Retirement dreams look different for everyone. For some, it means traveling the world without financial stress. For others, it’s simply living comfortably in your own home without depending on children or a pension. In 2026, with inflation continuing to pressure household budgets and life expectancy rising, thousands of working professionals are seriously evaluating their monthly SIP contributions.

One question keeps coming up in family discussions and office lunch breaks: Is ₹5,000 enough? Should I push to ₹10,000 or even ₹15,000 every month? Which amount actually moves the needle for retirement?

The gap between these three SIP levels feels small today — just ₹5,000–10,000 extra per month. But over a 20-year horizon, that difference can translate into a life-changing retirement corpus or a shortfall that forces you to delay retirement or compromise on lifestyle.

Most online SIP calculators show only one scenario at a time, leaving you to guess the impact of increasing your contribution. Wealthpedia’s free SIP Comparison Calculator changes that. It lets you instantly compare ₹5,000, ₹10,000, and ₹15,000 SIP side-by-side, along with different expected returns and inflation-adjusted real purchasing power — all in one clean, live table.

In this fresh 2026 guide, we dive deep into the real differences between these three popular SIP amounts specifically for retirement planning. We’ll use the latest market data, realistic assumptions, relatable Indian examples, and clear insights so you can decide what works best for your salary, age, and goals.

Ready to see the numbers for your own situation?

Open the SIP Comparison Calculator and compare instantly

The Retirement Reality Check in 2026

February 2026 saw SIP inflows touch ₹29,845 crore, showing that millions of Indians continue to trust systematic investing despite short-term market volatility. The mutual fund industry AUM has crossed ₹82 lakh crore, with equity SIPs remaining a favourite for long-term goals like retirement.

Yet, many investors still underestimate how small monthly differences compound over time — or how inflation quietly erodes future purchasing power.

Nifty 50 TRI has historically delivered strong long-term returns, but recent rolling periods and 2025–early 2026 market movements remind us that returns are never guaranteed. Conservative planners use 10%, realistic equity investors target 12%, and those comfortable with volatility test 14%.

A 20-year horizon (common for people in their mid-30s to early 40s) is long enough for compounding to shine but short enough that every extra rupee invested today matters hugely.

This is where comparing ₹5,000 vs ₹10,000 vs ₹15,000 becomes eye-opening. Let’s look at the numbers.

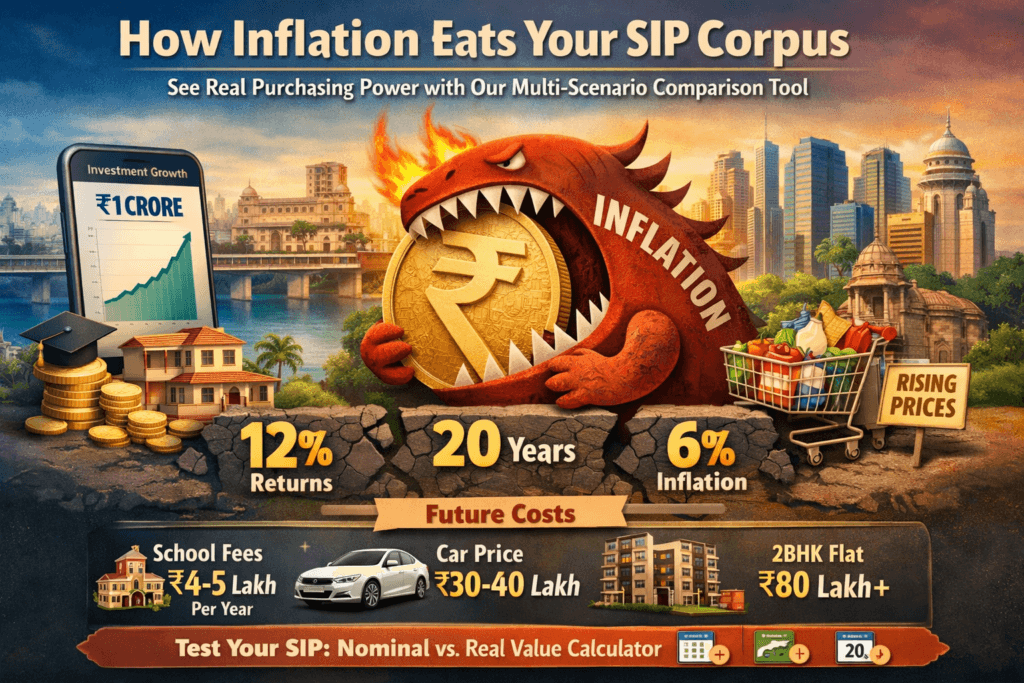

SIP Comparison Table for Retirement Planning (20 Years, 6% Inflation – April 2026)

