In the bustling streets of Ahmedabad or the tech hubs of Bengaluru, millions of Indians are quietly building wealth through Systematic Investment Plans (SIPs). You set up an auto-debit of ₹5,000 or ₹10,000 every month into a mutual fund, watch the app notifications show steady growth, and dream of that comfortable retirement, your child’s foreign education, or a second home by the beach. The numbers look impressive on paper—12% annual returns turning your modest contributions into crores over two decades. But here’s the harsh truth most investors overlook: inflation is silently devouring your SIP corpus, eroding the real purchasing power of every rupee you accumulate.

By 2026, with India’s CPI inflation hovering around 3.2% in early months and RBI projecting 4.6% for FY27 amid global uncertainties like energy price volatility, the silent wealth destroyer is far from dormant. Historical data shows India’s average inflation has hovered near 5.6-6% over the past two decades, with spikes touching 8-10% in certain years. What feels like a growing nest egg today might barely cover tomorrow’s groceries, school fees, or healthcare if you ignore the real value.

This isn’t fear-mongering—it’s financial reality. In this detailed guide, we’ll unpack exactly how inflation eats into your SIP returns, compare nominal vs. real purchasing power across multiple scenarios, and show you why a simple adjustment in perspective can transform your investment strategy. Most importantly, we’ll introduce a practical way to visualize this yourself: our free multi-scenario SIP comparison and real value calculator. You can test different monthly amounts, expected returns, inflation rates, and tenures in seconds to see what your corpus will actually buy in future rupees.

Ready to stop guessing and start calculating real wealth? Let’s dive in.

Understanding SIPs: The Power of Discipline Meets the Reality of Markets

Systematic Investment Plans, or SIPs, have democratized investing in India since the early 2000s. Instead of timing the market or needing a lump sum, you commit a fixed amount—say ₹5,000 monthly—into equity, debt, or hybrid mutual funds. The magic lies in rupee-cost averaging: you buy more units when markets dip and fewer when they rise, reducing average purchase cost over time.

According to industry data, equity-oriented SIPs have delivered average annualized returns of 12-15% over 10+ year horizons in many categories like flexi-cap and large-cap funds, with mid- and small-cap SIPs sometimes touching 14-20% in strong periods. That’s far superior to fixed deposits (6-8%) or savings accounts. SEBI-registered mutual funds, backed by AMFI data, show that consistent SIP investors in Nifty 50 TRI benchmarks have seen XIRR (extended internal rate of return) around 12-15% over long periods, with zero negative 10-year SIP returns in historical rolling windows.

Yet, here’s the catch: these are nominal returns. They don’t account for the rising cost of living. Your SIP statement might proudly display ₹1 crore corpus after 20 years, but if inflation averages 6%, that crore might only feel like ₹32-35 lakh in today’s purchasing power. That’s the difference between dreaming of financial freedom and waking up to stretched budgets.

SIPs work best for long-term goals—retirement (20-30 years), children’s education (10-15 years), or wealth creation. But without factoring inflation, even the best-performing fund can leave you short. This is why smart investors now demand tools that show real value, not just headline growth.

The Silent Erosion: What Inflation Really Means for Your Money

Inflation isn’t just a headline number from the Ministry of Statistics and Programme Implementation (MoSPI). It’s the steady increase in prices of goods and services that chips away at your money’s buying power. India’s Consumer Price Index (CPI) tracks a basket including food (nearly 50% weight), housing, transport, healthcare, and education. As of February 2026, headline CPI stood at 3.21% year-on-year, down from higher levels in prior years, but RBI’s projections signal it could average 4-5%+ in coming years due to food volatility, global oil shocks, and supply chain pressures.

Look back at history: Between 2000 and 2025, India’s average annual CPI inflation was around 5.6-7.2% depending on the dataset. Spikes hit double digits in 2010-2013 (up to 10-12%), while recent years (2023-2025) moderated to 4.9-6.7%. Even at a conservative 6% average, prices double roughly every 12 years. A ₹100 note today buys only ₹50 worth of goods in 12 years.

Real-life impact on SIP investors? Consider everyday items in an Indian household:

• A kg of rice or dal that costs ₹50-60 today could cost ₹120-150 in 15 years at 6% inflation.

• Private school fees averaging ₹1-2 lakh annually per child might balloon to ₹4-5 lakh.

• A mid-range car (₹10-15 lakh today) or a 2BHK flat in a Tier-2 city could require 2-3x the corpus.

