“Most Indians track their mutual fund returns. Very few track their financial life.”

That gap — between knowing your returns and knowing your reality — is exactly what Wealthpedia’s Personal Finance OS was built to close.

Why Your Financial Tools Are Failing You

You probably already use some financial tools. A SIP calculator here. An EMI calculator there. Maybe a budgeting app on your phone.

But here’s the hard truth: isolated tools produce isolated thinking.

When you calculate your SIP in one place, your EMI in another, and your retirement goal in a third, you’re not doing financial planning — you’re doing financial guessing. You have no idea how your loan is killing your investment capacity. You have no idea whether your SIP is enough for your actual goals. You have no idea how far or how close you are to financial freedom.

That’s the problem Wealthpedia’s Personal Finance OS solves — completely, systematically, and for free.

This is not a collection of calculators. This is an operating system for your financial life — one that takes you through a deliberate, sequenced journey from awareness all the way to freedom.

What Is Wealthpedia’s Personal Finance OS?

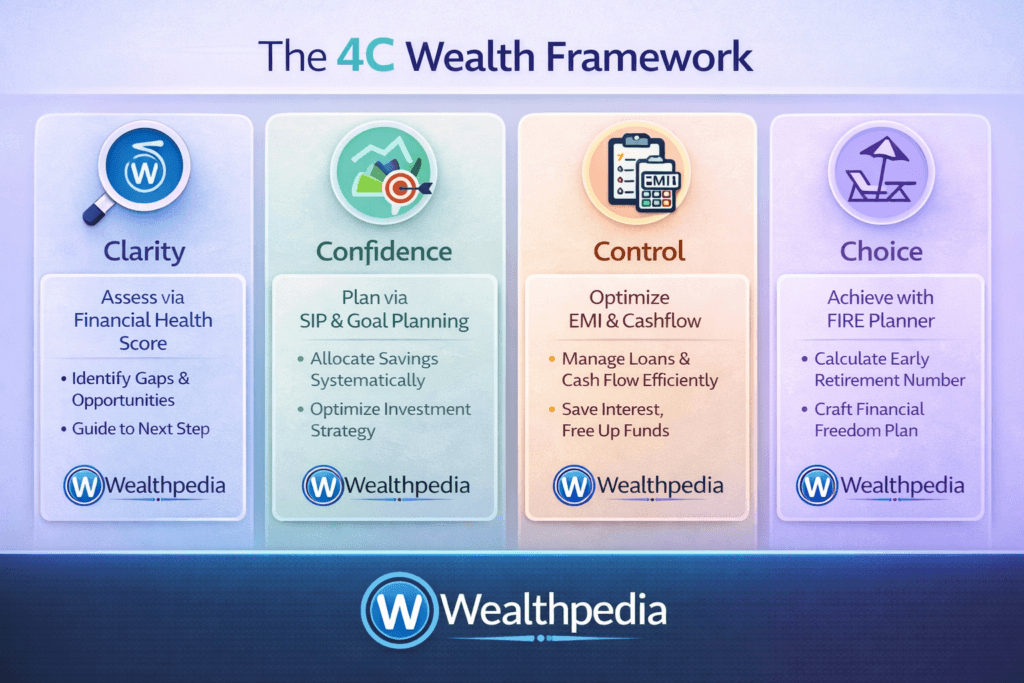

Wealthpedia’s Personal Finance OS is a structured, four-tool ecosystem built around a single philosophy: personal finance is not a math problem — it’s a transformation journey.

Most tools in India help you calculate. Wealthpedia’s OS helps you transform.

It is built on what we call the 4C Framework — four sequential stages that mirror how financial transformation actually works in real life:

Clarity → Confidence → Control → Choice

Each stage has a dedicated, deeply engineered tool. Each tool feeds insight into the next. The output of one becomes the input for another. Together, they form a complete financial operating system — the first of its kind built specifically for Indian users.

