Introduction: Why Most Indians Have No Idea What Their EPS Pension Will Be

Every month, 8.33% of your employer’s contribution quietly flows into a separate account you rarely think about — the Employees’ Pension Scheme, or EPS. Over a 30-year career, this becomes one of the most predictable income streams you will ever own: a guaranteed, lifelong monthly pension from EPFO, paid until your last breath, and continuing to your widow and children after you.

Yet ask any salaried Indian what their EPS pension will be, and the answer is almost always a shrug.

This is a planning failure with real consequences. Your EPS pension is a defined-benefit, government-backed annuity. In a world where fixed deposit rates fluctuate and safe withdrawal rates for Indian retirees are a subject of active debate, a guaranteed ₹4,000–₹7,500 per month for life is not trivial — it is a retirement planning anchor. Knowing this number lets you size your SIP corpus more precisely, plan your withdrawal strategy with more confidence, and make smarter decisions about when to retire.

The problem has never been the formula — it is actually simple. The problem is that every existing calculator in India gets at least one thing wrong, is missing key features, or presents results in a way that tells you nothing actionable.

This article explains the official EPS formula in full, walks through how to use the Wealthpedia EPS Pension Calculator step by step, shows you real-life examples across different income levels and career lengths, and answers the 20 questions we hear most often.

What Is EPS and Who Is Covered?

The Employees’ Pension Scheme (EPS-95) is administered by the Employees’ Provident Fund Organisation (EPFO) and was introduced on November 16, 1995. It provides a monthly pension to members of the organised sector workforce upon retirement, and to their family members upon death.

Who contributes to EPS?

Your employer contributes 12% of your Basic + Dearness Allowance (DA) to the EPF ecosystem. Of this 12%, 8.33% goes into EPS and only 3.67% goes into your EPF account. You, as the employee, contribute nothing directly to EPS — your full 12% goes to EPF.

Who is eligible?

- All employees earning a Basic + DA of ₹15,000 or less per month are mandatory EPS members.

- Employees earning above ₹15,000 can also be EPS members (contributions may be capped unless they opted for Higher Pension).

- Minimum 10 years of contributory service is required to receive a monthly pension.

- Members with fewer than 10 years of service can withdraw their EPS accumulation as a lump sum (Scheme Certificate or withdrawal).

When does pension begin?

Normal pension begins at age 58. Members with 10+ years of service can opt for early pension from age 50 (at a reduced rate) or defer pension up to age 60 (at an enhanced rate).

The Official EPS Pension Formula — Explained in Full

The formula EPFO uses is deceptively simple:

Monthly Pension = (Pensionable Salary × Pensionable Service) ÷ 70

But each of the three components has specific rules that most calculators handle incorrectly.

Component 1: Pensionable Salary

This is the average of your last 60 months of Basic + DA, capped at ₹15,000 per month — unless you are a Higher Pension member (see below).

The salary cap means that even if you earn ₹80,000 a month, your pensionable salary is still ₹15,000 for the pension calculation. This is why the maximum monthly pension under standard EPS is ₹7,500 (₹15,000 × 35 ÷ 70).

Higher Pension Exception: Following the Supreme Court order in November 2022, employees who were EPFO members before September 1, 2014, and whose employers paid EPS contributions on the actual salary (not capped), had a window to jointly apply for Higher Pension. If you are a Higher Pension member, your actual average salary — not capped at ₹15,000 — is used in the formula.

Component 2: Pensionable Service

This is your total years of EPS contributions, with three important rules:

Rule A — Rounding: If you have 6 or more months in a partial year, it rounds up to a full year. If you have fewer than 6 months, those months are dropped. So 24 years and 8 months becomes 25 years; 24 years and 4 months stays at 24 years.

Rule B — Maximum: Pensionable service is capped at 35 years.

Rule C — 20-Year Bonus: If your rounded pensionable service is 20 years or more, EPFO adds a 2-year bonus to your service count. So someone with 25 years of service gets an effective service of 27 years. This is a significant boost that most calculators miss entirely.

Component 3: The Divisor (70)

This is fixed. It is part of the EPS-95 formula and does not change.

Age Adjustments

Early Pension (age 50–57): If you choose to start your pension before age 58, the pension is reduced by 4% for each year before 58. Starting at 55 means a 12% reduction; at 50, a 32% reduction. You must have completed 10 years of service, and you must not be in active employment.

Deferred Pension (age 59–60): If you delay starting your pension after 58 (up to maximum age 60), the pension is increased by 4% per year. Waiting until 60 gives you an 8% enhancement.

Minimum Pension Floor: Regardless of the formula output, EPFO guarantees a minimum of ₹1,000 per month for eligible members (those with 10+ years of service). Note that the Parliamentary Standing Committee has formally recommended increasing this floor — watch for updates.

How to Claim EPS Withdrawal Benefit: Step-by-Step (Form 10-C)

The EPS Withdrawal Benefit is claimed using Form 10-C — distinct from Form 10-D, which is used to claim the monthly pension. Here is the complete process.

- Ensure your UAN is active and KYC is complete. Your Aadhaar, PAN, and bank account must be verified on the EPFO member portal. If KYC is incomplete, your claim will be rejected.

