“Pensionable salary” is the most consequential number in your EPS pension calculation — yet most employees have never consciously thought about what it is or why it matters. It appears in the formula once, but its value determines whether your monthly pension is ₹2,143 or ₹42,857.

This guide explains exactly what pensionable salary is, what components count, what the ₹15,000 ceiling means in practice, how the pre-2014 rules differed, and how the Higher Pension Scheme changes everything for eligible members.

Use the EPS Pension Calculator India to see how different pensionable salary values affect your monthly pension.

Quick Summary

Pensionable salary under EPS is the monthly salary figure used in the EPS pension formula — (Pensionable Salary × Pensionable Service) ÷ 70. For most employees, it is capped at ₹15,000 per month regardless of actual salary, since September 2014. Only basic salary + Dearness Allowance (DA) counts — HRA, conveyance, and other allowances are excluded. If your actual basic+DA is below ₹15,000, the actual amount is used. Under the Higher Pension Scheme, the cap is removed and the actual 60-month average salary is used. This article explains every dimension of pensionable salary with examples and its impact on pension. Use the EPS Pension Calculator India to see the effect on your pension.

What Is Pensionable Salary?

Pensionable salary under EPS is the monthly salary figure on which EPS contributions are calculated and which is used as the salary input in the EPS pension formula.

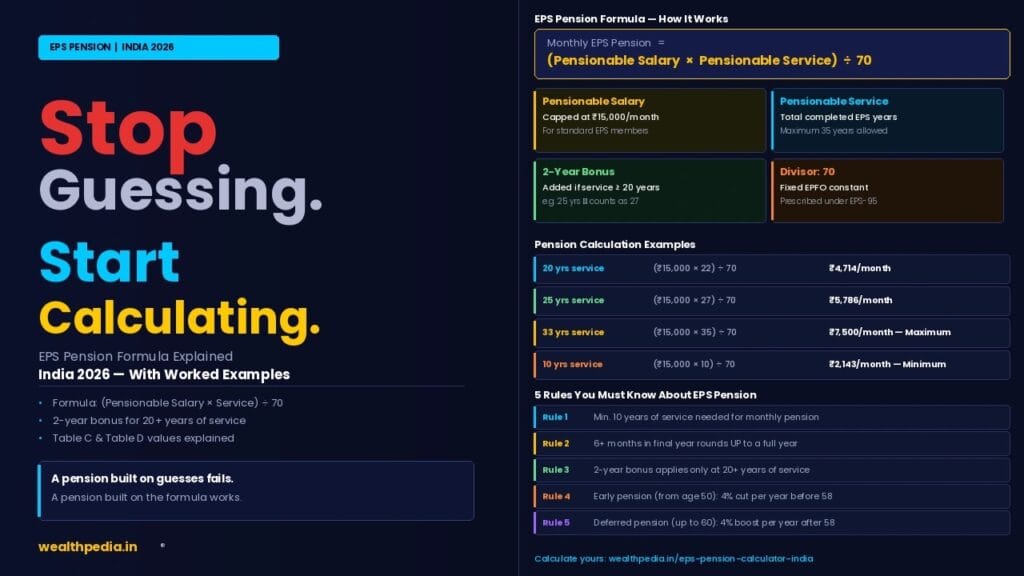

It appears in the formula as:

Monthly EPS Pension = (Pensionable Salary × Pensionable Service) ÷ 70

Pensionable salary is not your gross salary, not your take-home salary, and not even your full CTC. It is a specific, defined component subject to regulatory caps.

The ₹15,000 Wage Ceiling — The Most Important Rule

For most EPS members, pensionable salary is capped at ₹15,000 per month — regardless of actual salary.

This ceiling has been in effect since September 1, 2014, when EPFO raised it from the previous ₹6,500 ceiling. The ceiling means:

- If your basic + DA = ₹30,000 → Pensionable salary = ₹15,000 (capped)

- If your basic + DA = ₹50,000 → Pensionable salary = ₹15,000 (capped)

- If your basic + DA = ₹12,000 → Pensionable salary = ₹12,000 (actual used — below ceiling)

- If your basic + DA = ₹15,000 → Pensionable salary = ₹15,000 (exact ceiling)

Why the ceiling exists: EPS is a defined-benefit scheme where government subsidises part of the pension for lower-income workers. The ceiling limits EPFO’s liability and prevents the pension fund from being skewed toward higher-income employees. The monthly EPS contribution is capped at 8.33% × ₹15,000 = ₹1,250/month.