Here’s the architecture at a glance: Stage Core Emotion Tool What It Does Clarity Awareness Financial Health Score Diagnoses your entire financial life in one score Confidence Growth SIP Comparison Calculator Builds a concrete wealth-creation plan Control Stability EMI Pro Calculator Optimises debt and improves monthly surplus Choice Freedom Multi-Goal FIRE Planner Maps your path to financial independence

The 4C Framework: A Deep Dive

C1 — Clarity: “Understand Your Financial Reality”

Tool: Financial Health Score

Before you can improve anything, you must see it clearly. The Financial Health Score is Wealthpedia’s diagnostic engine — think of it as a credit score for your entire financial life, not just your borrowing history.

It evaluates seven pillars simultaneously and outputs a single score between 0 and 100:

- Cash flow health — Are you living within your means?

- Savings rate — What percentage of your income is actually being saved?

- Debt-to-income ratio — How much of your income is going toward EMIs?

- Emergency fund adequacy — Can you survive 3–6 months without income?

- Investment coverage — Are your investments consistent, diversified, and goal-aligned?

- Net worth position — Assets minus liabilities: where do you actually stand?

- Insurance and risk protection — Are you protected against life’s financial shocks?

The scoring model is weighted — similar to how SEBI-registered advisors assess client portfolios — with savings rate, debt ratio, and emergency fund receiving the highest weightage.

Score interpretation:

- 80–100: Excellent — you are building real wealth

- 70–79: Good — strong foundation, minor optimisation needed

- 50–69: Average — visible gaps requiring action

- Below 50: Critical — significant vulnerabilities, immediate attention needed

What makes this genuinely different from a bank’s “financial fitness quiz” is that it doesn’t ask you how you feel about your finances. It asks for your actual numbers — and calculates the truth.

The Clarity Outcome: You walk away knowing exactly where you are strong, where you are vulnerable, and which lever — if pulled first — will produce the biggest improvement. That’s the foundation every other step is built on.

C2 — Confidence: “Build Wealth With a Clear Plan”

Tool: SIP Comparison Calculator

Once you know your financial reality, the natural next question is: “How do I start building wealth systematically?”

The SIP Comparison Calculator answers that — but not in the way a regular SIP calculator would. This is India’s first 2-in-1 SIP Comparison + Goal Planner Calculator, and the distinction matters enormously.

Most SIP calculators ask: “If I invest ₹X, what will I get?” That’s one question, one scenario, one answer.

Wealthpedia’s SIP Comparison Calculator puts multiple scenarios side-by-side in a single live-updating table, so you can see trade-offs instantly.

What it does that no other Indian tool does (verified as of 2026):

- Compares 3, 5, or 10 different SIP amounts across three return rates (Conservative, Moderate, Aggressive — all editable) simultaneously

- Shows projected corpus, inflation-adjusted real value, and wealth multiple for each scenario

- One toggle flips the entire table from SIP Mode (“what will my SIP grow into?”) to Goal Planner Mode (“how much SIP do I need for this goal?”) — same table, instant transformation

- Supports Step-Up SIP simulation, so you model salary hikes automatically

- Updates every cell in real time as you type — no Calculate button, no waiting

The Confidence Outcome: You stop wondering “Am I investing enough?” and start knowing exactly what your current SIP will produce, what you need to invest to hit specific goals, and how much difference even a 2% better return makes over 20 years. That knowledge builds genuine investment confidence.

C3 — Control: “Optimise Cash Flow and Debt”

Tool: EMI Pro Calculator

Here’s a reality most financial content ignores: your debt is directly reducing your wealth-building capacity. Every rupee going toward unnecessary interest is a rupee not compounding in your SIP.

The EMI Pro Calculator is designed to give you complete control over your debt — and to show you the true, full cost of every loan you carry or plan to take.

This is not a basic EMI calculator. This is India’s first comprehensive loan intelligence system, combining features that exist separately — if at all — across multiple platforms:

Key capabilities:

- Four loan types with smart presets: Home, Car, Personal, and Education loans — each loading India-specific interest rate defaults and tax rules automatically

- Loan Health Score (unique in India): Instantly computes a 0–100 score based on your EMI-to-income ratio, interest rate, and tenure. Red means rethink. Green means go ahead.

