If there is one number every EPF-covered employee in India should know, it is 20. Twenty years of EPS-covered pensionable service is the threshold at which EPFO’s 2-year service bonus kicks in — a provision that silently and permanently boosts your monthly pension by an amount disproportionate to the additional years worked.

For an employee at 19 years, one more year of service does not just add the “normal” annual increment to their pension — it adds that increment plus an automatic 2-year bonus, effectively tripling the value of that single year.

This article is dedicated entirely to the 20-year milestone: how the calculation works, what the pension looks like at every salary level, how it compares with neighbouring milestones (15 and 25 years), and what the 2-year bonus actually means in rupee terms over a typical retirement.

Use the EPS Pension Calculator India to compute your exact pension based on your real service dates and salary — including the bonus calculation automatically.

Quick Summary

After 20 years of EPS-covered service, the 2-year bonus is triggered — EPFO adds 2 extra years to your pensionable service before applying the formula. At the ₹15,000 wage ceiling, 20 actual years becomes 22 pensionable years, giving a monthly pension of ₹4,714/month — calculated as (15,000 × 22) ÷ 70. This is a ₹1,500/month jump from the 15-year pension (₹3,214), nearly 50% higher despite only 5 additional actual years. This article explains the 2-year bonus mechanism in depth, provides salary-wise and early/deferred pension tables, compares 20 years against every other milestone, and explains why this is the single most valuable threshold in the entire EPS framework. Use the EPS Pension Calculator India to verify your figure.

Join Now →

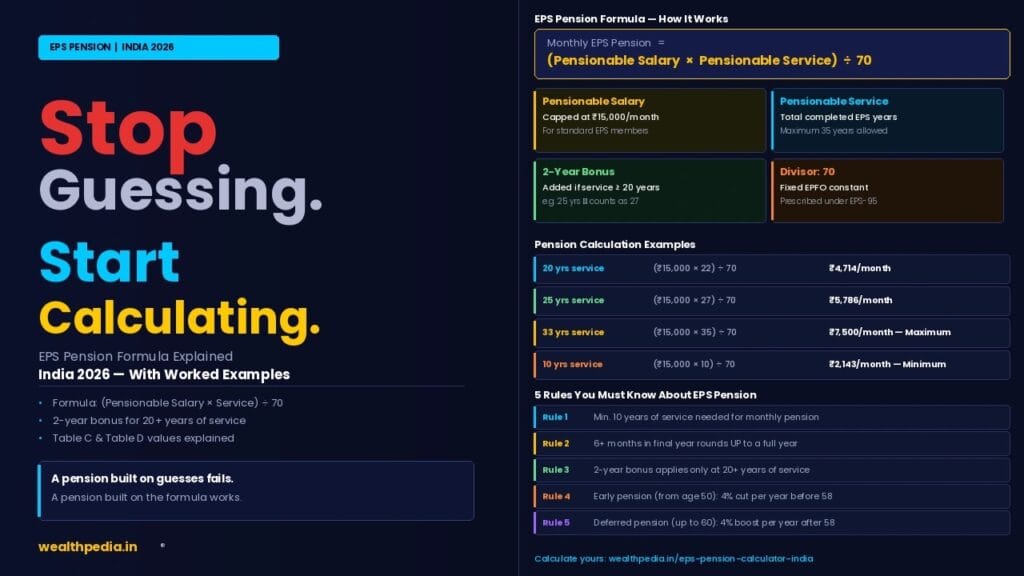

EPS Pension After 20 Years — The Calculation

The standard EPS pension formula is:

Monthly EPS Pension = (Pensionable Salary × Pensionable Service) ÷ 70

For exactly 20 years of actual service:

- Pensionable Salary: ₹15,000 (wage ceiling for most employees)

- Actual Service: 20 years

- 2-Year Bonus: YES — applies because service ≥ 20 years

- Pensionable Service used in formula: 20 + 2 = 22 years

- Divisor: 70 (fixed)

Monthly Pension = (15,000 × 22) ÷ 70 = ₹4,714.29 ≈ ₹4,714/month

This single calculation — ₹4,714/month — represents one of the most important numbers in EPS planning, because it marks the point where the 2-year bonus has fully activated and the pension growth curve steepens permanently.

For the complete formula breakdown including all components, see EPS Pension Formula Explained.

Understanding the 2-Year Bonus — Why 20 Years Is Special

EPFO’s EPS-95 rules state that if a member’s total pensionable service (after applying the standard 6-month rounding rule) reaches 20 years or more, the pensionable service used in the pension formula is increased by 2 years.

