As we step into 2026, retirement planning in India has never been more critical—or more achievable. With rising life expectancy, unpredictable healthcare costs, and inflation quietly eroding purchasing power, relying solely on EPF, NPS, or a traditional pension may not suffice for the lifestyle you envision. Systematic Investment Plans (SIPs) in mutual funds have emerged as the go-to wealth-building tool for millions of Indians, offering discipline, rupee-cost averaging, and the magic of compounding over decades.

But here’s the truth: not all SIPs are created equal. The “best” SIP strategy for retirement isn’t a one-size-fits-all formula. It depends on your starting age, monthly commitment, expected returns, time horizon, and—crucially—the real value of your corpus after inflation. In this comprehensive 2026 guide, we’ll dive deep into crafting an optimal SIP strategy tailored for retirement. We’ll test multiple investment amounts, realistic return scenarios, and use a real-value calculator to show what your money will actually buy in the future.

By the end, you’ll have actionable insights, data-backed projections, and a clear path forward. Ready to future-proof your golden years? Let’s begin.

Why SIPs Are the Cornerstone of Retirement Planning in 2026

SIPs allow you to invest a fixed amount regularly—usually monthly—into mutual funds, regardless of market conditions. This disciplined approach eliminates the need to time the market, a feat even seasoned investors struggle with. In 2026, with India’s economy showing resilience and headline inflation around 3.2% (as per recent MOSPI data for early 2026), though long-term planning still demands a prudent 5-6% buffer, equity markets continue to offer double-digit potential while hybrid options provide stability. SIPs stand out for retirement.

Consider the power of compounding: a modest ₹10,000 monthly SIP at a conservative 12% annual return over 20 years grows to nearly ₹99 lakh nominally. But factor in inflation, and the real purchasing power tells a different story—we’ll crunch those numbers shortly.

Unlike lump-sum investments, SIPs mitigate volatility through rupee-cost averaging. When markets dip, you buy more units at lower prices; when they rise, your existing units appreciate. For retirement, where your corpus must last 25-30+ years post-retirement, this risk-adjusted growth is invaluable.

Recent trends in 2026 reinforce why now is the moment: equity mutual funds in large-cap, flexi-cap, and mid-cap categories have historically delivered 10-18% CAGR over the past decade. Debt and hybrid funds offer 7-9% with lower volatility. With the RBI maintaining its 4% inflation target (within 2-6% band), disciplined SIP investors are well-positioned. Success, however, hinges on strategy—not just starting, but optimizing through testing and real-value assessment.

Key Factors Shaping Your SIP Retirement Strategy

Before testing scenarios, understand the variables that matter most in 2026:

1. Investment Amount: SIPs can start as low as ₹500, but scaling with income (via step-up features) accelerates growth.

2. Time Horizon: Longer periods amplify compounding. Someone in their mid-30s in 2026 retiring at 60 has 25 years; even starting at 45 offers 15 impactful years.