- Full Prepayment Simulator: Three modes — Lump Sum, Annual, and Extra EMI every month — with two goals: reduce tenure or reduce EMI. Shows exact interest saved and months eliminated.

- Tax Benefits Engine: Auto-applies Section 80C, 24(b), and 80E based on loan type and your tax slab. Shows year-wise tax savings — something no bank calculator will show you proactively.

- Step-Up EMI Simulator: Increase your EMI by 5–30% annually (mirroring salary hikes) and see how it collapses your loan tenure and interest burden.

- What-If Explorer: Three scenario modes — Rate Comparison, Tenure Trade-offs, and Step-Up projections — with dual-axis charts.

- Full Amortization Schedule: Yearly and monthly, searchable, with every rupee accounted for.

A practical example: A ₹50 lakh home loan at 8.5% for 20 years seems manageable at ₹43,186/month. But the EMI Pro Calculator shows you that you will pay ₹53.6 lakh in interest alone over the life of the loan. A single ₹2 lakh prepayment in year one saves ₹4.8 lakh and closes the loan 14 months early. That’s control — and most borrowers never see this picture.

The Control Outcome: You stop being a passive borrower and become an active loan manager. You reduce interest leakage, improve monthly surplus, and free up capital for wealth creation. Control over cash flow is the bridge between planning and freedom.

C4 — Choice: “Achieve Financial Freedom”

Tool: Multi-Goal FIRE Planner

The final stage is the most powerful: bringing everything together into a single, unified plan for financial independence.

The Multi-Goal FIRE Planner is not just a retirement calculator. It’s a complete financial life simulator that answers the question every middle-class Indian family is actually trying to answer: “I can only save ₹60,000 a month. How do I fund my child’s education in 10 years, buy a house in 5 years, and still retire at 55 with dignity?”

What makes it categorically different from any other FIRE or goal calculator in India:

- Single SIP, multiple goals: You enter one monthly investment capacity. The tool distributes it across all your goals using a smart waterfall allocation engine — priority-based, sequential, and dynamic.

- Unlimited goals with priority ranking: Add as many goals as your life requires. Assign priorities. The engine funds your highest-priority goal first, then moves down.

- FIRE fully integrated with goals: Your retirement corpus is the final goal in the waterfall — not a separate calculation in a separate tool.

- LTCG tax-aware withdrawals: Most FIRE calculators ignore the 12.5% LTCG tax on equity redemptions. This one grosses up your required corpus so your post-tax monthly income actually matches your lifestyle expenses.

- Step-Up SIP with live preview: Year 1: ₹60,000 → Year 5: ₹87,000 → Year 10: ₹1,17,000. Real-life modelling, not static assumptions.

- Portfolio journey chart till age 100: A single visual showing your wealth accumulating (green) and then being drawn down through retirement (gold) — all the way to age 100. No other free Indian tool offers this.

- Instant what-if analysis: Change a priority, delay a goal by two years, increase SIP by ₹10,000 — everything recalculates instantly.

The Choice Outcome: You can see your freedom timeline clearly. You know exactly what your current SIP produces, what trade-offs exist between your goals, whether you’re on track or short, and what specific adjustments close the gap. This is where financial discipline becomes financial freedom.

The Flow: How the Four Tools Work Together

This is what makes Wealthpedia’s Personal Finance OS more than a set of tools — it’s a sequential system where each stage feeds the next.

A real example of the flow in action:

Meet Arjun, 34, software engineer in Bangalore, monthly take-home ₹1.8 lakh.

- Clarity: His Financial Health Score is 52. Strong income and investments, but DTI is 38% (too high), emergency fund covers only 1.5 months (dangerously low), and savings rate is 15% (below ideal).

- Confidence: The SIP Calculator shows that with a ₹25,000/month SIP at 12% return over 20 years, he builds ₹2.5 crore. But with a 10% annual step-up, the same starting SIP grows to ₹5.1 crore — a 2× improvement from habit alone.