This is not an interest payment, not a tax benefit, and not a one-time bonus payment — it is a permanent recalibration of the formula’s service input, applied for the entire duration of the pension.

The Mechanics

| Actual Pensionable Service | Pensionable Service Used in Formula | Bonus Applied? |

|---|---|---|

| 18 years | 18 years | No |

| 19 years | 19 years | No |

| 20 years | 22 years | Yes (+2) |

| 21 years | 23 years | Yes (+2) |

| 22 years | 24 years | Yes (+2) |

The instant service crosses from 19 to 20 years, the formula input jumps from 19 to 22 — a jump of 3 years in a single step, even though only 1 additional actual year was worked.

Why This Matters in Rupee Terms

At ₹15,000 pensionable salary, each pensionable year is worth:

₹15,000 ÷ 70 = ₹214.29/month

So:

- Going from 18 to 19 actual years: +1 pensionable year → +₹214/month

- Going from 19 to 20 actual years: +1 actual year + 2 bonus years = +3 pensionable years → +₹643/month

The single year between 19 and 20 years of service is worth 3 times as much as any other individual year in the entire 35-year pensionable service range. This is the core insight of this article.

EPS Pension After 20 Years — Salary-Wise Calculation Table

For employees whose pensionable salary is below the ₹15,000 ceiling, here is the pension at 20 years of service (22 pensionable years with bonus):

| Monthly Pensionable Salary | Pensionable Service (with bonus) | Monthly EPS Pension |

|---|---|---|

| ₹6,500 | 22 years | ₹2,043/month |

| ₹8,000 | 22 years | ₹2,514/month |

| ₹10,000 | 22 years | ₹3,143/month |

| ₹12,000 | 22 years | ₹3,771/month |

| ₹14,000 | 22 years | ₹4,400/month |

| ₹15,000 | 22 years | ₹4,714/month |

Notice that even at the lowest historical wage ceiling (₹6,500), the 2-year bonus still produces a pension of over ₹2,000/month — well above the EPFO minimum pension floor of ₹1,000/month. For more on the floor, see What Is the Minimum EPS Pension in India?

20 Years vs Every Other Major Milestone

This table places the 20-year pension in context against all the other major service milestones, at the ₹15,000 ceiling:

| Actual Service | Pensionable Service (with bonus where applicable) | Monthly Pension | Step-Up from Previous Milestone |

|---|---|---|---|

| 10 years | 10 (no bonus) | ₹2,143 | — |

| 15 years | 15 (no bonus) | ₹3,214 | +₹1,071 (5 years → +₹1,071) |

| 20 years | 22 (+2 bonus) | ₹4,714 | +₹1,500 (5 years → +₹1,500) |

| 25 years | 27 (+2 bonus) | ₹5,786 | +₹1,072 (5 years → +₹1,072) |

| 30 years | 32 (+2 bonus) | ₹6,857 | +₹1,071 (5 years → +₹1,071) |

| 33 years | 35 (+2 bonus, max) | ₹7,500 | +₹643 (3 years → +₹643) |

The pattern is unmistakable: every 5-year jump produces approximately ₹1,071–₹1,072 in additional pension — except the 15-to-20-year jump, which produces ₹1,500. The extra ₹429 (= 2 years × ₹214.29) is the pure effect of the 2-year bonus newly applying at the 20-year mark.

For the 15-year analysis, see EPS Pension After 15 Years Service. For the 25-year analysis, see EPS Pension After 25 Years Service.

The Single-Year Comparison — 19 Years vs 20 Years

To isolate the bonus effect precisely, compare 19 years (no bonus) directly against 20 years (bonus applies):

| Metric | 19 Years | 20 Years | Difference |

|---|---|---|---|

| Actual Service | 19 | 20 | +1 year |

| Pensionable Service Used | 19 | 22 | +3 years |

| Monthly Pension | ₹4,071 | ₹4,714 | +₹643/month |

| Annual Pension | ₹48,852 | ₹56,568 | +₹7,716/year |

| Over 22-year retirement | ₹10,74,744 | ₹12,44,496 | +₹1,69,752 |

One additional year of work — going from 19 to 20 years of service — adds approximately ₹1.70 lakh to lifetime pension income (over a 22-year retirement at age 58–80). This is among the highest-leverage single decisions an EPS member can make regarding their career timeline.