What Counts as Pensionable Salary — Component Breakdown

| Salary Component | Counts Towards Pensionable Salary? |

|---|---|

| Basic salary | ✅ Yes |

| Dearness Allowance (DA) | ✅ Yes |

| House Rent Allowance (HRA) | ❌ No |

| Conveyance / Transport allowance | ❌ No |

| Special allowance | ❌ No |

| Medical allowance | ❌ No |

| Bonus / ex-gratia | ❌ No |

| Performance incentives | ❌ No |

| Overtime pay | ❌ No |

| Leave encashment | ❌ No |

Why DA Is Included

Dearness Allowance is an inflation-compensation component paid in addition to basic salary. Since it is structurally part of the base pay (particularly relevant for PSU and government employees), EPFO includes it in pensionable salary. Many private sector companies have zero DA (it is merged into basic) — in those cases, only basic salary forms the pensionable salary.

Practical Implication

For a private sector employee with CTC of ₹10 lakh:

- Gross salary: ₹83,333/month

- Basic salary: ₹30,000/month

- HRA: ₹15,000/month

- Special allowance: ₹38,333/month

- Pensionable salary: min(₹30,000, ₹15,000) = ₹15,000/month

Even though actual salary is ₹83,333/month, the pensionable salary for EPS is ₹15,000.

Pre-2014 Pensionable Salary — The ₹6,500 Ceiling Era

Before September 2014, the EPS wage ceiling was ₹6,500 per month (raised from ₹5,000 before 2001). This affected employees who worked through the pre- and post-2014 period in important ways.

Impact on Pension for Long-Tenured Employees

For an employee who joined in 1995 and retired in 2030 (35 years of service):

- Years under ₹6,500 ceiling: approximately 1995–2014 (19 years)

- Years under ₹15,000 ceiling: 2014–2030 (16 years)

EPFO uses the pensionable salary at the date of retirement (or cessation of employment) for the pension calculation — not a blended average of ceilings over the career. So an employee retiring after 2014 uses ₹15,000 as pensionable salary, regardless of how many years they worked under the ₹6,500 ceiling.

This effectively gave a significant pension boost to long-tenured employees who were still working when the ceiling was raised in 2014.

The 2014 Option — Employees Who Opted Out

When the ceiling was raised in September 2014, employees earning above ₹15,000 were given the option to become “excluded employees” — opting out of EPS. Those who opted out after September 2014 do not have EPS membership for the post-2014 period. Their pensionable service is frozen at the date of opt-out.

Pensionable Salary When Actual Salary Is Below ₹15,000

For employees whose actual basic + DA is below the ₹15,000 ceiling, the actual salary is used as pensionable salary — not ₹15,000.

Example — ₹10,000 Basic+DA, 20 Years Service

- Pensionable Salary: ₹10,000 (actual — below ceiling)

- Pensionable Service: 20 + 2 bonus = 22 years

- Monthly Pension = (10,000 × 22) ÷ 70 = ₹3,143/month

Compare with ₹15,000 salary at the same service:

- Monthly Pension = (15,000 × 22) ÷ 70 = ₹4,714/month

The lower pensionable salary reduces the pension proportionally. EPFO’s minimum pension guarantee of ₹1,000/month protects members whose formula-based pension falls below this floor. See What Is the Minimum EPS Pension in India?

Pensionable Salary Under the Higher Pension Scheme

For members approved under the Higher Pension Scheme (HPS), pensionable salary is the average of actual basic + DA over the last 60 months of EPS-covered service — with no ₹15,000 ceiling.

This is the defining difference between standard EPS and HPS — the salary input changes completely: EPS Type Pensionable Salary Standard EPS ₹15,000 (ceiling) or actual if below Higher Pension Scheme 60-month average of actual basic + DA

HPS Pensionable Salary Example

- Last 5 years average basic + DA: ₹60,000/month

- Pensionable Salary under HPS: ₹60,000

- Pension (30 years service): (60,000 × 32) ÷ 70 = ₹27,429/month

- vs Standard EPS: (15,000 × 32) ÷ 70 = ₹6,857/month

For the complete HPS guide, see EPS Higher Pension Scheme: Eligibility & Calculation.