- Leave employment and confirm your exit date. EPS withdrawal can be claimed only after leaving the EPF-covered employment. There is typically a 2-month waiting period after the date of leaving before the claim can be filed online.

- Log into EPFO Member Portal at unifiedportal-mem.epfindia.gov.in using your UAN and password.

- Navigate to: Online Services → Claim (Form 31, 19, 10C & 10D)

- Select Form 10-C from the dropdown. The system will show your service details, pensionable salary, and estimated withdrawal amount for verification.

- Choose “Withdrawal Benefit” or “Scheme Certificate” — this is the decision point. If you choose Scheme Certificate, you will receive a physical certificate by post; no money is transferred. If you choose Withdrawal Benefit, the amount is credited to your verified bank account.

- Submit the claim. No employer attestation is required for online claims if KYC is complete — this is a significant simplification introduced in 2016. Processing time is typically 15–30 working days.

- Track your claim status under Online Services → Track Claim Status.

Offline alternative: If the online portal shows errors (common for claims involving multiple employers or older UANs), you can file a physical Form 10-C at your regional EPFO office. The form must be attested by your last employer.

Common rejection reasons: KYC mismatch, exit date not updated by employer, UAN not seeded with Aadhaar, or bank account not verified. Resolve each through the member portal before filing.

EPS Withdrawal Benefit: What Happens If You Leave Before 10 Years

If you leave employment before completing 10 years of EPS contributory service, you are not entitled to a monthly pension. Instead, EPFO provides a one-time EPS Withdrawal Benefit — a lump sum calculated using official Table-D factors based on your completed years of service and pensionable salary.

This section covers exactly how the withdrawal benefit is calculated, what Table-D says, when to take it versus preserving service via a Scheme Certificate, the tax treatment, and the exact claim process. These are the most-searched questions on EPS that are not answered elsewhere on this page — because they apply to a different situation than monthly pension.

What Is the EPS Withdrawal Benefit?

The EPS Withdrawal Benefit is a lump-sum payment EPFO makes when a member exits the scheme with fewer than 10 years of qualifying service. It compensates the member for the employer’s EPS contributions made on their behalf, using a standardised factor table rather than the actual contributions or the full EPF corpus.

It is important to be clear about what it is not: it is not a refund of the actual contributions. The employer contributes 8.33% of pensionable salary to EPS every month, but the withdrawal benefit you receive is determined by Table-D — which may be more or less than the actual cumulative contributions depending on years of service and assumed returns.

EPS Table-D: The Official Withdrawal Benefit Factors

EPFO’s Table-D specifies a multiplier for each completed year of service. The withdrawal benefit equals the pensionable salary multiplied by the Table-D factor for the relevant year. Pensionable salary is capped at ₹15,000 per month for standard EPS members (or the actual salary for Higher Pension members).

Important rounding rule for withdrawal benefit: Unlike the pension formula (where 6+ months rounds up), withdrawal benefit uses only completed full years. Partial years are not counted — so 3 years and 11 months gives the same benefit as exactly 3 years.

| Completed Years of EPS Service | Table‑D Factor | Withdrawal Benefit (₹15,000 salary) | Withdrawal Benefit (₹10,000 salary) |

|---|---|---|---|

| 1 year | 1.02 | ₹15,300 | ₹10,200 |

| 2 years | 1.99 | ₹29,850 | ₹19,900 |

| 3 years | 2.98 | ₹44,700 | ₹29,800 |

| 4 years | 3.99 | ₹59,850 | ₹39,900 |

| 5 years | 5.02 | ₹75,300 | ₹50,200 |

| 6 years | 6.07 | ₹91,050 | ₹60,700 |

| 7 years | 7.13 | ₹1,06,950 | ₹71,300 |

| 8 years | 8.22 | ₹1,23,300 | ₹82,200 |

| 9 years | 9.33 | ₹1,39,950 | ₹93,300 |

Notes:

- Table‑D factors are as per EPS-95 scheme rules.

- Withdrawal Benefit = Pensionable Salary × Table‑D Factor

- Minimum 1 completed year of EPS service is required

Example — Withdrawal Benefit Calculation: Rahul worked for 7 years and 9 months. His pensionable salary was ₹15,000. His completed years = 7 (9 months is partial, not counted). Table-D factor for 7 years = 7.13. Withdrawal benefit = ₹15,000 × 7.13 = ₹1,06,950.

The Wealthpedia EPS Pension Calculator now includes a built-in EPS Withdrawal Benefit tab that automatically activates when your service is below 10 years. It shows your estimated amount, the Table-D factor applied, and a full reference table — so you never need to look up Table-D manually again.

Scheme Certificate vs EPS Withdrawal: Which Should You Choose?