3. Expected Returns: Realistic 2026 projections based on historical and category trends:

• Conservative (debt/hybrid-heavy): 8-10%

• Moderate (balanced equity): 10-12%

• Aggressive (equity-focused): 12-15%

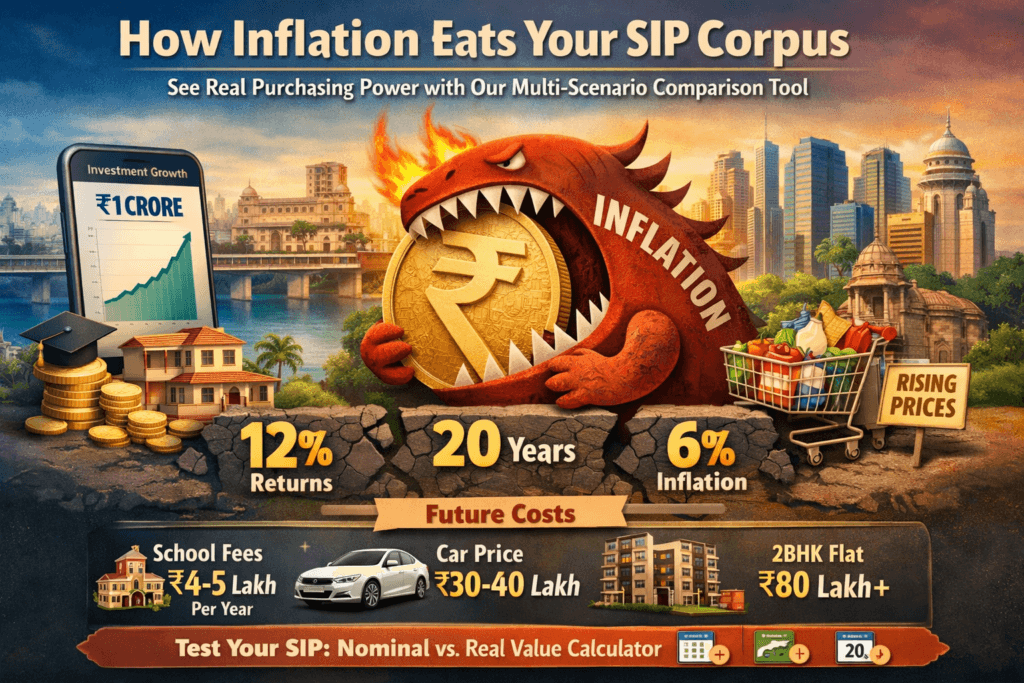

4. Inflation: Nominal returns can mislead. At a prudent 5% long-term assumption (despite current prints near 3.2%), ₹1 crore today may require significantly more in future purchasing power.

5. Asset Allocation: Shift from aggressive equity in early years to hybrid/debt nearer retirement. Diversify with international or gold elements for hedging.

6. Step-Up SIPs: Annual increases of 10-20% align contributions with salary growth, potentially boosting corpus by 30-60%.

Tax efficiency remains attractive: Equity SIPs (held >1 year) qualify for long-term capital gains at 12.5% above ₹1.25 lakh (2026 rules), while ELSS funds still offer Section 80C benefits up to ₹1.5 lakh.

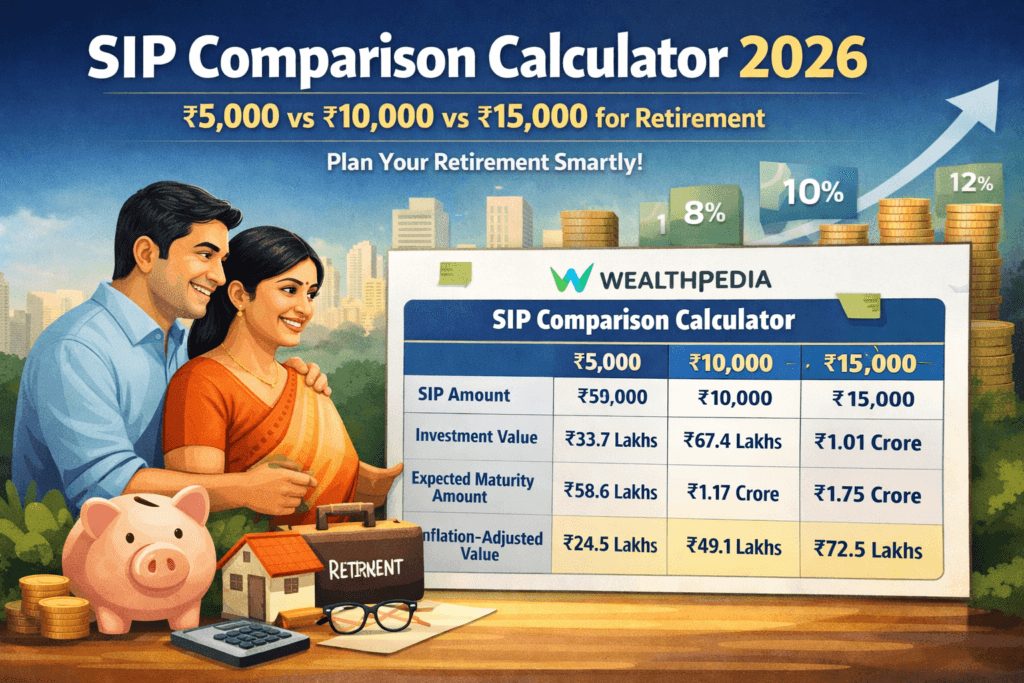

Testing Multiple SIP Amounts: Real Scenarios for 2026 Investors

Let’s translate theory into numbers. Using standard SIP future-value modeling (compounded monthly), here are projections for common amounts across horizons and return rates. Real value assumes 5% annual inflation adjustment to reflect today’s purchasing power.