How Pensionable Salary Is Verified by EPFO

EPFO verifies pensionable salary from the employer’s monthly ECR (Electronic Challan cum Return) filings. The ECR shows the salary on which EPS contributions were calculated each month. EPFO uses this data to:

- Confirm that EPS contributions were made on the correct salary basis

- Determine the pensionable salary at the date of retirement (for standard EPS)

- Calculate the 60-month average (for HPS members)

If there is a discrepancy between what the employer reported and the actual salary, the member can raise a grievance via EPFiGMS at epfigms.gov.in.

Pensionable Salary vs Pensionable Service — How They Interact

Both variables in the formula are multiplicative — a change in either proportionally changes the pension: Pensionable Salary Pensionable Service Monthly Pension ₹10,000 22 years (20 + bonus) ₹3,143 ₹12,000 22 years ₹3,771 ₹15,000 22 years ₹4,714 ₹15,000 27 years (25 + bonus) ₹5,786 ₹15,000 35 years (max) ₹7,500 ₹40,000 (HPS) 27 years ₹15,429 ₹60,000 (HPS) 32 years ₹27,429

The pension scales linearly with both variables — doubling pensionable salary doubles the pension (all else equal), and doubling service doubles the pension (all else equal).

For the full formula explanation, see EPS Pension Formula Explained.

Why Splitting Salary Into More Components Reduces EPS Pension

A common practice in Indian payroll structuring is to split the CTC into many small components to reduce tax and PF liability — keeping basic salary low and HRA, special allowances, and other components high.

Impact on EPS:

- Lower basic salary = lower pensionable salary (if below ₹15,000)

- For employees with basic+DA already above ₹15,000, this does not affect EPS (ceiling already applies)

- For employees with basic+DA below ₹15,000, salary structuring that further reduces basic directly reduces EPS pension

Example:

- Employee A: Basic ₹14,000, DA ₹0 → Pensionable salary = ₹14,000

- Employee B: Basic ₹10,000, DA ₹0, Special allowance ₹4,000 → Pensionable salary = ₹10,000

Same total pay, but Employee A gets ₹700/month more in EPS pension over the same service period — all because the basic salary was structured higher.

Pensionable Salary for Contract Employees and Piece-Rate Workers

For contract employees engaged through registered contractors:

- The principal employer’s EPF registration covers them

- Pensionable salary = basic + DA as per their actual wages, subject to ₹15,000 ceiling

- If wages are expressed as a daily or piece-rate, the monthly equivalent is used

For piece-rate workers, EPFO uses the monthly average wages to determine pensionable salary.

Pensionable Salary — Common Misconceptions

Misconception 1: “My pensionable salary is my gross salary.”

False. Only basic + DA counts. Gross salary includes HRA, allowances, and other components that are excluded.

Misconception 2: “If I earn ₹50,000, my EPS pension is based on ₹50,000.”

False. For standard EPS members, pensionable salary is capped at ₹15,000 regardless of actual earnings. The pension formula uses ₹15,000, not ₹50,000.

Misconception 3: “The ₹15,000 ceiling means I only contributed ₹15,000 to EPS.”

The ceiling means EPS contributions are calculated on ₹15,000 (not your actual salary). The actual contribution is 8.33% × ₹15,000 = ₹1,250/month — regardless of whether you earn ₹20,000 or ₹2,00,000.

Misconception 4: “My pensionable salary changes over time and the pension reflects the latest.”

For standard EPS, EPFO uses the pensionable salary at the date of leaving employment (capped at ₹15,000) — not a career average. One year before retirement you may have gotten a raise — but if your basic+DA was already above ₹15,000, it makes no difference to your EPS pension.

Misconception 5: “Pensionable salary affects how much I can withdraw from EPS.”

The Table D withdrawal benefit = Table D Factor × Pensionable Salary. So yes — for those withdrawing before 10 years, a lower pensionable salary means a smaller lump-sum withdrawal. See EPS Withdrawal Benefit Calculator.