Inflation hits fixed-income investors hardest, but even equity SIPs aren’t immune if returns don’t consistently outpace it. The formula for real return is simple yet eye-opening:

Real Return = [(1 + Nominal Return) / (1 + Inflation Rate)] – 1

A 12% nominal return at 6% inflation gives you only ~5.66% real growth. Over decades, this gap compounds dramatically. Your SIP corpus grows in absolute terms, but its purchasing power lags behind lifestyle inflation—especially in India where healthcare and education costs often rise faster than general CPI (sometimes 8-10% annually).

Nominal vs Real Returns: Why Your SIP Statement Is Lying to You (Politely)

Most SIP calculators and fund fact sheets proudly display nominal growth. A ₹5,000 monthly SIP at 12% for 20 years looks like ₹49.95 lakh corpus (total invested: ₹12 lakh). Impressive, right? But adjust for 6% inflation, and the real purchasing power shrinks to about ₹22.3 lakh in today’s rupees.

Why the discrepancy? Because every rupee you invest today faces inflation from Day 1, and your future corpus must battle cumulative price rises over the entire period. Nominal figures ignore this. Real-value calculations use the adjusted rate to show what your money can actually buy when you withdraw.

This distinction matters hugely for goal-based planning. Retirement planners often assume 6-7% post-retirement inflation. A corpus that seems sufficient on paper might force lifestyle downgrades—or worse, force you back to work.

Real-World Scenarios: How Inflation Devours SIP Corpus – Multi-Case Comparison

Let’s move from theory to numbers. Using standard SIP future value calculations (monthly compounding, investments at the start of each period for conservative illustration), here are multiple scenarios. These mirror what our SIP comparison calculator lets you test instantly with custom inputs.

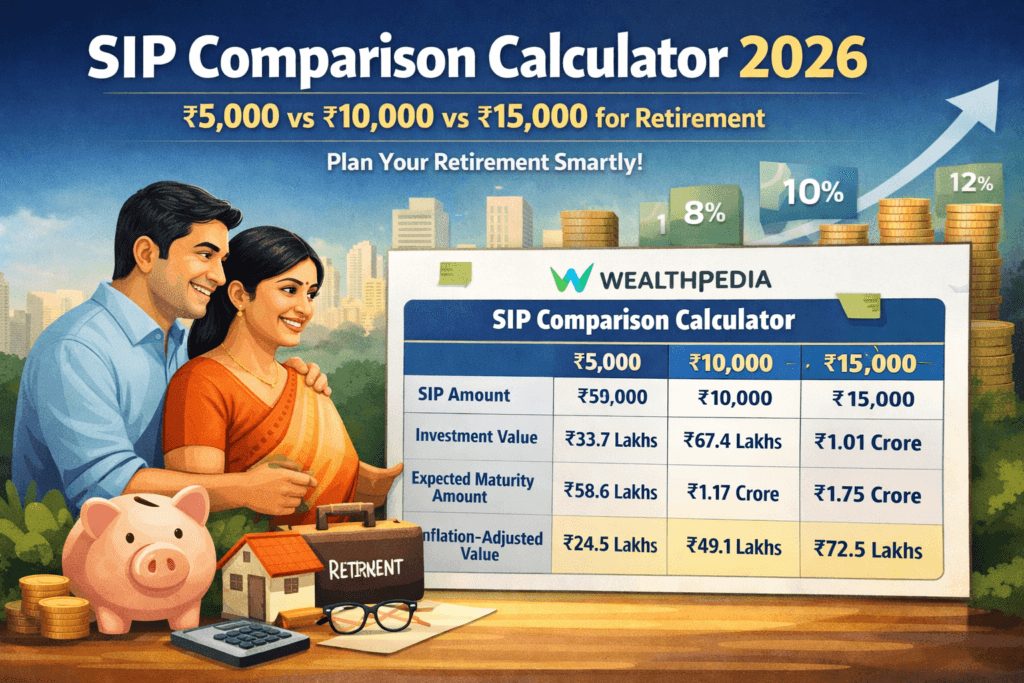

Scenario 1: Conservative Investor – ₹5,000/month SIP, 12% expected return, 20 years

• Total invested: ₹12 lakh

• Nominal corpus: ≈ ₹49.96 lakh

• At 6% average inflation: Real purchasing power ≈ ₹22.3 lakh (today’s terms)

• Real annualized return: ≈5.66%

Interpretation: Your “crore dream” is halved in real terms. Enough for a decent retirement supplement in a Tier-2 city, but not the luxurious one you envisioned.