Practical Implication

If you are at 19 years and 6+ months of service (which rounds up to 20 years under EPFO’s 6-month rule), you have already crossed the 20-year threshold and qualify for the bonus. If you are at 19 years and 5 months or less, working just enough additional months to reach the 19 years 6 months mark — rounding up to 20 — unlocks the bonus.

For the complete rounding rules, see What Is Pensionable Service Under EPS?

EPS Pension After 20 Years — Early Pension Options (Age 50–57)

Members with 20 years of service who have ceased EPF-covered employment can claim early pension from age 50, with a permanent 4% reduction per year before 58.

Early Pension = Base Pension × (1 − 0.04 × years before 58)

Early Pension Table — Base Pension ₹4,714/month (20 Years, ₹15,000 Salary)

| Claim Age | Years Before 58 | Reduction % | Monthly Pension | Annual Pension |

|---|---|---|---|---|

| 58 (standard) | 0 | 0% | ₹4,714 | ₹56,568 |

| 57 | 1 | 4% | ₹4,525 | ₹54,300 |

| 56 | 2 | 8% | ₹4,337 | ₹52,044 |

| 55 | 3 | 12% | ₹4,148 | ₹49,776 |

| 54 | 4 | 16% | ₹3,960 | ₹47,520 |

| 53 | 5 | 20% | ₹3,771 | ₹45,252 |

| 52 | 6 | 24% | ₹3,583 | ₹42,996 |

| 51 | 7 | 28% | ₹3,394 | ₹40,728 |

| 50 | 8 | 32% | ₹3,206 | ₹38,472 |

Even at the maximum 32% reduction (claiming at age 50), a member with 20 years of service receives ₹3,206/month — still ₹1,020/month more than the un-reduced pension at 10 years (₹2,143). The 2-year bonus advantage persists even after early pension reductions.

For the complete early pension analysis and break-even ages, see EPS Early Pension Before 58: Reduction Rules Explained.

EPS Pension After 20 Years — Deferred Pension Options (Age 59–60)

Members can also defer their pension claim beyond 58, receiving a permanent 4% enhancement per year of deferment (maximum 2 years, to age 60).

Deferred Pension = Base Pension × (1 + 0.04 × years after 58)

| Claim Age | Years After 58 | Enhancement | Monthly Pension | Annual Pension |

|---|---|---|---|---|

| 58 (standard) | 0 | 0% | ₹4,714 | ₹56,568 |

| 59 | 1 | 4% | ₹4,903 | ₹58,836 |

| 60 | 2 | 8% | ₹5,091 | ₹61,092 |

The maximum deferred pension at 20 years of service is ₹5,091/month — already higher than the standard (non-deferred) pension at 25 years without bonus consideration (which would be ₹4,464 if hypothetically the bonus didn’t apply — illustrating again how powerful the 20-year threshold is).

For the complete deferred pension analysis, see Deferred EPS Pension After 58: Benefits Explained.

What If Service Is 20 Years and Some Months?

The 6-month rounding rule applies at the 20-year mark with particular significance, since it determines whether the bonus applies at all:

| Actual Service | Rounded Service | Bonus? | Pensionable Service Used | Monthly Pension at ₹15,000 |

|---|---|---|---|---|

| 19 years 4 months | 19 years | No | 19 | ₹4,071 |

| 19 years 5 months | 19 years | No | 19 | ₹4,071 |

| 19 years 6 months | 20 years | Yes | 22 | ₹4,714 |

| 19 years 8 months | 20 years | Yes | 22 | ₹4,714 |

| 20 years 0 months | 20 years | Yes | 22 | ₹4,714 |

| 20 years 6 months | 21 years | Yes | 23 | ₹4,929 |

The most consequential row in this table is 19 years 6 months — this is the exact point where rounding up to 20 years unlocks the 2-year bonus. An employee at 19 years 5 months who works just 1 more month crosses this threshold and gains ₹643/month for life.

This single-month decision is more financially impactful than almost any other timing choice in an EPS member’s career.

Combined Retirement Picture at 20 Years — EPF + EPS

At 20 years of service with ₹15,000 pensionable salary (illustrative basic+DA of ₹20,000 for EPF calculations):

EPF Corpus (Approximate):

- Monthly EPF credit: ~₹3,134 (employee 12% + employer 3.67% on ₹20,000 basic)

- Over 20 years at 8.25% compound interest: approximately ₹18–22 lakh

EPS Pension:

- ₹4,714/month for life from age 58

- Over a 22-year retirement: approximately ₹12.44 lakh in total nominal pension

Combined package at 20 years:

- EPF lump sum: ₹18–22 lakh

- EPS pension: ₹4,714/month guaranteed floor income

This combination forms a substantial retirement foundation, with EPS providing the inflation-resistant floor and EPF providing flexible capital. See EPF vs EPS: Key Differences Explained for the complete breakdown of how both funds interact.