Pensionable Salary Quick Reference

| Scenario | Pensionable Salary Used |

|---|---|

| Basic + DA ≤ ₹15,000 | Actual Basic + DA |

| Basic + DA > ₹15,000 (standard EPS) | ₹15,000 (ceiling) |

| Higher Pension Scheme approved | 60-month average of actual Basic + DA |

| Before September 2014 (old ceiling) | Lower of actual salary or ₹6,500 |

| Retired after September 2014 | ₹15,000 ceiling applies (regardless of pre-2014 salary) |

| Below ₹15,000 at joining, increased later | Still capped at ₹15,000 after ceiling implementation |

Frequently Asked Questions — Pensionable Salary Under EPS

What is pensionable salary under EPS?

Pensionable salary is the monthly salary figure used in the EPS pension formula: (Pensionable Salary × Pensionable Service) ÷ 70. For most members it equals the lower of actual basic+DA or ₹15,000/month. Under the Higher Pension Scheme, it is the actual 60-month average salary with no ceiling.

What is the pensionable salary limit under EPS in 2026?

The pensionable salary ceiling is ₹15,000 per month as of 2026, unchanged since September 2014. This means the maximum EPS contribution is ₹1,250/month (8.33% × ₹15,000), and the maximum standard EPS pension is ₹7,500/month.

Does HRA count towards pensionable salary?

No. Only basic salary + Dearness Allowance (DA) counts. HRA, conveyance, special allowance, medical allowance, bonus, and all other components are excluded from pensionable salary.

What if my basic salary is ₹8,000 — what is my pensionable salary?

If your basic + DA is ₹8,000 (below the ₹15,000 ceiling), your pensionable salary is ₹8,000. Your monthly EPS pension after 20 years would be: (8,000 × 22) ÷ 70 = ₹2,514/month. Use the EPS Pension Calculator India to compute yours.

Does pensionable salary change when I get a salary hike?

Only if the hike brings your basic+DA from below ₹15,000 to above ₹15,000 — at that point pensionable salary becomes fixed at ₹15,000. If your basic+DA was already above ₹15,000, salary hikes have no effect on pensionable salary for standard EPS members.

What was pensionable salary before 2014?

Before September 2014, the EPS wage ceiling was ₹6,500/month. Members who retired before September 2014 had their pension calculated on the lower ceiling. Members who were still employed when the ceiling was raised to ₹15,000 in September 2014 benefit from the higher ceiling in their pension calculation.

How does pensionable salary affect the EPS withdrawal benefit?

The Table D withdrawal benefit = Table D Factor × Pensionable Salary. So a member with pensionable salary of ₹10,000 receives a smaller withdrawal benefit than one with ₹15,000 for the same service years. Example: 7 years service — Table D factor 7.46 × ₹10,000 = ₹74,600 vs 7.46 × ₹15,000 = ₹1,11,900.

Is pensionable salary the same as EPF wages?

They are related but not identical. EPF wages (on which both employee and employer EPF contributions are calculated) can include basic + DA + other allowances depending on the employer’s EPF filing structure. Pensionable salary for EPS is specifically basic + DA, capped at ₹15,000. In practice, EPFO uses the salary reported on ECR filings.

Can my employer set my pensionable salary below ₹15,000 deliberately?

Technically, the pensionable salary is determined by actual basic+DA — not something the employer can arbitrarily set below actual pay. However, employers who structure payroll with very low basic and high allowances effectively keep pensionable salary low. This is legal but reduces the employee’s EPS pension entitlement.

What is pensionable salary for a PSU employee with DA?

For PSU employees, both basic salary and the DA paid are included. If basic = ₹10,000 and DA = ₹8,000, pensionable salary = ₹18,000 → capped at ₹15,000 for standard EPS. For Higher Pension Scheme members, the full ₹18,000 (or the 60-month average) is used.

If I moved from ₹12,000 basic to ₹18,000 basic mid-career, what is my pensionable salary?

EPFO uses the pensionable salary at the date of leaving employment (capped at ₹15,000). Since ₹18,000 > ₹15,000, your pensionable salary is ₹15,000 — regardless of what it was earlier in your career.

Does pensionable salary affect family pension?

Yes — indirectly. Family pension is a percentage of the member’s pension, which is calculated using pensionable salary. A higher pensionable salary → higher member pension → higher widow/child pension. Under HPS, widow pension can be ₹13,000–₹20,000+/month vs ₹2,000–₹3,750 under standard EPS.

What is the EPS pension for pensionable salary of ₹12,000 after 25 years?