₹5,000 Monthly SIP (Entry-Level Starter)

• 20 years @ 12%: Nominal corpus ≈ ₹49.5 lakh (total invested ₹12 lakh); Real value ≈ ₹18.2 lakh.

• 25 years @ 12%: Nominal ≈ ₹1.02 crore; Real value ≈ ₹30.5 lakh.

• At 15% aggressive: 20-year nominal rises to ≈ ₹68.5 lakh (real ≈ ₹25.3 lakh).

₹10,000 Monthly SIP (Common Mid-Income Choice)

• 20 years @ 12%: Nominal ≈ ₹99 lakh; Real value ≈ ₹36.5 lakh.

• 25 years @ 12%: Nominal ≈ ₹2.05 crore; Real value ≈ ₹61 lakh.

• At 10% moderate: 20-year nominal ≈ ₹76.5 lakh; Real ≈ ₹28.2 lakh.

₹20,000 or ₹50,000 Monthly SIP (Higher Earners) Scaling doubles or quintuples outcomes. A ₹50,000 SIP at 12% over 20 years builds a nominal corpus near ₹4.95 crore (real value ≈ ₹1.82 crore)—potentially supporting a comfortable post-retirement lifestyle for many families.

These simulations highlight a key insight: higher amounts and longer horizons deliver exponential growth, but inflation halves the “feel-good” nominal figures. Testing multiples reveals your personal sweet spot—many discover that a moderate step-up SIP bridges gaps more efficiently than a high flat amount.

The Real Value Calculator: Why Nominal Returns Deceive

Basic calculators show only future nominal value. A true real-value SIP calculator adjusts the end corpus by dividing it by the inflation factor over the period. This reveals actual buying power.

In 2026, with food and fuel volatility persisting despite overall CPI moderation, ignoring inflation risks serious under-planning. Equity-heavy SIPs have historically outpaced inflation over 10+ years, but conservative portfolios may barely keep pace—making hybrid strategies popular for balanced retirement planning.

Aim for returns 4-6% above assumed inflation for real growth. Our advanced calculator lets you toggle custom inflation rates, step-ups, and pause periods for precise 2026 modeling.

Advanced SIP Strategies Tailored for 2026 Retirement Goals

• Step-Up SIP: Start at ₹10,000 and increase 10% annually. By year 15, contributions naturally rise, often adding 40-60% more to the final corpus versus flat SIPs.

• Goal-Based Allocation: Under 40 → 70-80% equity; 40-55 → 50-60% equity; nearing retirement → debt-heavy with SWP for income.

• Fund Selection: Focus on consistent performers in flexi-cap, large-cap, and hybrid categories rather than chasing recent outperformers.

• Tax Optimization: Combine ELSS for deductions with diversified equity/debt for efficient withdrawals via SWP post-retirement.

• Annual Review: Rebalance to match life-stage changes and market conditions.

Risks and Mitigation in 2026 SIP Retirement Planning

Volatility, sequence-of-returns risk near retirement, and longevity (living 25-30 years post-retirement) remain concerns. Mitigate with:

• Separate emergency funds (6-12 months expenses).

• Diversification across 4-6 funds and asset classes.

• Adequate term life and health insurance.

• Gradual de-risking as you approach retirement.

Tax Implications for SIPs in 2026

Equity-oriented funds: LTCG tax at 12.5% on gains above ₹1.25 lakh after 12 months. STCG at 20%. Debt/hybrid: taxed as per slab (with nuances). Use FIFO for redemptions from multiple SIP installments. Strategic SWP planning can optimize post-retirement tax liability.

How to Test and Compare Your SIP Strategies Effortlessly

Manually running dozens of scenarios is time-consuming. That’s why a robust SIP comparison calculator becomes invaluable. It allows side-by-side testing of multiple amounts, return assumptions, step-up rates, inflation adjustments, and real-value outcomes—with dynamic tables and month-wise breakdowns.

To instantly compare ₹5,000 vs ₹20,000 SIPs at 12% over 20-25 years, or model aggressive versus conservative portfolios with custom inflation, head to our free SIP Comparison Calculator. It’s designed specifically for 2026 realities, requires no login for basic use, and helps users fine-tune plans quickly. Many discover they can hit retirement targets with smarter step-ups rather than dramatically higher monthly commitments. Try it here: SIP Comparison Calculator.