This is the most consequential decision a short-tenure EPS member faces — and the default instinct to “take the money now” is often wrong. Here is a structured framework.

| Factor | Take EPS Withdrawal Benefit | Get Scheme Certificate |

|---|---|---|

| Future employment | You will never work in an EPF‑covered organisation again | You may or will return to organised sector employment |

| Service close to 10 years | Only 1–3 years, unlikely to bridge the gap | 7–9 years — one more EPF-covered job pushes you past the threshold |

| Amount received now | Table‑D lump sum credited immediately | Nothing now — service is preserved |

| Future benefit | No pension eligibility from this service | Prior service gets added; total may reach 10 years eligibility |

| Tax on receipt | Taxable if received before 5 years of continuous service | No tax event — no withdrawal, only preservation |

| Reversibility | Irreversible — once withdrawn, service is erased | Reversible — certificate can be used later for pension claim |

Decision framework: Scheme Certificate vs EPS Withdrawal. For anyone with 7–9 years of service considering organised sector employment, the Scheme Certificate is almost always the better choice.

The key rule of thumb: If you have 7 or more years of EPS service and any realistic chance of returning to organised sector employment, choose the Scheme Certificate. The monthly pension you would eventually receive over a 20-year retirement will almost always exceed the lump-sum withdrawal benefit — often by a multiple of 3 to 5 times.

Consider: 9 years of service, ₹15,000 salary → withdrawal benefit of ₹1,39,950. But if that 9-year service is preserved and later combined with just 1 more year (reaching 10 years), the member becomes eligible for a monthly pension of approximately ₹(15,000 × 10 ÷ 70) = ₹2,143/month, or roughly ₹25,716/year — meaning the preserved service pays back the forgone ₹1.4 lakh in just 5.4 years, and then continues for life.

Is EPS Withdrawal Benefit Taxable?

Yes, but with an important nuance tied to service length and continuity.

Tax-free scenario: If you have completed 5 or more years of continuous service (across employers, with unbroken EPF contribution and UAN transfer — not withdrawal), the EPS withdrawal benefit is exempt from tax under Section 10(12) of the Income Tax Act, similar to EPF withdrawal rules.

Taxable scenario: If total continuous service is less than 5 years — meaning you withdrew EPF at some point and broke the continuity — the EPS withdrawal benefit is taxable in the year of receipt, added to your other income, and taxed at your applicable slab rate. TDS at 10% is deducted by EPFO if the amount exceeds ₹50,000 and you do not submit Form 15G/15H (for those eligible).

Practical implication: If you have 4 years and 10 months of unbroken service and are considering withdrawing, waiting just 2 more months to cross the 5-year mark could make the entire withdrawal tax-free. The difference at a 20% or 30% tax bracket on ₹70,000–₹1,20,000 of withdrawal benefit can be ₹14,000–₹36,000 — meaningful enough to plan around.

Always consult a tax advisor for your specific situation, especially if your service spans multiple employers or involves breaks in EPF contribution.

How to Verify Your EPS Service and Contributions Before You Calculate

The single most common error people make with EPS calculations — both on this calculator and in their own planning — is using the wrong service figure. Here is exactly how to get the correct number from EPFO records.

Step 1: Check Your EPFO Passbook

Log into the EPFO member portal at unifiedportal-mem.epfindia.gov.in using your UAN. Go to View → Passbook. You will see a separate passbook for each PF account (each employer) linked to your UAN.

The passbook shows monthly entries with the month and year of contribution. Count the total months across all accounts where EPS contributions appear — this is your total EPS service. Divide by 12 for years and keep the remainder as months to enter into the calculator.

Step 2: Confirm EPS Contributions Are Correctly Split

Each monthly passbook entry should show a split: a portion to EPF (employee contribution + 3.67% employer) and a portion to EPS (8.33% employer). If your passbook shows only EPF contributions and no EPS line, it could indicate:

- Your employer was exempted from EPS (rare, for certain trusts)

- Your salary exceeded the EPS threshold and you were excluded at some point

- A data entry error — raise a grievance with EPFO if EPS entries are missing despite being an EPF member

Step 3: Check for Gaps in Service

If you changed jobs and withdrew your EPF/EPS between employers rather than transferring, those years of service are lost from your EPS record. A withdrawal using Form 19 (EPF) and Form 10-C (EPS) resets the clock. This is the most common reason people discover their actual EPS service is shorter than their total career length.

The Wealthpedia Financial Health Score tool includes an EPF health check module that helps you identify contribution gaps and evaluate your overall retirement readiness — use it alongside this calculator for a complete picture.

Why Existing EPS Calculators in India Fall Short

Before explaining what makes the Wealthpedia calculator different, it is worth being specific about the gaps in the existing landscape.

Groww, ClearTax, and most generic tools offer a basic three-input form: salary, service years, divisor of 70. They produce a number but miss the month-rounding rule, the 20-year bonus, and the age adjustment entirely. You can get a figure that is off by 10–20%.

EPFO’s own portal requires you to log in, navigate the passbook, and manually count your service years. It does not provide a forward-looking estimate at all.

Zerodha Coin, Kuvera, Paytm Money — these platforms do not have an EPS calculator. Their focus is accumulation (mutual funds, NPS), not the decumulation side.

Value Research and Morningstar India cover mutual fund analytics but have no EPS tool.

The Wealthpedia EPS calculator corrects all of these gaps and adds four features no existing Indian tool provides: the Age Scenarios comparison, the Family Pension tab, the step-by-step calculation breakdown with labelled flags, and the deferred pension option up to age 60. It also enforces the ₹1,000 minimum pension floor and correctly gates the 2-year bonus behind the 20-year service threshold — both of which are routinely missed.

