Why Most Indians Struggle With Money (Even With Good Income)

In India today, earning a decent salary is no longer enough to build wealth.

You’ll find people earning ₹50,000, ₹1 lakh—even ₹3 lakh per month—still feeling financially stressed.

Why?

Because financial success isn’t driven by income alone.

It’s driven by behavior, habits, and decisions made in everyday life.

Most people don’t realize where they’re going wrong because:

- Their mistakes feel “normal”

- They follow what everyone else is doing

- There’s no clear feedback system like a “financial health score”

That’s why case studies are powerful.

Instead of theory, you’ll see real-life scenarios that mirror your own financial decisions.

Let’s break down 7 such situations—and more importantly, how to fix them.

📩 Unlock Your Score

🧾 1. The Income Trap: “I Earn Well But Save Almost Nothing”

Case Study:

Rohit earns ₹60,000/month in a metro city. Despite a stable income, he barely saves ₹2,000–₹3,000 at the end of the month.

🔍 What’s Really Happening?

This is one of the most common financial traps:

- Lifestyle inflation (expenses rise with income)

- No fixed savings strategy

- Spending first, saving later

This pattern creates an illusion:

“I’m earning well, so I’m doing fine.”

But in reality, wealth is not being created at all.

⚠️ Why This Is Dangerous

- No buffer for emergencies

- No investments → no compounding

- Financial stress despite income growth

- Dependency on salary forever

✅ The Fix: Reverse Your Money Flow

Instead of:

Income → Expenses → Savings (if any)

Switch to:

Income → Savings → Expenses

Practical Steps:

- Set a minimum 20% savings target

- Automate transfers to savings/investment accounts

- Track expenses for 30 days (eye-opening exercise)

💡 Key Insight:

Your savings rate matters more than your salary.