- Control: The EMI Pro Calculator reveals his ₹40,000 home loan EMI can be shortened by 4.5 years with a ₹3 lakh lump-sum prepayment, saving ₹8.2 lakh in interest. That frees up his EMI headroom within 5 years, which can redirect to his SIP.

- Choice: The FIRE Planner shows him that with his current plan, he reaches FIRE at 57. But by increasing his SIP step-up from 10% to 15% and prepaying his loan as planned, the FIRE timeline moves to age 52 — five years of his life, back in his hands.

That’s the Personal Finance OS at work.

How to Use Wealthpedia’s Personal Finance OS: Step-by-Step Guide

Step 1: Start With Your Financial Health Score

Time required: 10–15 minutes

What to prepare: Bank statements or a rough mental inventory of income, expenses, savings, investments, loans, and insurance

Go to the Financial Health Score and enter:

- Monthly income (all sources)

- Monthly expenses (fixed + variable)

- Total savings and investments

- Outstanding loan amounts

- Emergency fund amount

- Insurance details (health + term life)

Get your score. Read the pillar-by-pillar breakdown. Screenshot or note which areas are weakest — these are your starting priorities.

Re-do this every 6–12 months to track progress.

Step 2: Build Your Investment Plan With the SIP Calculator

Time required: 5–10 minutes

What to prepare: Your investment goals and rough monthly SIP capacity (derived from surplus identified in Step 1)

Go to the SIP Comparison Calculator and:

- Set your investment horizon (years)

- Enable Step-Up SIP (10% annual increase is realistic for most salaried professionals)

- Enter 3–5 different SIP amounts to compare

- Toggle to Goal Planner Mode: enter your target corpus amounts for key goals (child’s education, home purchase, retirement) and see exact monthly SIP required at conservative, moderate, and aggressive returns

This gives you a clear investment benchmark — the minimum monthly SIP you should be running to achieve your goals.

Step 3: Optimise Your Debt With the EMI Pro Calculator

Time required: 10–20 minutes

What to prepare: Loan statements — amount outstanding, interest rate, remaining tenure, and your monthly income

Go to the EMI Pro Calculator and:

- Select your loan type (Home / Car / Personal / Education)

- Enter the four core inputs: loan amount, rate, tenure, monthly income

- Check your Loan Health Score — if below 60, your debt load is risky

- Go to the Prepayment tab and simulate: what does a ₹1 lakh or ₹2 lakh prepayment do to your total interest?

- Check the Tax tab — are you maximising your Section 80C and 24(b) deductions?

- Run the Step-Up EMI simulation — if your salary grows 8–10% annually, increasing your EMI proportionally can close your loan years earlier

Note the interest savings you can unlock. Redirect that surplus capacity to your SIP from Step 2.

Step 4: Build Your Complete Financial Freedom Plan

Time required: 15–20 minutes

What to prepare: Your goal list (education, home, marriage, retirement), current portfolio value, and monthly investment capacity

Go to the Multi-Goal FIRE Planner and:

- Enter monthly SIP capacity, current portfolio, age, return assumptions, and inflation

- Enable Step-Up SIP

- Enable FIRE Mode: enter desired retirement age, current monthly expenses, and safe withdrawal rate (3% recommended for India)

- Add all your goals with priorities (P1 = most critical)

- Watch the waterfall allocation engine distribute your SIP across goals

- Study the portfolio journey chart — your entire financial life, accumulation through retirement, in one visual

- Play “what if”: delay a goal, increase SIP, change FIRE age — watch trade-offs instantly

This is your living financial plan. Revisit it annually or whenever a major life event occurs.

What Makes Wealthpedia’s Personal Finance OS Stand Out

1. It’s a System, Not a Collection

Every other platform — Groww, ET Money, BankBazaar, Zerodha — offers calculators. Wealthpedia offers a sequenced transformation framework. The tools are designed to feed each other, not sit independently.

