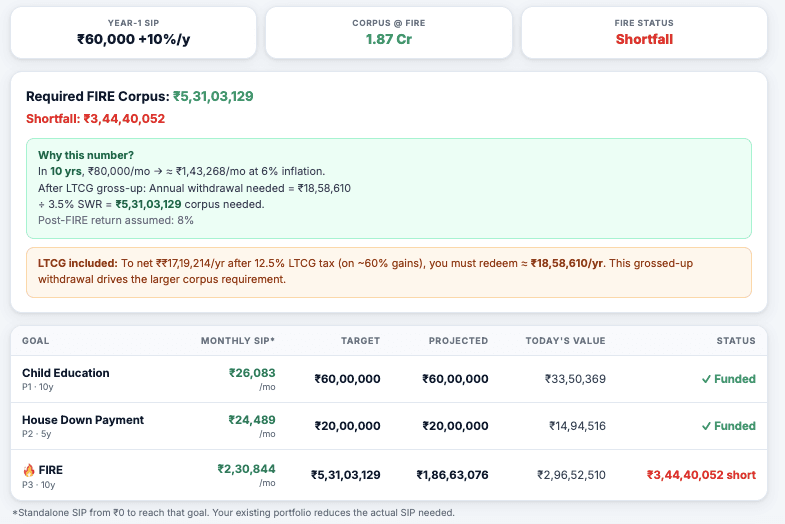

Live Results Dashboard

- Three Pill Summary Cards: Year-1 SIP, Corpus at FIRE, FIRE Status (On Track / Shortfall).

- Detailed FIRE Card — Explains exactly how the FIRE number was calculated, including inflation and LTCG gross-up.

- Goals Table:

- Monthly SIP required (standalone)

- Target amount (future value)

- Projected corpus

- Today’s present value

- Status (Funded or Shortfall in ₹)

- Portfolio Journey Chart (the most beautiful part):

- Green line = Accumulation phase

- Gold line = Withdrawal phase (only if FIRE is ON)

- Shows your wealth till age 100

- Updates instantly when you change any input

Step-by-Step Guide: How to Use the Multi-Goal FIRE Planner

Open the Calculator

Here is the link for the calculator : Multi Goal FIRE Planner India 2026: Smart Priority SIP Allocation + Trade-Off Simulator

Fill Core Inputs

Enter your monthly SIP capacity, current portfolio, age, expected return, and inflation.

Decide Step-Up SIP

Turn it ON and choose 10% (most realistic). Watch the preview.

Turn ON FIRE Mode

Enter your desired retirement age and current monthly expenses. Decide SWR and whether to apply LTCG tax.

Add Your Goals

Click + Add Goal as many times as needed. Example:

Goal 1 → House Down Payment → ₹25 lakh → 5 years → Priority 1

Goal 2 → Child Education → ₹60 lakh → 10 years → Priority 2

Goal 3 → Retirement Corpus (auto-added when FIRE is ON)

Click Anywhere or Just Wait

The calculator runs automatically on every change. No “Calculate” button needed.

Read the Results

Check the three pills first.

Read the FIRE explanation card.

Scroll to the table to see exact allocation per goal.

Study the chart — this is where most users get their “Aha!” moment.

Play “What-If” Scenarios

Change priorities, delay a goal, increase SIP, turn step-up off — everything updates instantly.

Benefits of Using This Calculator

- Saves hours of manual Excel work.

- Shows the real trade-offs between goals.

- Prevents over-saving for one goal at the cost of others.

- Gives you a single monthly number to act upon.

- Makes FIRE planning realistic by including multiple goals and taxes.

- Helps you visualise your money till age 100 — something no other tool does so clearly.

- Completely free, no login, no email, no data collection.