For a broader look at how to build a retirement income strategy that goes beyond EPS, see our Retirement Corpus Calculator and Retirement Withdrawal & SWP Calculator.

How to Use the Wealthpedia EPS Pension Calculator: A Step-by-Step Guide

The calculator has two sections: an input form on the left, and a four-tab results panel on the right. Here is exactly what to enter and how to read the output.

Step 1: Enter Your Average Basic + DA (Last 60 Months)

This is your average monthly Basic Salary plus Dearness Allowance over the last five years. If you are mid-career, use your current Basic + DA as a reasonable proxy.

Do not include HRA, LTA, bonuses, or any other components — only Basic and DA count.

If you are salaried in the private sector and your salary slip shows no DA separately, your Basic alone is the figure to use.

Where to find this number: Your salary slip, EPFO passbook, or Form 16. For the most accurate figure, average your last 60 months’ Basic + DA from your payslips.

Step 2: Choose Higher Pension or Standard Cap

If you are a standard EPS member, leave this on “No — Capped at ₹15,000”. Your pensionable salary will be capped regardless of what you enter.

If you jointly applied with your employer for Higher Pension under the Supreme Court 2022 ruling and your application was approved, select “Yes”. The calculator will use your actual salary figure.

Step 3: Enter Your Service Years and Additional Months

Enter your total EPS contributory service across all employers. This is not your current employer’s service — it is your total career service where EPS contributions were made.

When you switch jobs, the EPS credit transfers via your UAN.

Enter the additional months separately (0–11). The calculator applies the official rounding rule automatically.

Pro tip: Check your EPFO passbook on the member portal (unifiedportal-mem.epfindia.gov.in) to confirm your actual service period. Many people undercount service from early-career jobs.

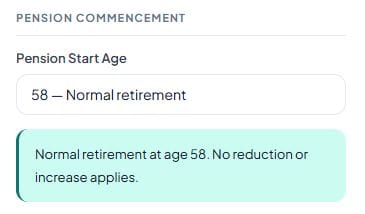

Step 4: Select Your Pension Start Age

Use the dropdown to choose your planned pension start age. The options are 50 through 60, with the age adjustment automatically calculated and displayed. The info box beneath the dropdown updates in real time to show the exact percentage impact.

For most people planning ahead, running the calculator at 58, 59, and 60 to compare outcomes is useful — which is exactly what the Age Scenarios tab does automatically.

Step 5: Enter Your Expected Life Span

This is used only to calculate the Lifetime Total figure — the total pension receipts over your expected retirement years. The EPFO actuarial assumption for Indian EPS is around 75–78 years for urban workers, but personal health history may warrant a higher number. The default of 80 is reasonable for planning purposes.

Step 6: Click “Calculate My EPS Pension →”

Results populate across four tabs.

Reading the Results: Tab by Tab

Summary Tab: The large teal card shows your monthly pension. Below it, the Annual Pension, Replacement Ratio (pension as % of current salary), and Lifetime Total are shown. A status pill at the top tells you whether your pension represents strong (≥40%), moderate (20–39%), or low (<20%) income replacement. The formula is shown with your actual numbers substituted in, so you can verify the arithmetic.

Calculation Steps Tab: Every step in the calculation is shown in sequence with labels. A “CAPPED” tag shows if your salary was limited to ₹15,000. A “+2 YRS” tag shows if the 20-year bonus applied. “ROUNDED UP” confirms month rounding. “FLOOR APPLIED” alerts you if the minimum ₹1,000 floor was triggered. This tab is your audit trail.

Age Scenarios Tab: All eleven ages from 50 to 60 are shown in a comparison table (desktop) or stacked cards (mobile), with monthly pension, adjustment percentage, annual pension, and lifetime total for each. Your selected age is highlighted. This lets you make an informed decision about whether to take early pension, wait for 58, or defer to 59–60.

Family Pension Tab: Shows estimated widow pension (approximately 50% of member pension, per EPFO Table-C), child pension (25% of widow pension per child, up to two children), and orphan pension (75% of widow pension per child). All figures respect the ₹1,000 minimum. These are approximations — actual amounts follow EPFO Table-C — but they are useful for retirement planning conversations with your family.

Real-Life Examples

Example 1: Factory Worker — Ramesh, 30 Years of Service, Standard EPS

Profile: Ramesh works at a manufacturing company. His Basic + DA has averaged ₹15,000 over the last five years (the cap applies regardless). He has 30 years and 7 months of service. He plans to retire at 58.

Inputs:

- Average Salary: ₹15,000

- Higher Pension: No

- Service: 30 years, 7 months

- Pension Start Age: 58

Calculation:

- Pensionable Salary: ₹15,000 (at cap)

- Rounding: 7 months ≥ 6, so rounds up to 31 years

- 20-Year Bonus: Applicable (31 ≥ 20), so +2 years

- Effective Service: 33 years

- Base Pension: (15,000 × 33) ÷ 70 = ₹7,071/month

- Age Adjustment: None (retiring at 58)

- Final Pension: ₹7,071/month

Annual Pension: ₹84,857

Lifetime Total (to age 80): ₹18.67 lakh

This is close to the maximum possible under standard EPS. Ramesh’s EPS pension alone covers basic monthly expenses in a smaller city. When combined with his EPF corpus and other savings, his retirement planning picture is solid for a lean lifestyle.