2. It’s Built for Indian Reality

Western financial tools assume stable income, low inflation, no joint family obligations, and simple tax rules. Wealthpedia’s OS is built for:

- India’s 6%+ general inflation and 10–14% healthcare inflation

- Joint family financial obligations

- EMI-heavy household balance sheets

- LTCG tax on equity withdrawals

- Section 80C, 24(b), and 80E deduction optimisation

- SIP-based investing as the primary wealth-creation vehicle

3. No Logins. No Data Storage. No Upsells.

Every tool is 100% free. No email capture. No data stored on servers. No hidden subscriptions. Your numbers stay on your device. This is a rare commitment in a landscape where most “free” tools are lead-generation funnels.

4. Real-Time, No “Calculate” Button

Every tool updates live as you type. This isn’t just a UX choice — it fundamentally changes how people interact with financial scenarios. You explore, experiment, and discover trade-offs in real time, the way planning should actually feel.

5. Depth That Matches Professional Advisor Tools

The weighted scoring model in the Financial Health Score mirrors SEBI advisor methodology. The waterfall allocation engine in the FIRE Planner is how professional financial planners actually structure multi-goal portfolios. The LTCG tax gross-up in FIRE withdrawals is something even most paid tools ignore. This is advisor-grade logic, democratised.

Comparison: Wealthpedia’s Personal Finance OS vs. Existing Tools

| Feature | Wealthpedia OS | Groww | ET Money | BankBazaar | NPS / AMFI Tools |

|---|---|---|---|---|---|

| Holistic Financial Health Score | ✅ 7-pillar, quantitative | ❌ | ❌ | ❌ | ❌ |

| SIP Side-by-Side Multi-Scenario Comparison | ✅ Live, unlimited rows | ❌ (Single scenario) | ❌ (Single scenario) | ❌ | ❌ |

| SIP + Goal Planner (One Toggle) | ✅ India’s first | ❌ | ❌ | ❌ | ❌ |

| Step-Up SIP Simulation | ✅ | ✅ (Some) | ✅ (Some) | ❌ | ❌ |

| Loan Health Score (EMI/Income Ratio) | ✅ Unique | ❌ | ❌ | ⚠️ Basic | ❌ |

| Prepayment Simulator (3 Modes) | ✅ | ❌ | ❌ | ⚠️ Basic | ❌ |

| Tax Savings Engine (80C, 24b, 80E) | ✅ Year-wise | ❌ | ❌ | ⚠️ Partial | ❌ |

| Step-Up EMI Simulator | ✅ | ❌ | ❌ | ❌ | ❌ |

| Multi-Goal + FIRE in One Tool | ✅ Waterfall engine | ❌ (Separate tools) | ❌ (Separate tools) | ❌ | ❌ |

| LTCG Tax on FIRE Withdrawals | ✅ | ❌ | ❌ | ❌ | ❌ |

| Portfolio Journey to Age 100 | ✅ | ❌ | ❌ | ❌ | ❌ |

| Priority-Based Goal Allocation | ✅ | ❌ | ❌ | ❌ | ❌ |

| 100% Free / No Login / No Data Storage | ✅ | ⚠️ Partial | ⚠️ Partial | ❌ | ✅ |

| System Thinking (Integrated Tools) | ✅ | ❌ | ❌ | ❌ | ❌ |

Verdict: No single platform in India — free or paid — currently offers this combination of diagnostic depth, planning breadth, and system-level integration.

Who Is This For?

Wealthpedia’s Personal Finance OS is built for every Indian who earns, spends, saves, borrows, or invests — which is to say, everyone. But it’s particularly transformative for:

Salaried professionals (25–45) who have income but feel like they’re not getting ahead fast enough. The OS reveals the leaks and the levers.

Business owners and freelancers with irregular income who need to understand their true financial health beyond the good months.

Young earners (22–30) starting their financial journey. The earlier you run through the 4C Framework, the more powerful the compounding effect of getting it right early.

EMI-heavy households carrying multiple loans who feel financially squeezed despite reasonable incomes. The Control stage alone can free up significant monthly surplus.

FIRE aspirants who want to retire early but have no clear, unified plan that accounts for multiple goals simultaneously.

Families planning major milestones — children’s education, home purchase, wedding, parental healthcare — who need to see all goals in one coherent plan.