| Scenario | Monthly SIP | Expected Return | Total Amount Invested | Nominal Corpus (Future Value) | Inflation‑Adjusted Real Value (Today’s Purchasing Power) | Wealth Gained (Nominal) |

|---|---|---|---|---|---|---|

| A: Conservative Starter | ₹5,000 | 12% | ₹12.00 Lakh | ₹49.96 Lakh | ₹15.58 Lakh | ₹37.96 Lakh |

| B: Steady Builder | ₹10,000 | 12% | ₹24.00 Lakh | ₹99.91 Lakh | ₹31.15 Lakh | ₹75.91 Lakh |

| C: Serious Retiree | ₹15,000 | 12% | ₹36.00 Lakh | ₹1.50 Crore | ₹46.73 Lakh | ₹1.14 Crore |

| D: Safety First (10%) | ₹10,000 | 10% | ₹24.00 Lakh | ₹76.57 Lakh | ₹23.87 Lakh | ₹52.57 Lakh |

| E: Growth Focused | ₹10,000 | 14% | ₹24.00 Lakh | ₹1.32 Crore | ₹41.04 Lakh | ₹1.08 Crore |

| F: Accelerated Plan | ₹15,000 | 14% | ₹36.00 Lakh | ₹1.97 Crore | ₹61.57 Lakh | ₹1.61 Crore |

What the Numbers Reveal:

• Moving from ₹5,000 to ₹10,000 monthly SIP roughly doubles both your invested capital and the final corpus at 12% return.

• Jumping to ₹15,000 adds another ₹50 lakh+ in nominal value and ₹15 lakh+ in today’s real purchasing power compared to ₹10,000.

• A 2% higher return (12% to 14%) on ₹10,000 SIP delivers over ₹32 lakh extra nominal corpus — more than the entire ₹5,000 SIP scenario in some cases.

• At 6% inflation, the real value column shows the true lifestyle impact. ₹1.50 crore in 2046 feels closer to ₹46–47 lakh in today’s money.

These calculations match the exact math in Wealthpedia’s SIP Comparison Calculator (monthly compounding, investments at the beginning of each period).

Compare ₹5,000, ₹10,000, and ₹15,000 SIP with your preferred returns and tenure →

How Different SIP Amounts Are Shaping Retirement Plans

Case 1: Neha, 36, Marketing Manager in Ahmedabad

Neha earns ₹9.5 lakh annually after taxes. She began with ₹5,000 SIP two years ago (Scenario A style) in a flexi-cap fund. Using the comparison tool, she realised that staying at ₹5,000 would give her only about ₹50 lakh nominal after 20 years — barely enough for basic expenses. She increased to ₹10,000 after a promotion and now projects ₹99–100 lakh nominal. She plans one more step-up to ₹12,000–13,000 next year.

Case 2: The Sharma Family, 39 & 41, Dual-Income Household in Surat

Both working in private sector with combined take-home around ₹18–20 lakh. They run ₹8,000 each (total ₹16,000). After testing ₹10,000 and ₹15,000 per person in the calculator, they decided to stretch to ₹12,000 each. At 12% expected return, they are targeting a combined corpus above ₹2.5 crore nominal — giving them the freedom to retire comfortably or pursue part-time work.

Case 3: Sanjay, 44, Bank Officer in Vadodara

Sanjay has a stable job but limited surplus. He can manage only ₹7,000–8,000 currently. He ran conservative 10% scenarios and aggressive 14% ones. The tool helped him understand that consistent ₹10,000 (with annual step-ups) plus some lump-sum investments could still get him close to a decent retirement. He now focuses on cutting unnecessary expenses to reach ₹10,000.

These are not theoretical cases — they reflect the kind of decisions thousands of middle-class families are making in 2026 using multi-scenario comparison.