Example 2: IT Professional — Priya, High Salary, Standard Cap

Profile: Priya is a software engineer. Her Basic + DA has averaged ₹65,000 per month. She has 18 years and 4 months of service. She plans to retire at 58.

Inputs:

- Average Salary: ₹65,000

- Higher Pension: No

- Service: 18 years, 4 months

- Pension Start Age: 58

Calculation:

- Pensionable Salary: ₹15,000 (salary capped — ₹65,000 not used)

- Rounding: 4 months < 6, so stays at 18 years

- 20-Year Bonus: Not applicable (18 < 20)

- Effective Service: 18 years

- Base Pension: (15,000 × 18) ÷ 70 = ₹3,857/month

- Final Pension: ₹3,857/month

Replacement Ratio: 3,857 ÷ 65,000 = 5.9% — very low

The insight here is critical. Priya earns ₹65,000 in Basic alone, but her EPS pension is only ₹3,857. Her salary is irrelevant above the cap. For someone like Priya, EPS is a minor income floor — the real retirement work must be done by her SIP corpus, NPS, and EPF. This is why high-income earners need a separate retirement corpus calculator rather than relying on EPS estimates.

If Priya had opted for Higher Pension (actual salary used):

- Pensionable Salary: ₹65,000

- Base Pension: (65,000 × 18) ÷ 70 = ₹16,714/month

- Replacement Ratio: 25.7% — meaningfully better

But this comes at a cost: employer contributions that previously flowed to EPF now flow to EPS, reducing her EPF corpus. The trade-off depends on longevity and investment preferences.

Example 3: Early Pension — Suresh, Retiring at 55

Profile: Suresh has 22 years and 8 months of service. His Basic + DA is ₹15,000. He wants to retire at 55 due to health reasons.

Inputs:

- Average Salary: ₹15,000

- Service: 22 years, 8 months

- Pension Start Age: 55

Calculation:

- Pensionable Salary: ₹15,000

- Rounding: 8 months ≥ 6, rounds up to 23 years

- 20-Year Bonus: Applicable (+2 years)

- Effective Service: 25 years

- Base Pension: (15,000 × 25) ÷ 70 = ₹5,357/month

- Early Pension Reduction: (58 − 55) × 4% = 12% reduction

- Reduction Amount: ₹643

- Final Pension: ₹4,714/month

By retiring 3 years early, Suresh sacrifices ₹643/month permanently. Over a 25-year retirement (to age 80), this means he receives roughly ₹1.93 lakh less in lifetime pension. However, he also starts receiving pension 3 years earlier, collecting ₹4,714 × 36 = ₹1.70 lakh during those early years. The net early-pension trade-off here is roughly neutral around age 83 — making the decision personal rather than mathematical.

The Age Scenarios tab in the calculator shows this comparison instantly for all ages from 50 to 60.

Example 4: Deferred Pension — Meera, Waiting Until 60

Profile: Meera has 28 years of service. Basic + DA is ₹14,500. She is healthy, still employed at 58, and wants to maximise her pension.

Inputs:

- Average Salary: ₹14,500

- Service: 28 years, 0 months

- Pension Start Age: 60

Calculation:

- Pensionable Salary: ₹14,500

- Rounding: 0 months, stays at 28 years

- 20-Year Bonus: Applicable (+2 years)

- Effective Service: 30 years

- Base Pension: (14,500 × 30) ÷ 70 = ₹6,214/month

- Deferred Enhancement: (60 − 58) × 4% = +8%

- Enhancement Amount: ₹497

- Final Pension: ₹6,711/month

Versus starting at 58 (₹6,214/month), she gains ₹497/month permanently by waiting 2 years. She foregoes ₹6,214 × 24 months = ₹1.49 lakh during the deferment. The breakeven point is ₹1,49,136 ÷ ₹497 = 300 months = 25 years — so she breaks even at age 85. Deferring pension makes financial sense only if you expect to live well past the mid-80s.

Example 5: Minimum Pension Floor — Ajay, Short Service

Profile: Ajay worked for 12 years before switching to self-employment. His Basic + DA was ₹9,000. He plans to claim pension at 58.

Calculation:

- Pensionable Salary: ₹9,000

- Rounding: 0 extra months → 12 years

- 20-Year Bonus: Not applicable (12 < 20)

- Effective Service: 12 years

- Base Pension: (9,000 × 12) ÷ 70 = ₹1,543/month

- Final Pension: ₹1,543/month (above the ₹1,000 floor)

Ajay’s pension is modest but real. Had his service been only 10 years and his salary lower, the floor would have kicked in at ₹1,000. The calculator flags this with a “FLOOR APPLIED” tag so you always know exactly which rule is determining your pension.

How EPS Fits Into Your Overall Retirement Plan

EPS pension is one piece of a larger retirement income puzzle. Understanding where it fits helps you make smarter decisions about the rest of your planning.