How This Calculator is Different & Superior to Other Tools in 2026

| Feature | Wealthpedia Multi-Goal FIRE Planner | Typical Multi-Goal Calculators (Groww, ET Money, Wealthify, etc.) | Typical FIRE Calculators |

|---|---|---|---|

| Single monthly SIP for all goals | Yes (waterfall) | Usually equal split or manual allocation | Not available |

| Priority-based sequential funding | Yes | Rarely available | No |

| Step-up SIP simulation | Yes (with preview) | Very few have it | Rare |

| Existing portfolio impact | Yes | Sometimes | Sometimes |

| FIRE integrated with multiple goals | Yes | Never | Separate tool |

| LTCG tax gross-up on withdrawals | Yes | Never seen in free tools | Rarely |

| Full portfolio journey chart to 100 | Yes (accumulation + withdrawal) | Basic bar charts only | Simple line only |

| Real-time updates on every change | Yes | Some require “Calculate” button | Yes |

| Number of goals supported | Unlimited | Usually 3–5 | Only retirement |

Verdict: Most tools are either “goal calculators” OR “FIRE calculators”. This is the only free tool that is both at the same time, with professional-level logic.

Unique Features No Other Calculator Offers

- True Waterfall Priority Funding — Money flows to highest priority goal first. Lower goals get only what is left. Real-life behaviour.

- LTCG Tax-Aware FIRE Calculation — Most FIRE calculators ignore tax on withdrawal. This one grosses up the corpus so your post-tax income matches your expense.

- Step-Up SIP + Existing Portfolio Simulation — Shows exactly how your current corpus grows and reduces future SIP burden.

- Portfolio Journey Chart with Decumulation Phase — You can literally see your money grow green, then turn gold and slowly come down till age 100.

- Instant What-If Analysis — Change one priority or delay one goal and everything recalculates instantly.

Real-Life Examples

Example 1: 38-year-old IT professional Monthly SIP ₹80,000 | Current portfolio ₹45 lakh | Wants house in 4 years + child education in 9 years + FIRE at 52. Result: Calculator shows he is on track for house and education but needs to increase SIP by ₹15,000 or delay FIRE by 2 years.

Example 2: 45-year-old couple Monthly SIP ₹50,000 | Wants to retire at 58. Calculator shows shortfall of ₹1.8 Cr because of LTCG tax. By turning step-up ON, the shortfall disappears.

What is FIRE (for Indians specifically)?

FIRE stands for Financial Independence, Retire Early. It is a personal finance movement and lifestyle philosophy that emphasizes aggressive saving (often 50-70% or more of income), frugal or intentional living, and smart investing to build a large enough investment corpus. Once achieved, passive income or withdrawals from this corpus can sustainably cover living expenses, freeing individuals from the need to work for money—potentially decades before the traditional retirement age of 60.

The core idea originated in the West (popularized by books like Your Money or Your Life in the 1990s and later blogs like Mr. Money Mustache), but it has gained traction among Indian millennials and Gen Z in the 2010s and 2020s. A 2025 Grant Thornton Bharat survey indicated that nearly 43% of Indians under 25 aspire to retire before 55, reflecting a shift from traditional job security toward time freedom, passion pursuits, or escaping corporate burnout.

For Indians, FIRE must be adapted to local realities. Key differences from Western contexts include:

- Higher inflation: General CPI around 5-6%, but lifestyle and healthcare inflation often higher (10-14% for medical costs).

- Longer retirement horizon: Retiring at 40-45 could mean 40-50+ years of funding needs, given improving life expectancy (often to 80-85 or beyond).

- Family and social obligations: Support for parents, children’s education/weddings, or joint family expectations.

- Healthcare system: Limited universal coverage; out-of-pocket costs are high, making comprehensive health insurance and buffers essential.

- Investment environment: Equity markets (Nifty/Sensex) have delivered strong long-term returns (historically 10-12%+ nominal), but with volatility. Fixed income, PPF, NPS, mutual funds, and index funds are common vehicles. Taxes (LTCG on equities, debt taxation) and rupee depreciation (if any international exposure) matter.

- Lifestyle variability: Costs differ vastly between metros (Mumbai, Delhi, Bengaluru) and Tier-2/3 cities or smaller towns. Geo-arbitrage (moving to lower-cost areas post-FIRE) is a popular strategy.

The mathematical foundation often references the “4% rule” (or Trinity Study-inspired): Save 25x your annual expenses. In the first year of retirement, withdraw 4% of the corpus; adjust subsequent withdrawals for inflation. If investments return enough (historically ~7% real in the US), the portfolio has a high chance of lasting 30 years. For Indians, many experts recommend a more conservative 2.5-3.5% safe withdrawal rate (SWR) due to higher inflation, volatility, and longer horizons, implying a 33-40x corpus multiple instead of 25x.