Scenario 2: Mid-Level Earner – ₹10,000/month SIP, 12% return, 10 years

• Total invested: ₹12 lakh

• Nominal corpus: ≈ ₹23.23 lakh

• At 6% inflation: Real value ≈ ₹16.17 lakh

Shorter horizon amplifies the hit because compounding has less time to fight inflation.

Scenario 3: Aggressive Growth – ₹20,000/month SIP, 15% return (mid/small-cap tilt), 15 years, 5% inflation

• Total invested: ₹36 lakh

• Nominal corpus: ≈ ₹1.35 crore

• Real purchasing power: ≈ ₹80 lakh

Higher returns and slightly lower assumed inflation help, but you still lose ~40% in real terms compared to headline numbers.

Scenario 4: Debt/Conservative Hybrid – ₹5,000/month, 8% return, 20 years, 6% inflation

• Nominal corpus: ≈ ₹29.65 lakh

• Real value: ≈ ₹14.59 lakh

Debt funds struggle more visibly; real returns turn barely positive (~1.9%).

Scenario 5: High-Contribution Earner (Inspired by common 2026 data) – ₹25,000/month, 12% return, 10 years, 6% inflation

• Total invested: ₹30 lakh

• Nominal corpus: ≈ ₹58.08 lakh

• Real purchasing power: ≈ ₹40.41 lakh

These aren’t hypothetical—they’re derived from standard compounding math used by leading mutual fund platforms. Notice the pattern: Longer tenures and higher returns help close the gap, but inflation still claims 30-50% of apparent wealth in most cases. Step-up SIPs (increasing contribution 10-15% annually) can counter this effectively, but few investors model it properly.

What if inflation spikes to 8% (as in past decades)? Or drops to RBI’s 4% target? Our tool lets you slide these variables and compare side-by-side across 3-5 scenarios at once—something static calculators miss.

Visualizing Purchasing Power: What Your SIP Corpus Can Actually Buy

Let’s make it tangible with Indian goals:

• Child’s Higher Education (15 years horizon): ₹10,000 monthly SIP at 12% might grow nominally to ~₹46 lakh. At 6% inflation, real value ~₹25-28 lakh. But engineering/medical seats today cost ₹20-50 lakh; in 15 years? Easily double or triple with sector-specific inflation.

• Retirement Corpus: Target ₹2 crore nominal in 25 years? Real value might equate to only ₹70-80 lakh today’s buying power. Will that sustain ₹1 lakh monthly expenses (rising with inflation)?

• Dream Home Down Payment: A ₹50 lakh flat today might need ₹1 crore+ corpus slice. Inflation makes the gap wider.

These examples underscore why real-value tracking is non-negotiable. Historical data from 2000-2025 shows equity SIPs have outpaced inflation by 6-9% on average in real terms over long periods—but only if you stay invested and review periodically.

Introducing the Ultimate Multi-Scenario SIP Comparison Tool: Test, Compare, Conquer Inflation

Tired of spreadsheets or one-size-fits-all calculators that ignore inflation? That’s exactly why we built the SIP Real Value Calculator & Multi-Scenario Comparison Tool.

This free, intuitive tool lets you:

• Input multiple SIP amounts (₹1,000 to ₹1 lakh+ monthly)

• Test varied expected returns (8%, 12%, 15%, or custom)

• Adjust inflation assumptions (historical 6%, RBI 4%, or stress-test 8%)

• Vary tenures (5-30 years)

• Compare 3 scenarios side-by-side

• Instantly view: Total invested | Nominal corpus | Real purchasing power (today’s rupees) | Effective real return | Inflation-adjusted goal gap

No sign-up. No jargon. Just plug in numbers relevant to your life—perhaps one scenario for equity-heavy SIPs and another for balanced—and see charts that reveal the true picture. Thousands of investors in Gujarat and across India have already used it to recalibrate their plans, stepping up contributions or shifting to higher-growth funds.

Ready to see your SIP’s real future? Head straight to our SIP Comparison Calculator and run your custom scenarios in under 60 seconds. Discover exactly how inflation is (or isn’t) eating your corpus—and what small tweaks can protect it.

Proven Strategies to Beat Inflation and Protect Your SIP Corpus

1. Step-Up Your SIP Annually: Increase contributions by 10-15% every year to match salary growth and inflation. This alone can boost real corpus by 30-50% over decades.