Family Pension at 20 Years of Service

If a member with 20 years of EPS service (and the associated 2-year bonus pension of ₹4,714/month) dies, their family receives: Beneficiary Rate Monthly Amount Widow / Widower 50% of member’s pension ₹2,357/month Each Child (up to 2) 25% of member’s pension ₹1,179/month Orphan (both parents deceased) 75% of member’s pension ₹3,536/month

The 2-year bonus flows through to family pension as well — a widow of a member with exactly 20 years of service receives ₹2,357/month, compared to ₹2,036/month if the bonus had not applied (hypothetically, at 20 years without bonus). For the complete family pension rules, see EPS Family Pension Rules Explained.

Strategic Decision-Making Around the 20-Year Threshold

If You Are at 18–19 Years and Considering a Career Change

The single most financially significant piece of advice in this entire article: if you are close to 19 years 6 months of pensionable service, consider delaying any career transition until you cross this threshold.

Whether the transition is:

- Moving to self-employment or entrepreneurship

- Switching to a non-EPF-covered employer

- Taking an extended career break

- Early retirement under VRS

…crossing 19 years 6 months first locks in the 2-year bonus permanently — adding ₹643/month for life (₹1.70 lakh over a typical retirement), for as little as 1–2 additional months of EPF-covered employment.

If You Are Negotiating a VRS Package

Employees being offered Voluntary Retirement Scheme (VRS) packages should check their exact pensionable service before accepting. If the VRS effective date falls just before the 19 years 6 months mark, negotiating a 1–2 month delay in the effective date — if possible — could secure the 2-year bonus for life.

If You Are Comparing Job Offers

When evaluating a job change that would interrupt EPF-covered service (e.g., moving to a startup not yet EPF-registered, or to a government role without EPS), check your current pensionable service. If you are within reach of 20 years at your current employer, completing that milestone before switching preserves the bonus permanently — provided service from both employers combines correctly via UAN or Scheme Certificate. See Scheme Certificate vs EPS Withdrawal for how service preservation works across employer transitions.

If You Are Planning for FIRE

For FIRE-focused employees, the 20-year EPS milestone often coincides with the early-to-mid career phase when major life decisions (career breaks, sabbaticals, geographic moves) are being considered. Factoring in the ₹1,500/month pension jump (vs ₹1,071 for other 5-year increments) into your FIRE corpus calculations can meaningfully reduce the corpus required, since EPS pension functions as guaranteed, inflation-resilient floor income. Use the Multi-Goal FIRE Planner to model how the 20-year EPS pension fits into your broader retirement plan.

EPS Pension After 20 Years — Higher Pension Scheme Comparison

For members who were approved under the Higher Pension Scheme (HPS), the 2-year bonus rule applies identically — only the pensionable salary changes from ₹15,000 to the actual 60-month average salary.

HPS Example at 20 Years of Service

- Average salary (last 60 months): ₹50,000

- Actual service: 20 years

- 2-year bonus applies → Pensionable service = 22 years

- HPS Pension = (50,000 × 22) ÷ 70 = ₹15,714/month

Compared to standard EPS at the same service (₹4,714/month), HPS delivers more than 3.3 times the pension — for the exact same 20 years and the exact same bonus mechanism. The bonus is proportionally even more valuable under HPS because it applies to a much larger salary base.

For the complete HPS guide, see EPS Higher Pension Scheme: Eligibility & Calculation.

Why 20 Years Is Often Called the “EPS Sweet Spot”

Financial planners and EPFO advisory content frequently refer to the 20-year mark as the “EPS sweet spot” for several converging reasons:

1. It is the bonus activation threshold — no other single year of service delivers 3x the normal pensionable-year value.

2. It typically falls mid-career — for an employee starting work at 23–25, the 20-year mark falls around age 43–45, a common point for career reassessment, geographic moves, or family planning decisions.

3. It significantly de-risks pre-retirement transitions — an employee with 20+ years of EPS service who later moves to self-employment, consulting, or entrepreneurship retains a meaningful guaranteed pension floor (₹4,714/month minimum at ₹15,000 salary) regardless of how their subsequent career unfolds.