Achieving FIRE in India typically involves:

- Tracking and minimizing expenses without sacrificing quality of life.

- Maximizing savings rate through high income (IT, consulting, entrepreneurship) or side hustles.

- Investing consistently (SIP in equity mutual funds, index ETFs, debt for stability) with asset allocation shifting toward safety closer to FIRE.

- Building buffers for emergencies, healthcare, and sequence-of-returns risk (poor market returns early in retirement).

Many Indian FIRE practitioners do not fully “retire” but achieve financial independence (FI) and pursue flexible work, consulting, or passions (“Barista FIRE” or Coast FIRE variants). Success stories often highlight moving to quieter locations, pursuing hobbies, or starting small ventures. However, the movement stresses that FIRE is about freedom, not idleness.

Lean FIRE vs Fat FIRE (with ₹ examples)

FIRE is not one-size-fits-all; variants reflect different lifestyle ambitions.

- Lean FIRE: Minimalist, frugal approach. Focus on essentials with little discretionary spending. Suitable for those comfortable with simple living, possibly in smaller cities or with geo-arbitrage. Corpus target is often lower (closer to 25-28x annual expenses or conservative adjustments). Post-FIRE, you might cut back further if needed, and work remains optional but could supplement.

- Fat FIRE: Comfortable or luxurious lifestyle maintained indefinitely. Includes travel, dining out, premium healthcare, hobbies, gifting, and buffers for family. Requires significantly higher corpus (often 30-50x or more, or higher SWR conservatism). Aimed at high earners who want their pre-retirement lifestyle (or better) without compromises.

₹ Examples (illustrative, assuming current 2026 prices; always personalize with inflation projection):

Assume a 40-year-old planning to FIRE in 10-15 years, with retirement lasting 40+ years. Use ~3% SWR for safety in India (33x multiple) as a baseline, with adjustments. Inflation at 6% during accumulation; healthcare separate.

Lean FIRE Example:

- Current monthly expenses: ₹40,000 (₹4.8 lakh/year) — rent/shared housing in Tier-2 city, basic groceries, public transport, minimal travel, no big luxuries.

- Inflation-adjusted at retirement (say 15 years later at 6%): ~₹9.6-10 lakh/year.

- Corpus needed (33x): ~₹3.2-3.3 crore (or 25-28x for aggressive Lean: ~₹2.4-2.8 crore).

- Savings rate required: High (60-70%+). If current take-home ₹1.5 lakh/month, save ₹90k-1 lakh/month via SIPs in equity funds targeting 10-12% returns.

- Lifestyle post-FIRE: Simple home-cooked meals, local travel, community activities, perhaps part-time gigs. Many move to hometown or smaller towns to stretch the corpus. Healthcare via good insurance + buffer (add 20-25% extra corpus or separate medical fund).

Fat FIRE Example:

- Current monthly expenses: ₹1.5-2 lakh (₹18-24 lakh/year) — metro rent/housing EMI equivalent, dining out, international/domestic vacations, car, premium groceries, entertainment, shopping, family support.

- Inflation-adjusted at retirement: ~₹36-48 lakh/year or more.

- Corpus needed (33-40x for safety, or 45-50x for “fat” buffer): ₹12-20 crore+. Some calculations show Fat FIRE pushing toward ₹15-30 crore depending on ambitions.

- Savings rate: Extremely challenging unless high income (₹5 lakh+/month take-home) or business equity. Save/invest ₹3-4 lakh+/month with step-up SIPs.

- Lifestyle post-FIRE: Maintained or enhanced — frequent travel, club memberships, quality healthcare, helping children/grandchildren, hobbies like golf or collecting. Often stays in metros or has multiple properties. Requires diversified portfolio (equities for growth, debt/gold for stability) and possibly rental income.

Intermediate “Regular” or “Chubby FIRE” sits between: ₹75k-1 lakh/month expenses today → corpus of ₹5-10 crore range.

Realistic Indian adjustments (from various calculators and discussions):

- For ₹50k/month today expenses: Lean ~₹4-7 crore target; Fat ~₹10-15+ crore.

- Higher multiples account for India’s realities: longer life, medical inflation (up to 11-14%), and potential lower real returns after taxes/inflation.