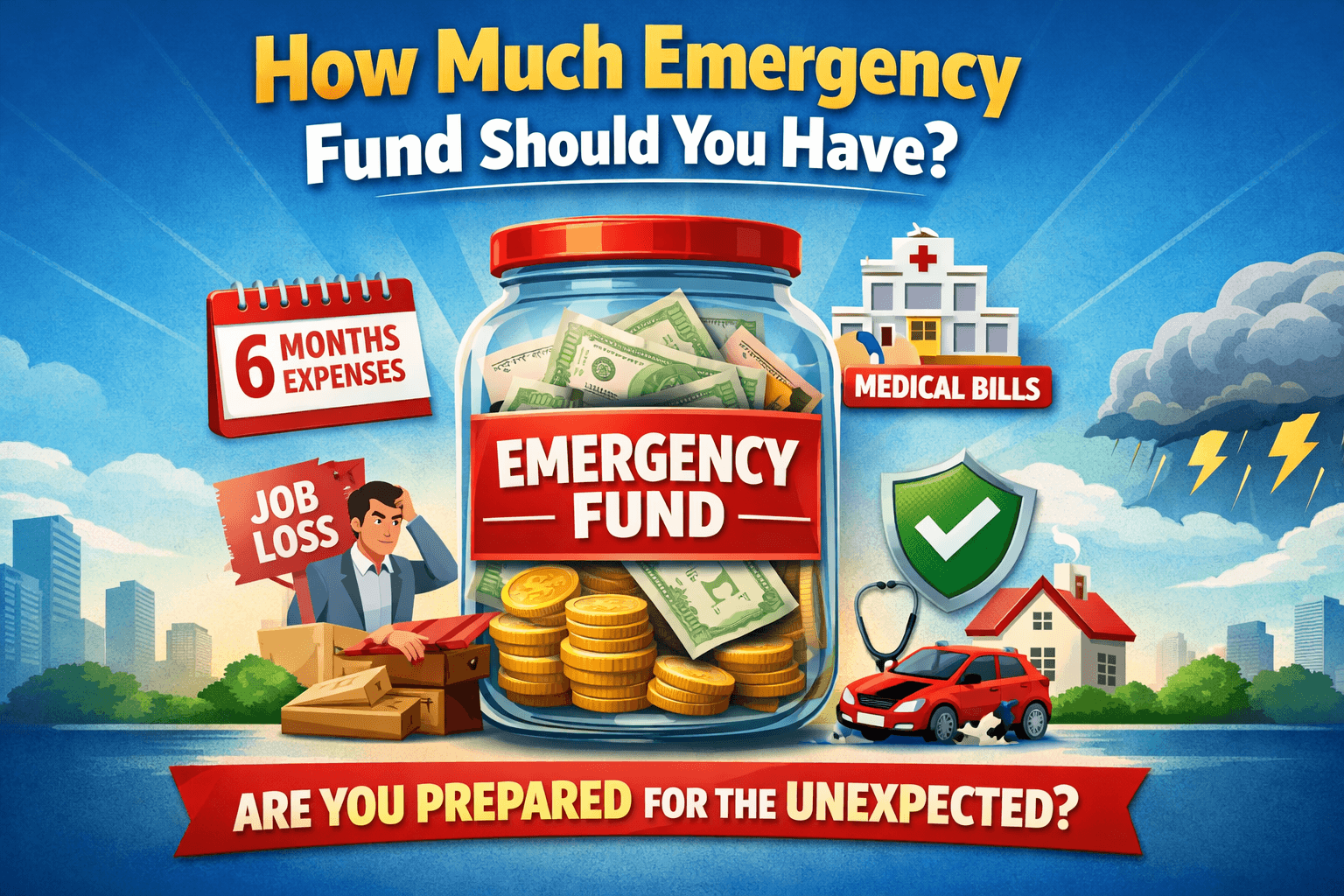

🏥 2. The Emergency Illusion: “I Had Savings, But It Wasn’t Enough”

Case Study:

Priya had ₹1 lakh saved. A sudden medical emergency cost ₹80,000.

🔍 What Went Wrong?

On the surface, Priya did everything right—she saved money.

But she lacked:

- A structured emergency fund

- Risk protection (health insurance)

⚠️ The Real Risk

- 80% of savings wiped out instantly

- Next emergency = debt

- Financial progress reset to zero

In India, medical inflation is rising rapidly. A single hospitalization can derail years of savings.

✅ The Fix: Build a Safety Net First

Step 1: Emergency Fund

- Target: 3–6 months of expenses

- Keep it in liquid funds or savings account

Step 2: Health Insurance

- Minimum ₹5–10 lakh cover

- Essential even if your employer provides coverage

💡 Key Insight:

Savings without protection is like driving without insurance.

📉 3. The Panic Investor: “Market Fell, I Want to Exit”

Case Study:

Amit invested in mutual funds. The market fell 20%, and he wants to withdraw.

🔍 What’s Happening Psychologically?

- Fear of losing money

- Lack of understanding of market cycles

- Short-term thinking

⚠️ The Biggest Mistake

Selling during a fall:

- Locks in losses

- Misses recovery

- Breaks long-term wealth creation

📊 Reality Check

Markets:

- Fall in the short term

- Grow in the long term

Historically, every major fall has been followed by recovery and growth.

✅ The Smart Strategy

- Continue SIP (you’re buying at lower prices)

- Stay invested for long-term goals (5–10+ years)

- Avoid checking portfolio daily

💡 Key Insight:

The biggest risk in investing is not volatility—it’s emotional decisions.

💳 4. The Credit Card Trap: “I Pay Only Minimum Due”

Case Study:

Neha pays only the minimum due on her credit card every month.

🔍 What Most People Don’t Realize

Credit card interest rates in India:

👉 30%–40% annually

This is one of the most expensive forms of debt.

⚠️ What This Leads To

- Debt snowballing quickly

- Paying mostly interest, not principal

- Long-term financial drain

📉 Example

₹1 lakh unpaid → can double in just a few years if only minimum payments are made.

✅ The Fix

- Pay full outstanding amount immediately

- Stop using credit card temporarily

- Convert to EMI only if necessary (lower interest)

💡 Key Insight:

Compounding can build wealth—or destroy it through debt.

🏠 5. The EMI Burden: “Half My Income Goes Into Loans”

Case Study:

Rahul’s EMIs consume 45% of his monthly income.

🔍 What’s Going Wrong?

- Over-borrowing

- Lifestyle upgrades through loans

- Poor financial planning

⚠️ Risks

- No room for savings

- Constant cash flow pressure

- High stress and dependency

📊 Ideal Rule

👉 Keep total EMIs below 30% of income

✅ How to Fix It

- Prepay high-interest loans

- Avoid unnecessary EMIs (gadgets, lifestyle purchases)

- Increase income streams

💡 Key Insight:

Debt should support your goals—not control your life.

🛡 6. The Protection Gap: “I Have Money But No Insurance”

Case Study:

Karan has ₹5 lakh in savings but no health insurance.

🔍 The Hidden Risk

Many Indians think:

“I have savings, I’ll manage.”

But healthcare costs can:

- Wipe out savings instantly

- Force borrowing

⚠️ Reality in India

- Surgeries can cost ₹2–10 lakh

- Private hospital expenses rising yearly

✅ Correct Priority Order

- Health insurance

- Term life insurance

- Emergency fund

- Investments

💡 Key Insight:

Wealth protection comes before wealth creation.

👴 7. The Delay Trap: “I’ll Start Retirement Later”

Case Study:

Anjali is 35 and hasn’t started retirement planning.