Pensionable Service = 25 + 2 bonus = 27 years. Monthly Pension = (12,000 × 27) ÷ 70 = ₹4,629/month. Compare with ₹5,786/month at ₹15,000 ceiling — the ₹3,000 salary difference results in ₹1,157/month lower pension.

Is pensionable salary the same as CTC?

No. CTC (Cost to Company) includes all employer costs — EPF contribution, EPS contribution, gratuity, insurance, and other benefits. Pensionable salary is only basic + DA, capped at ₹15,000. It is a small subset of CTC.

Can pensionable salary be higher than ₹15,000 for standard EPS members?

No. For standard EPS members (not HPS), ₹15,000 is the absolute ceiling. No matter how high the actual salary, standard EPS pension is capped by this ceiling. Only HPS-approved members can have pensionable salary above ₹15,000.

What pensionable salary is used for invalidity pension?

The pensionable salary at the time of disablement (capped at ₹15,000 for standard EPS) is used, along with either the actual service or the 2-year notional minimum (whichever is higher). The formula and ceiling rules are the same as standard pension.

Does changing jobs affect pensionable salary?

No — pensionable salary is determined at the date of leaving the final EPF-covered employment. If your last job had basic+DA of ₹20,000, your pensionable salary is ₹15,000 (ceiling). Prior jobs’ salaries do not factor into pensionable salary (they affect service, not salary).

What if my employer reported incorrect salary to EPFO?

If the salary reported in ECR filings is incorrect (lower than actual), your pensionable salary may be understated. Raise a grievance via EPFiGMS with salary slips as evidence. EPFO can compel the employer to correct the filings. This is important particularly for HPS members where the 60-month average matters significantly.

Is pensionable salary gross salary or net salary?

Neither. Pensionable salary is the pre-tax basic + DA component of gross salary, capped at ₹15,000. Net salary (take-home after all deductions) is irrelevant to EPS pension calculation.

If my DA is merged into basic, does it still count?

Yes. If your employer has merged DA into basic salary and pays a consolidated “basic” figure, the entire consolidated basic is treated as basic for pensionable salary purposes. The distinction between basic and DA is only relevant when they are paid as separate line items.

What is the effect of the ₹15,000 ceiling on EPS pension across service years?

The ceiling creates a flat maximum pension growth curve above ₹15,000 salary. Two employees — one earning ₹15,000 and one earning ₹80,000 — receive exactly the same EPS pension for the same service under standard EPS. The higher earner’s additional salary above ₹15,000 generates zero additional pension (unless they are on HPS).

Will the ₹15,000 pensionable salary ceiling ever be raised?

The ceiling has been raised twice historically — from ₹5,000 to ₹6,500 in 2001, and from ₹6,500 to ₹15,000 in 2014. Government committees and trade unions periodically recommend raising it to ₹21,000 or higher. As of 2026, the ceiling remains at ₹15,000 — monitor EPFO notifications for future revisions.

What is the minimum pensionable salary?

There is no prescribed minimum pensionable salary — it equals actual basic+DA if below ₹15,000. However, the EPFO minimum pension of ₹1,000/month provides a floor for low-salary members whose formula-based pension falls below this amount.

How do I find out what EPFO has recorded as my pensionable salary?

Log in to the EPFO Member Portal at passbook.epfindia.gov.in. The EPS contribution column shows the monthly EPS contribution (8.33% × pensionable salary). Divide the EPS contribution by 0.0833 to get the pensionable salary for that month. Maximum shown will be ₹1,250 (= 8.33% × ₹15,000).

Where can I compute my EPS pension based on my pensionable salary?

Use the free EPS Pension Calculator India on Wealthpedia. Enter your actual or HPS pensionable salary, service years, and claim age — the calculator applies all EPFO rules and shows your monthly pension instantly, including Table D withdrawal benefit if applicable.

Disclaimer: The information on this page is for educational purposes only and does not constitute investment or financial advice. EPS rules and the pensionable salary ceiling are governed by EPFO regulations and may be updated by the Government of India. For personalised guidance, consult a SEBI-registered financial planner or visit your nearest EPFO office. Wealthpedia™ (Trademark Reg. No. 4910385) is not a SEBI-registered investment advisor. All mutual fund references on this site are for Direct Plan, Growth option only.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up