2. Choose Equity Tilt for Long Horizons: Data shows equity SIPs deliver superior real returns (5-9% after inflation) over 10+ years versus debt.

3. Diversify Across Categories: Mix large-cap stability with mid-cap growth. Review every 6-12 months.

4. Inflation-Adjusted Goal Setting: Use the real-value calculator to back-solve required SIP amounts for specific targets.

5. Tax Efficiency: Equity SIPs held >1 year qualify for LTCG tax (12.5% above ₹1.25 lakh gains as of current rules)—far better than debt.

6. Emergency Buffer First: Don’t let inflation panic push you into over-risky bets. Maintain 6-12 months’ expenses in liquid funds.

7. Review & Rebalance: Markets and inflation evolve. Use tools like ours annually.

Common Myths Debunked

• “My 12% return beats inflation automatically.” Not in real terms over short periods.

• “Short-term SIPs are safe.” Inflation impact is sharper when time is limited.

• “Fixed deposits are inflation-proof.” They’re often not—even post-tax.

Conclusion: Take Control Before Inflation Takes Your Dreams

Inflation isn’t a villain—it’s an economic fact. But ignoring it in your SIP journey turns a powerful wealth-builder into a slow leak. By understanding nominal vs. real returns, studying real scenarios, and leveraging data-driven tools, you can ensure your corpus retains its purchasing power and grows meaningfully.

Don’t settle for impressive-looking statements. Demand real value. Open our multi-scenario SIP comparison tool right now, input your current SIP details alongside alternatives, and visualize the difference. Whether you’re a salaried professional in Ahmedabad saving for retirement or a parent planning education, this calculator empowers precise, inflation-aware decisions.

Your future self will thank you for seeing beyond the numbers—into the true purchasing power that matters. Start comparing scenarios today and build a SIP corpus that actually delivers the life you envision.

Frequently Asked Questions (FAQs) on Inflation and SIP Corpus

What is the difference between nominal returns and real returns in SIP investments?

Nominal returns are the headline growth figures shown by mutual fund apps and standard SIP calculators — for example, 12% annualized returns on your equity SIP. Real returns, however, adjust for inflation to show the actual increase in your purchasing power.

The simple formula is:

Real Return ≈ [(1 + Nominal Return) / (1 + Inflation Rate)] – 1

If your SIP delivers 12% nominal returns and inflation averages 6%, your real return is roughly 5.66%. This means while your corpus grows on paper, its ability to buy goods, services, education, or healthcare in the future is significantly lower. Our real value calculator instantly shows both nominal and inflation-adjusted figures side-by-side so you can see the true picture.

How does inflation actually eat into my SIP corpus over time?

Inflation steadily increases the cost of living, reducing what every future rupee can buy. Even if your SIP grows to ₹50 lakh in 15 years at 12% returns, at 6% average inflation that amount may only have the purchasing power of ₹20–25 lakh in today’s terms.

This erosion happens in two ways:

• The future corpus buys less than expected.

• Your fixed monthly SIP loses real value over time because your income (and expenses) usually rise with inflation, but the contribution amount stays the same unless you step it up.

Long-term historical data shows India’s average CPI inflation has hovered around 5–6% over the past two decades, with periods spiking higher. This is why simply looking at nominal corpus figures can create a false sense of security.

What is the current inflation rate in India (as of 2026), and what should I assume for long-term planning?

As of February 2026, India’s headline CPI inflation stood at 3.21% year-on-year, with food inflation contributing to recent movements. The RBI continues to target 4% inflation with a tolerance band of 2–6%. For conservative long-term SIP planning (10–25 years), most financial planners recommend assuming 5–6% average inflation, as this aligns with India’s historical trend (around 5.6–7.2% over recent decades).

You can stress-test higher (7–8%) or lower (4%) scenarios in our multi-scenario SIP comparison tool to see how sensitive your goals are to inflation changes.

Will equity SIPs always beat inflation?

Equity-oriented SIPs have historically delivered strong real returns over long periods (10+ years). When nominal returns average 12–15%, real returns after 5–6% inflation often land in the 6–9% range — significantly better than fixed deposits or savings accounts, which frequently deliver near-zero or negative real returns after tax and inflation.

However, “always” is not guaranteed in the short term. Markets are volatile, and there can be periods of underperformance. The key is staying invested for the full horizon and using rupee-cost averaging through SIPs. Equity SIPs remain one of the most effective ways for Indian investors to build real wealth over time, but diversification and periodic review are essential.