Lean is more accessible for middle-class professionals; Fat often requires exceptional income or early business success. Hybrids like Coast FIRE (build a growing corpus early, then let it compound while working minimally) or Barista FIRE (part-time/low-stress work for benefits/expenses) bridge the gap.

How much corpus YOU need (based on lifestyle)

There is no universal number—the corpus depends on your current expenses, desired retirement lifestyle, age at FIRE, expected inflation, investment returns, life expectancy, location, family responsibilities, and risk tolerance.

Step-by-step calculation framework (India-specific):

- Track current annual expenses: List everything (housing, food, transport, utilities, healthcare, insurance, travel, entertainment, family obligations). Exclude work-specific costs (commute, office clothes) that may drop. Example: ₹60,000/month = ₹7.2 lakh/year.

- Project future expenses at retirement: Multiply by inflation over the years until FIRE. Formula: Future Expense = Current × (1 + inflation rate)^years. Use 5-7% general; 10-14% for healthcare separately. Example: ₹7.2 lakh today, 15 years at 6% → ~₹17.2 lakh/year.

- Decide post-retirement lifestyle multiplier: Lean (reduce 10-20%), Regular (maintain), Fat (increase 20-50% for luxuries).

- Choose Safe Withdrawal Rate (SWR):

- Traditional 4% (25x) is optimistic for India.

- Recommended: 3% (33x) or 2.5-3.5% for early retirees to handle 40+ year horizon and volatility. Some simulations support 3-3.5% with diversified Indian portfolios.

- Corpus Formula: Corpus = Projected Annual Expense / SWR. Or directly: Projected Expense × 33-40.

- Example (₹60k/month today, retire in 15 years at age 45, 6% inflation, maintain lifestyle, 3% SWR):

- Future annual: ~₹14.4 lakh.

- Corpus: ₹14.4 lakh / 0.03 ≈ ₹4.8 crore.

- Add 20-30% buffer for healthcare/uncertainties → ₹6-7 crore target.

- Example (₹60k/month today, retire in 15 years at age 45, 6% inflation, maintain lifestyle, 3% SWR):

- Additional factors:

- Healthcare: Often 25-62% of corpus erosion due to high inflation. Budget separate corpus or top-up insurance (super top-up plans).

- Location: Metro costs 1.5-2x Tier-2. Moving can reduce needs by 30-50%.

- Other income: Rental property, pensions, part-time work lowers corpus need.

- Returns assumption: 8-10% nominal post-retirement mix (equity + debt). Stress-test with Monte Carlo or historical Indian data.

- Taxes: Withdrawals may attract tax; plan with tax-efficient vehicles (equity for LTCG, NPS, etc.).

- Family: Children’s education (if not pre-funded), parental support, weddings.

Lifestyle-based rough bands (2026 perspective, for 40-45 retirement):

- Minimalist/Lean (Tier-2, frugal): ₹3-5 crore (expenses ~₹40-60k/month today).

- Comfortable/Regular (balanced): ₹5-10 crore (₹70k-1.2 lakh/month today).

- Premium/Fat (metro/luxury): ₹10-20+ crore (₹1.5 lakh+/month today).

Use online FIRE/retirement calculators (adjust for India inflation/returns) and review annually. Start with your current burn rate and savings rate—the higher the savings rate, the faster you reach any target (e.g., 50% savings can halve timeline vs 20%).

Why most FIRE plans fail in India

Despite growing interest, many FIRE plans falter or get delayed. Failures rarely stem from low earnings alone but from mismatched assumptions, life realities, and behavioral pitfalls.

Key reasons:

- Underestimating inflation and longevity: The classic 4%/25x rule assumes US-like conditions (lower inflation, 30-year horizon). In India, 6%+ inflation + 40-50 year retirement erodes purchasing power faster. Healthcare inflation (10-14%) can consume 50%+ of corpus. A ₹1 crore corpus today may feel like far less in 20-30 years.

- Sequence of returns risk: If markets crash or deliver low returns just after FIRE (e.g., early 2020s-style volatility), aggressive withdrawals deplete the corpus permanently. Indian equities are growth-oriented but volatile.