Understanding Returns in Today’s Market (2026 Perspective)

Recent data shows Nifty 50 movements have been volatile in early 2026, with the index fluctuating around 22,000–23,000 levels in April. Long-term TRI returns remain attractive, but forward-looking assumptions should stay realistic:

• Conservative (debt-heavy or cautious equity mix): 10%

• Balanced diversified equity SIP: 12%

• Growth-oriented (higher mid/small-cap allocation): 14%

Higher returns come with higher volatility. The SIP Comparison Calculator lets you stress-test all three assumptions without guesswork.

Actionable Tips to Decide Your SIP Level for Retirement

• Assess your current cash flow honestly — Start at ₹5,000 if ₹10,000 feels impossible, but commit to stepping up 10–15% every year.

• Align with your retirement age and lifestyle goal — If you want to retire at 55–58 with travel and hobbies, lean toward ₹15,000 (or higher with step-ups).

• Factor in other income sources — EPF, gratuity, rental income, or spouse’s pension can reduce the burden on SIP corpus.

• Diversify smartly — Don’t put the entire SIP in one fund. A mix of large-cap stability and flexi-cap growth works well for retirement portfolios.

• Use the tool regularly — Run fresh comparisons every 12 months or after a salary hike/bonus.

Mistakes That Can Derail Your Retirement SIP Journey

Many people begin with good intentions at ₹5,000 but never increase it. Others chase last year’s top-performing fund expecting 18–20% forever. Some pause SIPs when markets correct, missing the best buying opportunities. The biggest hidden mistake? Looking only at nominal numbers and ignoring that inflation will make tomorrow’s rupees worth far less.

Comparing multiple amounts and return scenarios upfront helps avoid these pitfalls.

Step-by-Step: Using the SIP Comparison Calculator for Your Retirement Plan

1. Go to the tool page.

2. Input ₹5,000, ₹10,000, and ₹15,000 as separate rows.

3. Try 10%, 12%, and 14% returns.

4. Set tenure to 20 years (or your actual remaining years) and inflation to 6%.

5. Review the live table — especially the real value column.

6. Adjust and bookmark the combination that feels achievable yet meaningful.

The calculator is mobile-friendly, requires no registration, and gives instant results.

Frequently Asked Questions (FAQs)

Which is better for retirement — ₹5,000, ₹10,000 or ₹15,000 SIP?

₹10,000 offers a strong balance for most families. ₹15,000 accelerates your corpus significantly if your budget allows. ₹5,000 is a good starting point but needs regular step-ups.

How much extra corpus does ₹5,000 more SIP create over 20 years?

At 12% return, moving from ₹10,000 to ₹15,000 adds roughly ₹50 lakh nominal and ₹15 lakh in today’s real value.

Does inflation really make that much difference?

Yes. The real value column shows that future crores buy far less than we imagine today.

What if my actual returns are lower than 12%?

You can compensate by increasing SIP amount gradually or extending your working years slightly. The tool helps visualise all options.

Can I mix these amounts — for example ₹5,000 in one fund and ₹10,000 in another?

Absolutely. Many investors split across 2–3 funds for better diversification.

How does this tool compare to popular apps like Groww or Zerodha?

It stands out by showing multiple SIP levels and inflation-adjusted values together in one view.

When should I review and possibly increase my SIP?

After every salary hike, bonus, or at least once a year.

Take the Next Step Toward a Stronger Retirement

₹5,000, ₹10,000, or ₹15,000 — none is “wrong,” but each leads to a very different retirement story. The ₹5,000 investor who never increases may struggle with basic expenses. The ₹15,000 investor who stays consistent often enjoys real financial freedom.

Don’t leave your retirement to chance or single-number estimates. Use the Wealthpedia SIP Comparison Calculator to compare these three amounts (and any custom variations) with clear nominal and real-value outcomes.

Compare ₹5,000 vs ₹10,000 vs ₹15,000 SIP for Your Retirement Right Now →

Make the comparison today. Increase your SIP if possible. Review it every year. Your future self will thank you.

Happy Investing and Planning!

Team Wealthpedia

Disclaimer: This content is for educational and illustrative purposes only. Mutual fund investments are subject to market risks. Past performance is not indicative of future results. Please consult a SEBI-registered financial advisor before making investment decisions. Calculations are based on standard SIP future value formula with monthly compounding and assumed constant returns.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up