How can a step-up SIP help me protect my corpus from inflation?

A step-up SIP automatically increases your monthly contribution by a fixed percentage (commonly 10–15%) every year. This mirrors typical salary growth and rising living costs, ensuring you invest more as inflation pushes expenses higher.

Example: Starting with ₹5,000 monthly and stepping up by 10% annually can significantly boost your final corpus compared to a flat SIP — often by 30–60% or more over 15–20 years — while keeping the increases manageable. Many investors find this the single most effective way to maintain or improve real purchasing power. Our calculator lets you model step-up scenarios alongside different inflation rates for clear comparisons.

Why do most standard SIP calculators show misleading results?

Most basic SIP calculators only display nominal future value without adjusting for inflation. They show impressive-looking corpus numbers (e.g., “₹1 crore in 20 years”) but ignore how much that money will actually buy when you need it.

An inflation-adjusted or real-value calculator reveals the gap and helps you set realistic goals. That’s why our SIP real value calculator with multi-scenario comparison was built — to let you test multiple combinations of investment amount, expected return, inflation rate, tenure, and step-up options in one view.

How do I calculate the real purchasing power of my SIP corpus?

You need three main inputs:

• Monthly SIP amount (or step-up details)

• Expected nominal return

• Assumed average inflation rate

• Investment tenure

The calculator compounds your investments at the nominal rate, then discounts the final corpus back using the inflation rate to express it in today’s rupees. This gives you the inflation-adjusted (real) value. You can also view the effective real annualized return. Try different combinations directly in our free tool to understand various outcomes.

Is it better to use a debt fund SIP or equity SIP when worrying about inflation?

For horizons longer than 7–10 years, equity or equity-oriented hybrid SIPs generally deliver superior real returns because they have the potential to outpace inflation by a healthy margin. Debt funds (or conservative hybrids) typically offer 6–8% nominal returns, which often translate to very low or even negative real returns after 5–6% inflation and taxes.

Use debt SIPs for short-term goals or as a stabilizer in your overall portfolio, but rely on equity for long-term wealth creation and inflation beating.

How often should I review my SIPs in the context of inflation?

Review your SIP portfolio at least once a year, or whenever there is a significant change in your income, goals, or economic outlook. Check whether your current contributions (with step-ups if any) are on track to meet inflation-adjusted goals. Use our multi-scenario tool annually to re-run projections with updated inflation expectations and returns. Rebalance your fund allocation if needed, but avoid frequent churning.

Can your SIP comparison calculator help me plan specific goals like retirement or child education?

Absolutely. Our tool is designed for goal-based planning. You can input your target corpus in today’s rupees (inflation-adjusted), then work backwards or forward to see required monthly SIPs under different return and inflation scenarios. Test conservative, moderate, and aggressive assumptions side-by-side. Many users in cities like Ahmedabad and across India use it to fine-tune retirement, education, or home-buying plans.

What are realistic expected returns for SIPs in India?

For diversified equity funds (large-cap, flexi-cap, multi-cap), long-term (10+ years) annualized returns have historically ranged between 12–15% in many periods, though past performance is not a guarantee. Mid- and small-cap categories can deliver higher but with greater volatility. Debt funds usually range 6–8%. Always use conservative estimates (10–12% for equity) when planning, and focus more on real returns after inflation.

Does taxation affect real returns on SIPs?

Yes. For equity mutual funds, long-term capital gains (holding period >1 year) are taxed at 12.5% above ₹1.25 lakh per year (as per current rules). This slightly reduces net real returns. Debt fund gains are taxed as per your slab. Factor this in when estimating net real purchasing power. Equity SIPs still tend to offer better post-tax, post-inflation returns over long horizons compared to most alternatives.

Final Tip from the FAQs

Inflation is a silent but persistent force. The best defense is awareness combined with action — using step-up SIPs, choosing growth-oriented funds for long-term goals, and regularly tracking real (not just nominal) progress.

Don’t rely on guesswork. Test your current SIPs and alternative scenarios right now with our free multi-scenario SIP comparison and real value calculator. Input different monthly amounts, returns, inflation rates, and tenures to see exactly how inflation impacts your corpus — and what small changes can do to protect your purchasing power.

Have more questions? Feel free to reach out or drop your specific numbers in the calculator comments. Staying informed and proactive is the smartest way to ensure your SIP corpus actually delivers the future you’re working toward.

Select Your Favorite Section