- Lifestyle creep and unrealistic frugality: During accumulation, people underestimate ongoing desires (better lifestyle, kids, travel). Post-FIRE, many find minimalism unsustainable long-term and resume work or dip into capital. High EMIs, education costs, and social pressures (weddings, gifts) derail savings rates.

- Family and social obligations: Supporting aging parents’ healthcare, children’s higher education/abroad studies, or unexpected family events. Joint family dynamics or cultural expectations add layers Western models ignore.

- Inadequate healthcare planning: One major hospitalization without proper coverage can wipe out years of savings. Many plans lack dedicated medical corpus or sufficient insurance.

- Over-optimistic returns and poor asset allocation: Assuming consistent 12%+ equity returns ignores drawdowns, taxes, and the need for diversification (debt, gold, international). Behavioral biases lead to panic selling or chasing hot assets.

- Life events and black swans: Job loss, health issues, divorce, economic downturns, or policy changes (tax, regulations). Early retirement removes employer benefits like group health insurance or PF contributions.

- Psychological factors: Boredom, loss of identity/purpose from work, or “one more year” syndrome. Many achieve the number but don’t retire fully, opting for flexible work.

- Calculation errors: Not adjusting expenses properly, ignoring taxes on withdrawals, or using static models without stress-testing.

- Low savings rate reality: High cost of living in metros, rising aspirations, and debt culture make 50%+ savings difficult for most. Borrowing for lifestyle rather than assets squeezes margins.

Mitigation strategies:

- Use conservative SWR (2.5-3.5%) and higher multiples (33-40x).

- Build multiple income streams (rentals, dividends, skills for consulting).

- Maintain flexibility: Aim for FI first, then decide on full retirement. Consider Barista/Coast variants.

- Annual reviews and buffers (emergency fund 12-24 months, separate healthcare bucket).

- Focus on geo-arbitrage, low-cost index investing, and comprehensive insurance.

- Prioritize purpose beyond money—many “successful” FIRE folks continue meaningful work.

FIRE in India is challenging but achievable with discipline, realism, and adaptation. It rewards early starters and high savers, but success often looks like financial freedom with optional work rather than complete idleness. Track progress with net worth and savings rate; adjust as life evolves. For personalized plans, consult a fiduciary advisor, as individual circumstances (income trajectory, risk appetite, family) vary widely.

Frequently Asked Questions (FAQs)

Is this calculator completely free?

Yes. No signup, no email, no hidden charges.

How many goals can I add?

As many as you want. The engine handles 10+ goals easily.

Does it consider taxes on gains?

Yes — only on the FIRE withdrawal phase via the LTCG toggle (12.5%).

Can I use it for different expected returns per goal?

Currently it uses one equity return for simplicity. This keeps calculations realistic and easy to understand.

Why is the chart going till age 100?

To show you the complete picture — whether your corpus will last throughout your lifetime after retirement.

Is the calculation accurate?

Yes. It uses monthly compounding (correct SIP formula) and exact waterfall logic used by professional financial planners.

Can I save my plan?

Currently the tool is for instant planning. You can take screenshots of the chart and table.

Conclusion

The Wealthpedia Multi-Goal FIRE Planner is not just another calculator — it is a complete financial co-pilot for every Indian family that wants to achieve multiple big goals without sacrificing retirement.

It forces you to make realistic trade-offs, shows you the exact impact of every decision, and gives you one clear monthly number to follow.

Try it today. Change one input. Watch the entire plan update instantly. You will immediately understand why this is the most advanced free planning tool available in India in 2026.

Ready to plan your multiple goals and FIRE together? Just scroll up and use the embedded calculator on this page.

Methodology & Data

Our tools and calculators are built using a robust combination of historical data, well-established financial models, and user-defined inputs to ensure relevance and practicality. Each tool incorporates carefully selected datasets—such as market returns, inflation trends, and regulatory frameworks—paired with proven methodologies like rolling return analysis, withdrawal rate modelling, and rule-based calculations.

To ensure reliability, every model undergoes rigorous design validation and back-testing against historical scenarios. We simulate real-world conditions across different market cycles to evaluate consistency and accuracy. Additionally, assumptions are regularly reviewed and refined to reflect changing financial environments.

We encourage users to explore the underlying methodology and assumptions behind each tool to better understand how results are generated, enabling more informed and confident financial decision-making.