EPF + EPS as a combined base. Your EPS pension provides a guaranteed monthly income. Your EPF corpus, accumulated separately, can be drawn down as a lump sum or through a Systematic Withdrawal Plan (SWP). Together, these cover the “guaranteed floor” of your retirement income. For a sophisticated look at how to structure the drawdown of a larger corpus, see the Retirement Withdrawal & SWP Calculator.

NPS as the variable annuity complement. NPS also mandates a 40% annuity purchase at withdrawal, giving you a second guaranteed income stream. Our NPS vs Mutual Funds comparison covers when NPS makes more sense than pure equity SIPs.

The SIP corpus fills the gap. For most salaried Indians, the EPS + EPF combination replaces only 30–50% of pre-retirement income. The gap must be filled by the equity + debt SIP corpus built over a career. Our Best SIP Strategy for Retirement 2026 and the Waterfall SIP Allocation guide explain how to structure this.

Healthcare is your biggest wildcard. EPS pension is not indexed to inflation, so its real value erodes every year. This makes healthcare planning especially important — a single hospitalisation can wipe out months of pension income. See our Healthcare Inflation Calculator to understand how medical costs scale as you age.

Sequence-of-returns risk is real even with guaranteed income. Having a pension floor reduces but does not eliminate this risk. If markets crash in your early retirement years while you also have a SIP corpus to draw from, the pension acts as a buffer. For a full treatment, see Sequence of Returns Risk for Indian Retirees.

If you are also considering early retirement, your EPS pension may not start at the same time as your income stops. Our FIRE at 40, FIRE at 45, and FIRE at 50 guides cover how to bridge the gap between FIRE date and pension start.

Frequently Asked Questions About EPS Pension

What is the maximum monthly pension under EPS?

The maximum is ₹7,500 per month for standard EPS members. This is achieved with the salary capped at ₹15,000 and the maximum effective service of 35 years (i.e., ₹15,000 × 35 ÷ 70). In practice, with the 2-year bonus, an effective service of 37 years is possible, giving a maximum of ₹7,929/month (₹15,000 × 37 ÷ 70). For Higher Pension members, there is no hard cap.

What is the minimum pension under EPS?

The minimum monthly pension is ₹1,000, as set in 2014. However, this applies only if you have completed 10 or more years of qualifying service. Below 10 years, you are not eligible for monthly pension — only a lump-sum withdrawal.

Is EPS pension taxable?

Yes. EPS pension is taxable under the head “Income from Salary” or “Income from Other Sources” depending on whether you are still employed when you receive it. It is added to your total income and taxed at your applicable slab rate. However, most pensioners’ total income (EPS + other) may fall below the ₹3 lakh basic exemption limit (New Tax Regime) or ₹2.5 lakh (Old Regime). See our PPF vs ELSS vs NPS comparison for tax-efficient alternatives to consider alongside EPS.

Can I receive EPS pension while still working?

Yes, if you retire at 58 (superannuation). The rules allow you to start receiving EPS pension upon turning 58 even if you continue in employment, because EPS membership automatically ends at 58. However, for early pension (50–57), you must not be in employment when you claim.

What happens to EPS if I resign before 10 years?

If you have less than 10 years of qualifying service, you are not entitled to a monthly pension. You can either:

(a) Withdraw the EPS accumulation as a lump sum using Form 10-C, or

(b) Obtain an EPS Scheme Certificate and preserve your service history for future use if you rejoin covered employment.

Taking the lump sum makes sense only if you are permanently leaving the organised sector. If there is any possibility of returning to an EPF-covered job, the Scheme Certificate preserves your service credit.

How is EPS different from EPF?

EPF (Employees’ Provident Fund) is a savings account — money goes in, earns interest, and comes back to you as a lump sum on retirement or withdrawal. EPS is a defined-benefit pension scheme — contributions go into a pool managed by EPFO, and you receive a monthly pension for life regardless of how much was contributed on your behalf. You cannot “withdraw” EPS as a lump sum once you are eligible for monthly pension, except in specific early-exit scenarios.

What is the EPS Scheme Certificate and when should I get one?

A Scheme Certificate is a document EPFO issues when you exit employment before 10 years without withdrawing EPS. It records your service and salary for future use. If you later join another EPF-covered employer, your previous service adds to the new service, helping you cross the 10-year threshold. Always get a Scheme Certificate when leaving a job — never let early-career EPS accumulations go unclaimed.

What does “Higher Pension” mean and am I eligible?

Following the Supreme Court judgment of November 4, 2022, employees who were EPFO members before September 1, 2014, and whose employers had been contributing EPS on the actual salary (not capped), could jointly apply with their employer for Higher Pension. The window to apply closed in May 2023. If you applied and it was approved, your EPS pension is calculated on your actual average salary, not capped at ₹15,000. Check with your employer’s HR or your EPFO passbook to confirm your status.

Is the 2-year bonus service always added if I have 20+ years?

Yes — this is an automatic rule in EPS-95, not an optional benefit. If your rounded pensionable service reaches 20 years or more, EPFO adds 2 years to the service count for pension calculation purposes. You do not need to apply for this.

Can I nominate someone other than my spouse to receive EPS family pension?

EPS family pension rules are strict. The widow (or widower) is the primary beneficiary. If there is no surviving spouse, children under 25 receive children’s pension (25% of widow pension per child, max 2 children). If the widow remarries, children become “orphans” and receive orphan pension (75% of widow pension each). The scheme does not allow nomination to parents, siblings, or other relatives for the monthly family pension.