The Philosophy Behind the OS: Why “Operating System” Is the Right Metaphor

Your phone’s operating system doesn’t do one thing. It manages memory, runs applications, coordinates hardware, and provides a consistent environment for everything to work together.

That’s exactly what a personal finance OS should do.

Right now, most Indians run their finances like they’re running apps without an OS. The SIP app doesn’t talk to the EMI app. The EMI app doesn’t talk to the retirement calculator. Everything is siloed. Decisions are made in isolation.

Wealthpedia’s Personal Finance OS creates the connective tissue — a framework where each decision is made with awareness of how it affects everything else. Your loan optimisation informs your SIP capacity. Your SIP capacity informs your goal timeline. Your goal timeline informs your FIRE date.

This is how wealth is actually built: not through a series of isolated good decisions, but through a coherent system that compounds those decisions over time.

Unique Features Summary: What You Won’t Find Anywhere Else

From the Financial Health Score:

- 7-pillar, quantitative (not survey-based) financial diagnosis

- Weighted scoring model aligned with SEBI advisor methodology

- India-specific benchmarks for savings rate, DTI, and emergency fund adequacy

From the SIP Comparison Calculator:

- Live, multi-row, multi-return side-by-side comparison (India’s first)

- Instant 2-in-1 toggle: SIP Mode ↔ Goal Planner Mode (India’s first)

- Step-Up SIP + inflation adjustment in both modes simultaneously

From the EMI Pro Calculator:

- Loan Health Score with EMI-to-income ratio (unique in India)

- Three prepayment modes (lump-sum, annual, extra EMI) with two optimisation goals

- Tax engine covering all three relevant sections (80C, 24b, 80E) with year-wise charts

- Step-Up EMI simulator modelling salary growth impact on loan closure

From the Multi-Goal FIRE Planner:

- Priority-based waterfall allocation across unlimited goals (India’s first free tool)

- FIRE fully integrated with life goals — not a separate calculation

- LTCG tax gross-up on withdrawal phase (extremely rare in free tools)

- Portfolio journey chart accumulation + decumulation to age 100 (unique)

- Instant what-if scenario modelling across all inputs simultaneously

Frequently Asked Questions

What is the 4C Framework and why does the order matter?

The 4C Framework — Clarity, Confidence, Control, Choice — represents the natural sequence of financial transformation. You cannot build confidence in a plan without first having clarity about your current reality. You cannot exercise true choice (financial freedom) without first gaining control over cash flow. The order isn’t arbitrary; it mirrors the cognitive and practical sequence of real financial improvement.

Do I need to use all four tools, or can I use them independently?

Each tool works standalone and delivers significant value on its own. But the full power of the OS emerges when you use them sequentially — because insights from each tool directly inform decisions in the next. The system is designed so that the output of Stage 1 (what’s weak in my financial health?) becomes the input for Stage 2 (how do I build my investment plan to fix it?).

How often should I run through the full 4C Framework?

At minimum, once a year — ideally around the start of the financial year (April) or after a major life event like a salary hike, new loan, job change, or new financial goal. Some users revisit individual tools quarterly for specific monitoring.

Is Wealthpedia’s Personal Finance OS suitable for beginners with no finance background?

Absolutely. The tools are designed so that a 23-year-old with their first salary can use them without financial jargon confusion. The scores, health indicators, and plain-English insights guide action without requiring prior knowledge.

Is this system applicable outside major metros?

Yes. Whether you’re in Mumbai, Ahmedabad, Coimbatore, or Patna, the core financial principles are universal. The tools use percentages and ratios rather than absolute thresholds, so they adapt to different cost-of-living contexts.

How is the Financial Health Score different from a CIBIL score?

Your CIBIL score measures how reliably you repay loans — it exists for lenders, not for you. The Financial Health Score measures the overall strength of your financial life — savings discipline, investment consistency, debt burden, protection adequacy, and net worth — holistically. A person can have an excellent CIBIL score and a terrible Financial Health Score (high debt, zero savings, no insurance).

A score of 55 sounds low — should I be alarmed?