Real-Life Case Studies

• 38-year-old professional: ₹15,000 monthly SIP (60% equity) at ~12% over 22 years builds nominal ~₹3.2 crore (real value ~₹1.1 crore), supporting ₹70,000-80,000 monthly inflation-adjusted withdrawals.

• 48-year-old entrepreneur: ₹30,000 SIP over 12 years at 10-11% creates a solid supplement to existing savings for semi-retirement.

Consistent testing and adjustment make these outcomes repeatable.

Common Pitfalls to Avoid

Starting late, stopping during market dips, ignoring expense ratios (prefer direct plans), or failing to adjust for inflation are frequent mistakes. Discipline and periodic reviews win in the long run.

Conclusion: Your 2026 Action Plan for Retirement Freedom

The best SIP strategy for retirement in 2026 combines realistic testing of amounts and returns with a clear focus on real (inflation-adjusted) value. Start sustainably, incorporate step-ups, diversify wisely, and review annually. Use tools that let you simulate multiple scenarios to stay motivated and on track.

Don’t leave your golden years to chance. Open the SIP Comparison Calculator, input your numbers, and map your personalized path—whether targeting ₹1 crore or ₹5 crore+ corpus. The power of disciplined, tested SIP investing is in your hands.

Begin now—your 2046+ self will thank you.

FAQs: Best SIP Strategy for Retirement in 2026

What is the best SIP amount for retirement planning in 2026?

There is no universal “best” amount—it depends on your age, income, expenses, and target corpus. Starting with ₹5,000-10,000 monthly is realistic for many, while higher earners may target ₹20,000+. The key is consistency plus annual step-ups. Use a real-value calculator to test what fits your retirement goal (e.g., ₹2-5 crore nominal corpus) while accounting for 5% inflation.

How much corpus do I need for retirement in India in 2026?

A common benchmark is 25-30 times your current annual expenses. If you spend ₹6 lakh yearly today, aim for ₹1.5-1.8 crore in real terms at retirement. Factor in healthcare, lifestyle inflation, and 25-30 years of post-retirement life. Test scenarios in a SIP comparison calculator to arrive at a personalized target.

What realistic returns should I assume for retirement SIPs in 2026?

For planning, use conservative 10-12% for moderate equity portfolios and 8-10% for hybrid/debt-heavy ones. Aggressive equity SIPs have historically delivered 12-15%+ over long periods, but past performance isn’t guaranteed. Always run real-value projections rather than relying solely on nominal figures.

How does inflation affect my SIP retirement corpus?

At 5% annual inflation, the real purchasing power of your corpus roughly halves every 14 years. A ₹2 crore nominal amount after 25 years may feel like only ₹60-75 lakh in today’s rupees. This is why real-value calculators are essential—they show true lifestyle sustainability.

Should I use a step-up SIP for retirement?

Yes—step-up SIPs (increasing contribution by 10-20% yearly) are highly effective for retirement as they align with salary growth and combat inflation automatically. They can significantly boost your final corpus (often 40%+) without feeling like a sudden burden.

Are SIPs in equity mutual funds tax-efficient for retirement?

Equity SIPs (including ELSS) are relatively tax-efficient. LTCG above ₹1.25 lakh is taxed at 12.5% after one year. Use direct plans to minimize expense ratios. For withdrawals, SWP from a mix of equity and debt can help manage tax slabs effectively.

What if markets fall near my retirement?

This is sequence-of-returns risk. Mitigate by gradually shifting to hybrid/debt funds 5-7 years before retirement and maintaining a separate 2-3 year expense buffer in liquid assets. SIPs over long horizons have historically recovered well from downturns.

Can I pause or stop my SIP temporarily?

Most platforms allow pauses, but for retirement goals, minimize interruptions. Use the comparison calculator to model pause scenarios and see the impact on your corpus. Consistency usually outweighs short pauses.

How often should I review my retirement SIP portfolio?

Review annually or after major life events (job change, marriage, etc.). Rebalance asset allocation as you near retirement. Tools like the SIP comparison calculator make quick “what-if” testing easy.

Is the SIP Comparison Calculator useful for retirement planning?

Absolutely. It lets you test multiple SIP amounts, return rates, step-up options, inflation adjustments, and real-value outcomes side-by-side. Whether you’re comparing flat vs step-up SIPs or conservative vs aggressive strategies, it provides instant, personalized insights tailored for 2026 planning. Access it here for free: SIP Comparison Calculator.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up