What if I worked for multiple employers? Does service add up?

Yes. EPS contributory service across all employers is cumulative, provided you transferred your PF account (via UAN) rather than withdrawing. When you join a new employer and link your UAN, all prior service is preserved. This is why UAN portability is critical — withdrawing your EPF/EPS at every job change destroys your pension entitlement.

Will my EPS pension increase after I start receiving it?

The base pension amount is fixed at retirement. EPFO does occasionally declare “pension relief” (a percentage increase for existing pensioners), but these are irregular and not guaranteed. EPS pension is not formally indexed to inflation, which is an important planning consideration — the real purchasing power of ₹5,000/month today will be significantly lower in 20 years. This reinforces the need for an inflation-adjusted corpus alongside EPS. Our article on how inflation erodes SIP corpus explains the mechanics in detail.

What is the difference between early pension and premature withdrawal?

Early pension (age 50–57) means you start receiving your monthly pension before the normal age of 58, at a permanently reduced rate. Premature withdrawal means you exit EPS entirely and take a lump-sum payout, forfeiting any future monthly pension. Once you are past 58 with 10+ years of service, you cannot take a lump-sum withdrawal — you must take the monthly pension.

How do I claim my EPS pension?

You claim EPS pension using Form 10-D filed with your regional EPFO office (or online via the member portal). You will need your UAN, Aadhaar, bank account details, and a joint declaration from your last employer. The processing time is typically 30–90 days. Pension is credited monthly to your bank account.

Is EPS pension available to self-employed or freelancers?

No. EPS covers only employees of establishments registered under the EPF & MP Act, 1952 (typically companies with 20+ employees). If you are self-employed, a freelancer, or work for an unregistered small employer, you are not covered under EPS. NPS (through the NPS Lite or All Citizens model) is the government-backed pension alternative for such individuals. See our NPS vs Mutual Funds guide for how to think about this.

Does EPS pension stop at the member’s death?

The member’s pension stops at death. However, the family pension (widow pension, children pension, or orphan pension) continues immediately to the eligible family member. Widow pension is paid until the spouse’s death or remarriage. Children’s pension is paid until each child turns 25. For planning purposes, the EPS Family Pension tab in this calculator gives you approximate figures for these dependent benefits.

What if my employer did not deposit EPS contributions?

This is unfortunately a real issue for employees of smaller or financially stressed companies. If your passbook shows contributions but your pension claim is rejected due to employer default, you can file a complaint with the regional EPFO office. EPFO has the power to recover dues from employers and credit the EPS account. Always monitor your EPFO passbook via the member portal for regular contribution credit.

Can NRIs receive EPS pension?

Yes. There is no residency restriction on EPS pension. If you qualified under EPS and later became an NRI, you can still claim your pension at the appropriate age and have it credited to an NRI bank account in India (NRO account). Consult with your bank on repatriation rules and applicable TDS.

How does EPS interact with my overall FIRE plan?

If you are pursuing Financial Independence / Retire Early, EPS is a guaranteed income floor that actually reduces the corpus you need. A ₹5,000/month EPS pension starting at 58 reduces the SWP requirement from your invested corpus by ₹5,000 × 12 = ₹60,000/year — which at a 3.5% safe withdrawal rate means you need ₹17.1 lakh less in your investable corpus. Use the Wealthpedia FIRE Number Calculator alongside this EPS calculator to get your net FIRE corpus target.

The calculator says my pension is very low. What can I do?

If your projected EPS pension is low (under ₹2,000/month), it is typically because of one of three reasons: (a) short service tenure below 20 years (missing the 2-year bonus and having fewer effective years), (b) salary capped at ₹15,000 when your actual contribution base was low, or early pension with a steep reduction. The honest answer is that EPS has structural limits — it was designed as a floor, not a replacement income. Building a robust SIP corpus is the primary lever. See our SIP calculator with inflation and the Step-Up SIP guide to accelerate your corpus building.

Can I claim both EPF and EPS withdrawal at the same time?

Yes. EPF withdrawal (Form 19) and EPS Withdrawal Benefit (Form 10-C) are filed together as a composite claim on the EPFO portal. You do not need to file two separate claims. When you select “Final Settlement” under Online Claim, the system processes both EPF and EPS simultaneously. However, if you want only a Scheme Certificate (EPS preserved) but want the EPF amount, you select EPF withdrawal separately and EPS Scheme Certificate separately — in which case two distinct selections are made.

What if I have less than 1 year of EPS service?

Table-D starts from 1 completed year. If you have less than 12 months of EPS contributions, you are not entitled to either monthly pension or the Table-D withdrawal benefit. However, the actual employer EPS contributions made may be refunded — the mechanism for this varies and is handled by EPFO directly based on your records. Raise a grievance with your regional EPFO office if you believe contributions were made on your behalf for a period below 1 year.

Does the EPS Withdrawal Benefit earn interest?