A score of 55 means there are visible gaps, but it is not a crisis. It is actually the most useful score to have — because it means improvement is both necessary and achievable. Focus on the two lowest-scoring pillars first. Most users see a 10–15 point improvement within 6–12 months of targeted action.

Does the tool store my financial data?

No. All calculations happen in your browser. No data is transmitted to or stored on Wealthpedia’s servers. No login is required. Your numbers remain entirely private.

The tool asks for very specific numbers. What if I don’t know them precisely?

Use your best estimates — round numbers are fine for a first assessment. The more precise your inputs, the more accurate your diagnosis, but even approximate inputs will reveal your major strengths and vulnerabilities. Precision improves with each subsequent assessment as you get more familiar with your numbers.

Can couples use this tool for joint finances?

Yes. You can either combine household income and expenses for a joint assessment or run separate assessments to compare financial health individually. For most Indian households, a combined assessment provides the most actionable picture.

What is “Goal Planner Mode” and how is it different from SIP Mode?

SIP Mode answers: “If I invest ₹X/month, how much will I have in N years?” Goal Planner Mode flips the question: “I want ₹Y corpus in N years — how much do I need to invest monthly?” Both modes display multiple scenarios simultaneously, so you’re always comparing, not calculating in isolation. One toggle switches between them instantly — no page reload, no separate tool.

Why does the tool show both nominal value and inflation-adjusted value?

The nominal value (e.g., ₹2.5 crore) is what your account will show. The inflation-adjusted value is what that amount will actually buy in today’s purchasing power terms. For long-term goals like retirement or a child’s education 20 years away, the inflation-adjusted figure is the number that actually matters for planning.

What is a realistic Step-Up SIP percentage to use?

For salaried professionals, 10% annual step-up is realistic and conservative — it mirrors average salary growth in India’s corporate sector. If you’re in a high-growth career or plan aggressive income increases, 15% is appropriate. The tool lets you set any percentage and see the exact compounding impact.

Can I compare SIPs across different asset classes — not just equity mutual funds?

The calculator is primarily designed for equity mutual fund SIPs, but it works for any investment with an expected annualised return. Set your expected return for debt funds, gold, or hybrid funds and compare scenarios across asset classes.

What is the Loan Health Score and what score is considered safe?

The Loan Health Score (0–100) rates the safety of your loan relative to your income and profile. Scores of 80–100 indicate an excellent loan structure. 60–79 is good. 40–59 is fair — manage proactively. Below 40 is high risk — the EMI is likely straining your cash flow. The key driver is your EMI-to-income ratio: ideally, total EMIs should not exceed 35–40% of take-home income.

How does the prepayment simulator account for bank prepayment charges?

The simulator shows the pure mathematical interest savings from prepayment. Prepayment penalties vary by bank (0–2% for some fixed-rate loans; zero for most floating-rate home loans under RBI guidelines). Factor your bank’s specific prepayment charge manually against the displayed interest savings to calculate your net benefit.

Should I choose “Reduce Tenure” or “Reduce EMI” when prepaying?

For wealth-building, “Reduce Tenure” is almost always the better choice. It eliminates the loan faster, saves more total interest, and frees up your full EMI amount sooner — which can then redirect to investments. “Reduce EMI” improves monthly cash flow immediately but keeps you in debt longer and costs more overall. Use “Reduce EMI” only if you’re genuinely cash-flow constrained today.

The tax benefits tab shows zero for my Personal Loan. Why?

Personal loans do not qualify for income tax deductions under Indian tax law, unlike home loans (Sections 80C and 24b) and education loans (Section 80E). This is accurate and by design — the calculator correctly excludes deductions where none legally exist, so you’re never misled about your actual tax liability.

I have a floating-rate home loan. How do I use the What-If Rate Comparison?

Enter your current rate and use the Rate Comparison tab to instantly see how your EMI and total interest change if your bank revises the rate up or down. This is particularly useful in an RBI rate cycle — you can model both a 50 bps rate cut (how much does my EMI drop?) and a 50 bps rate hike (how much more will I pay over the loan life?).