🔍 What’s Happening?

- No urgency

- Underestimating compounding

- Prioritizing short-term expenses

⚠️ The Cost of Delay

Starting late means:

- Higher monthly investment required

- Lower final corpus

- Increased financial pressure

📊 Simple Comparison

| Start Age | Monthly Investment Needed |

|---|---|

| 25 | ₹5,000 |

| 35 | ₹15,000+ |

(For similar retirement goals)

✅ The Fix

- Start immediately (even small SIP)

- Increase contributions over time

- Focus on equity for long-term growth

💡 Key Insight:

Time is the most powerful wealth-building tool you have.

🔥 Common Patterns Across All 7 Mistakes

If you look closely, all these scenarios share common themes:

❌ What People Get Wrong:

- No financial planning

- Emotional decision-making

- Ignoring risks

- Delaying important actions

- Over-reliance on income

✅ What Financially Smart People Do:

- Save consistently

- Invest regularly

- Manage debt carefully

- Protect with insurance

- Think long-term

📊 Why You Need a Financial Health Score

Most people don’t know:

- Where they stand financially

- What they’re doing right or wrong

- What to fix first

That’s where a Financial Health Score helps.

It gives you:

- A clear number (0–100)

- A diagnosis of your finances

- A step-by-step improvement plan

🎯 Final Thoughts

Financial success is not about:

- Being rich

- Earning a high salary

- Timing the market

It’s about:

Making better decisions consistently over time.

💡 Ask Yourself Honestly:

- Are you saving enough?

- Are you protected against risks?

- Are you investing consistently?

- Are you managing debt well?

🚀 Next Step

Want to know where YOU stand?

👉 Get your Financial Health Score in 60 seconds

👉 Identify your biggest money mistakes

👉 Get a personalized action plan

FAQs

What are the most common personal finance mistakes in India?

The most common mistakes include:

Not saving enough

No emergency fund

Investing without knowledge

High credit card debt

Ignoring insurance

Delaying retirement planning

These small mistakes compound over time and significantly impact long-term wealth.

How much should I save from my salary in India?

Ideally, you should save at least 20% of your monthly income.

If you’re just starting, aim for 10% and gradually increase.

How big should an emergency fund be?

An ideal emergency fund should cover 3 to 6 months of your living expenses.

For unstable jobs or self-employed individuals, aim for 6–12 months.

Is it better to save or invest first?

You should:

Build an emergency fund

Get insurance

Then start investing

Saving provides safety; investing builds wealth.

What is the biggest mistake new investors make?

The biggest mistake is reacting emotionally to market movements, especially:

Selling during market crashes

Stopping SIPs

Long-term consistency is key.

How dangerous is paying only the minimum due on a credit card?

Very dangerous.

Credit cards charge 30–40% annual interest, which can quickly trap you in debt.

What is a safe EMI-to-income ratio?

Your total EMIs should ideally be below 30% of your monthly income.

Anything above 40% is considered risky.

Do I really need health insurance if I have savings?

Yes, absolutely.

Medical emergencies can wipe out your savings quickly. Insurance protects your wealth.

When should I start retirement planning?

As early as possible.

Starting in your 20s or early 30s allows compounding to work in your favor.

How much should I invest for retirement in India?

It depends on your lifestyle, but a common rule is:

Aim for a corpus of 25–30x your annual expenses

What is the difference between saving and investing?

Saving = keeping money safe (low risk, low return)

Investing = growing money (higher risk, higher return)

Both are essential for financial health.

Why do high-income earners still struggle financially?

Because:

They spend more as income increases

They don’t save or invest consistently

They rely only on income, not assets

Income alone doesn’t guarantee wealth.

What is lifestyle inflation and why is it harmful?

Lifestyle inflation is when your expenses increase as your income increases.

It prevents wealth creation because you never increase your savings rate.

How can I improve my financial health quickly?

Start with these steps:

Track your expenses

Increase savings rate

Reduce high-interest debt

Start SIP investments

Get insurance coverage

What is a Financial Health Score?

A Financial Health Score is a 0–100 score that measures:

Savings

Investments

Debt

Insurance

Financial habits

It gives a clear picture of your financial condition.

What is a good Financial Health Score?

80+ → Excellent

60–80 → Stable

Below 60 → Needs improvement

How can I calculate my Financial Health Score?

You can calculate it using tools that evaluate:

Savings ratio

Debt levels

Investment habits

Risk protection

👉 Or use an online Financial Health Score calculator for a quick result.

What should I fix first: debt, savings, or investing?

Priority order:

High-interest debt (credit cards)

Emergency fund

Insurance

Investing

Select Your Favorite Section

{kind=link}