No. EPS is a defined-benefit scheme — your contributions go into a common pool managed by EPFO and there is no individual account earning interest. The withdrawal benefit is determined solely by Table-D, regardless of actual contributions or the interest EPFO earns on the pool. This is fundamentally different from EPF, where your individual account earns the declared rate (currently 8.25% for 2023-24) and the balance grows year on year.

I withdrew EPS at a previous job. Can I still claim pension on my current service?

Yes — but only for the current and subsequent service periods. The withdrawn service is gone and cannot be reclaimed. Your pension calculation will use only the service from your new start date. This is why withdrawing EPS between jobs is almost always a financial mistake for those planning long careers in the organised sector — ₹30,000–₹60,000 received today could cost you ₹1,000–₹3,000/month in pension for 20+ years.

Is there a deadline to claim EPS Withdrawal Benefit after leaving a job?

There is no statutory deadline to claim EPS Withdrawal Benefit, but practical constraints apply: dormant accounts can be difficult to process if your UAN is inactive, your employer’s PF trust has closed, or contact details have changed. EPFO also occasionally transfers unclaimed balances to a senior citizens’ welfare fund after extended inactivity. Best practice is to file within 3–6 months of leaving employment, or get a Scheme Certificate if you are unsure about future employment plans.

Will the EPS Withdrawal Benefit affect my EPF withdrawal eligibility?

No. EPS and EPF are separate accounts and claiming one does not affect the other. You can withdraw EPF (Form 19) and leave EPS as a Scheme Certificate, or withdraw both simultaneously, or withdraw EPS and leave EPF invested (if you are below 58 and not fully retiring). The flexibility exists — but the composite online claim is the simplest route for a complete final settlement.

Key Planning Takeaways

Knowing your EPS pension number is not just an academic exercise — it changes real decisions.

It sets your retirement income floor. Every guaranteed rupee per month from EPS is one less rupee you need your invested corpus to generate. A ₹6,000/month EPS pension at 4% withdrawal rate is equivalent to having ₹18 lakh extra in corpus. Factor it in before you panic about whether you have enough to retire.

It informs your early retirement math. If you want to FIRE at 45 but EPS doesn’t start until 58, you have a 13-year gap where EPS contributes nothing. The Wealthpedia Multi-Goal FIRE Planner lets you model this gap explicitly — building a bridge corpus for ages 45–58 and a perpetual corpus for post-58 life.

It guides when to retire. The Age Scenarios tab shows clearly whether deferring to 59 or 60 meaningfully improves your income. For most people, the 4% annual increase for deferral has a long breakeven (age 83–85). Unless you have strong health reasons to expect longevity, retiring at 58 rather than deferring is often the right call.

It reduces your annuity purchase need. Many retirement planners recommend buying an annuity at retirement for guaranteed income. If your EPS pension is already ₹5,000–₹7,000/month, your annuity need from NPS or other sources is correspondingly lower — and the corpus you need to accumulate through SIPs is smaller.

It is not enough on its own. This bears repeating. The maximum EPS pension is ₹7,929/month. India’s urban consumer inflation is 5–6%. For anyone with a monthly expense of ₹50,000 today, EPS covers at most 15% of retirement income needs. The remaining 85% must come from EPF, NPS, mutual funds, real estate rental income, or other sources. Understanding your savings rate and how it translates to retirement corpus is the next step.

About This Calculator

The Wealthpedia EPS Pension Calculator was built using official EPFO EPS-95 rules and validated against published EPFO pension calculations. It implements the full formula — including the month rounding rule, the 20-year service bonus, early pension reduction (4%/year before 58), deferred pension enhancement (4%/year after 58, up to 60), the ₹1,000 minimum pension floor, and the Higher Pension toggle for members covered under the Supreme Court 2022 ruling. Few months ago, I had developed a basic EPFO Pension Calculator and based on the user feedbacks, I have design this comprehensive EPS Pension Calculator.

Unlike most tools, the calculator shows you every step of the calculation so you can verify the arithmetic independently. If you spot an error or have a specific edge case to report, use the contact page.

For the full suite of financial planning tools, visit the Wealthpedia Calculators hub.

Methodology & Data

Our tools and calculators are built using a robust combination of historical data, well-established financial models, and user-defined inputs to ensure relevance and practicality. Each tool incorporates carefully selected datasets—such as market returns, inflation trends, and regulatory frameworks—paired with proven methodologies like rolling return analysis, withdrawal rate modelling, and rule-based calculations.

To ensure reliability, every model undergoes rigorous design validation and back-testing against historical scenarios. We simulate real-world conditions across different market cycles to evaluate consistency and accuracy. Additionally, assumptions are regularly reviewed and refined to reflect changing financial environments.

We encourage users to explore the underlying methodology and assumptions behind each tool to better understand how results are generated, enabling more informed and confident financial decision-making.

This article was last updated in June 2026. EPS rules are set by EPFO and the Ministry of Labour. While every effort has been made to ensure accuracy, always verify your final pension amount with EPFO directly. The EPS Withdrawal Benefit calculator and Table-D values are based on EPFO EPS-95 scheme rules as publicly available. Actual entitlements are determined by EPFO based on official contribution records. This content is for educational purposes only and does not constitute financial, legal, or tax advice. Consult a qualified advisor for personalised guidance. I am not a SEBI-registered financial advisor. See full disclaimer.