What is FIRE and what is a realistic FIRE corpus for India?

FIRE stands for Financial Independence, Retire Early. It is the accumulation of enough invested wealth so that its returns can fund your lifestyle indefinitely — without needing employment income. For Indian users, a safe withdrawal rate of 2.5–3% (implying a 33–40x corpus of annual expenses) is more appropriate than the Western 4% rule, due to higher domestic inflation (6%+) and longer potential retirement horizons.

What is the waterfall allocation engine and why does it matter?

The waterfall engine funds your goals in strict priority order using your single monthly SIP. It grows your total portfolio with monthly compounding throughout the year, withdraws the required corpus when each goal’s year arrives, checks whether the corpus is sufficient, records any shortfall, and continues with the remaining portfolio toward the next goal. This mirrors how professional financial planners actually allocate money across goals — and it’s the only free tool in India that does this.

Why does the planner show my portfolio till age 100?

Because retirement planning is fundamentally about making your money outlast you — not just accumulate enough by retirement. The chart shows both the accumulation phase (building wealth until FIRE age) and the decumulation phase (drawing down wealth through retirement) in one continuous visual. Seeing your wealth curve extend to age 100 forces realistic planning for longevity — something most retirement calculators conveniently ignore.

What is LTCG tax, and why does the planner account for it?

Long-Term Capital Gains (LTCG) tax of 12.5% applies to equity mutual fund gains above ₹1.25 lakh per year (as of 2026). When you withdraw from your FIRE corpus monthly, a portion of each withdrawal is taxable. Most FIRE calculators ignore this and tell you a corpus that looks sufficient but actually delivers less post-tax income than needed. Wealthpedia’s planner grosses up the required corpus so that after paying LTCG tax, your monthly income still matches your lifestyle expenses. This is advisor-level accuracy in a free tool.

Can I plan for goals that have already partially been funded (e.g., existing savings for education)?

Yes. Enter your current portfolio value (total investments today) in the Core Inputs. The engine grows this existing corpus alongside your ongoing SIP and applies it toward your goals in priority order. If you already have ₹10 lakh set aside for a goal due in 8 years, that corpus continues compounding and reduces the SIP burden for that goal.

Is Wealthpedia’s Personal Finance OS a substitute for a financial advisor?

No — and it doesn’t claim to be. It is a democratised diagnostic and planning system that gives you the same quality of analysis a good advisor would use, but as a starting point — not a replacement for personalised professional advice. For major financial decisions (large real estate purchases, complex tax situations, business ownership, significant estate planning), consulting a SEBI-registered investment advisor remains important. What the OS does is ensure you walk into that conversation already knowing your numbers, your gaps, and your goals — which makes every advisor conversation far more productive.

The Bottom Line: Your Financial Life Deserves an Operating System

The way most Indians manage their finances — checking returns here, calculating EMIs there, worrying about goals in a third place — is like running a business without an accounting system. Things seem to work until they suddenly don’t.

Wealthpedia’s Personal Finance OS changes that. It gives you:

- Clarity — a brutally honest picture of where you actually stand

- Confidence — a concrete, comparison-driven investment plan

- Control — optimised debt and liberated monthly surplus

- Choice — a unified, realistic path to financial independence

Every tool is free. Every tool is deeply engineered. Every tool is built for Indian reality. And together, they form something that has never existed in India before: a complete, sequenced operating system for your financial life.

Start with your Financial Health Score today. Then follow the framework.

Your financial transformation starts with a single number.

Start Your Journey

Stage Tool Link Clarity Financial Health Score wealthpedia.in/financial-health-score Confidence SIP Comparison Calculator wealthpedia.in/sip-comparison-calculator Control EMI Pro Calculator wealthpedia.in/emi-pro-calculator-india Choice Multi-Goal FIRE Planner wealthpedia.in/multi-goal-fire-planner-india

Disclaimer: This article is for educational and informational purposes only. Wealthpedia is not a SEBI-registered investment advisor. All tools are for indicative planning — consult a qualified financial professional before making major financial decisions.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up