4. It compounds with deferred pension — a member with 20 years of service who defers to age 60 receives ₹5,091/month — exceeding what a 22-year-service member would receive at standard age 58 without deferral (₹5,143… actually very close), illustrating how the bonus and deferral interact favourably.

EPS Pension After 20 Years — Quick Reference Summary

| Metric | Value (₹15,000 Salary) |

|---|---|

| Actual Service | 20 years |

| 2-Year Bonus Applies | Yes (+2 years) |

| Pensionable Service Used | 22 years |

| Monthly Pension at 58 | ₹4,714 |

| Monthly Pension at 50 (early) | ₹3,206 (−32%) |

| Monthly Pension at 60 (deferred) | ₹5,091 (+8%) |

| Annual Pension at 58 | ₹56,568 |

| 22-year retirement total | ₹12,44,496 |

| Improvement vs 19 years | +₹643/month |

| Improvement vs 15 years | +₹1,500/month |

| Widow pension (50%) | ₹2,357/month |

| Child pension (25% each) | ₹1,179/month |

| Orphan pension (75%) | ₹3,536/month |

Frequently Asked Questions — EPS Pension After 20 Years

How much EPS pension will I get after 20 years of service?

With 20 years of EPS service at the ₹15,000 wage ceiling, your monthly pension is ₹4,714/month. The calculation: 20 years + 2-year bonus (since service ≥ 20 years) = 22 pensionable years; (15,000 × 22) ÷ 70 = ₹4,714. Use the EPS Pension Calculator India for your personalised figure.

What is the 2-year bonus and why does it apply at 20 years?

EPFO’s EPS-95 rules state that if total pensionable service reaches 20 years or more (after rounding), 2 additional years are added to the pensionable service used in the pension formula. So 20 actual years becomes 22 pensionable years in the formula — a permanent enhancement applied for the life of the pension.

How much extra pension does the 2-year bonus give?

At ₹15,000 pensionable salary, each pensionable year is worth ₹214.29/month (= 15,000 ÷ 70). The 2-year bonus adds 2 × ₹214.29 = ₹428.57/month (rounds to approximately ₹429/month) compared to what the pension would be without the bonus.

What is the EPS pension for 19 years vs 20 years of service?

At 19 years (no bonus): (15,000 × 19) ÷ 70 = ₹4,071/month. At 20 years (with bonus, 22 pensionable years): (15,000 × 22) ÷ 70 = ₹4,714/month. The difference is ₹643/month — for just 1 additional year of actual service, because the bonus adds 2 more years on top.

What is the EPS pension for 20 years at ₹10,000 salary?

Pensionable Service = 20 + 2 bonus = 22 years. Monthly Pension = (10,000 × 22) ÷ 70 = ₹3,143/month.

Can I claim EPS pension at 20 years of service before age 58?

Yes — from age 50, with a 4% reduction per year before 58. At age 50 (8 years early, 32% reduction): ₹4,714 × 0.68 = ₹3,206/month. See EPS Early Pension Before 58 for the full table.

What is the EPS pension for 20 years and 6 months of service?

EPFO rounding: 6 months ≥ 6 → rounds up to 21 years. With the 2-year bonus: 21 + 2 = 23 pensionable years. Monthly Pension = (15,000 × 23) ÷ 70 = ₹4,929/month — ₹214 more than exactly 20 years.

What is the widow pension for a member with 20 years of EPS service?

Widow pension = 50% of the member’s pension = 50% × ₹4,714 = ₹2,357/month, for life or until remarriage. Each child receives 25% = ₹1,179/month (up to 2 children, up to age 25). See EPS Family Pension Rules.

Is it worth waiting a few extra months to cross 20 years of EPS service?

Yes — emphatically. If you are at 19 years 5 months, working just 1 more month brings you to 19 years 6 months, which rounds up to 20 years and unlocks the 2-year bonus. This adds ₹643/month for life — over ₹1.70 lakh in additional lifetime pension over a 22-year retirement, for just 1 month of additional service.

What is the EPS pension at age 60 (deferred) for 20 years of service?

Base Pension = ₹4,714/month. Deferred to 60 (2 years, +8%): ₹4,714 × 1.08 = ₹5,091/month. See Deferred EPS Pension After 58.

How does 20 years of service compare to 25 years?

At 25 years: Pensionable Service = 25 + 2 bonus = 27 years → Monthly Pension = (15,000 × 27) ÷ 70 = ₹5,786/month. Compared to 20 years (₹4,714/month), the difference is +₹1,072/month — close to the “normal” 5-year increment of ₹1,071, since both milestones already include the bonus. See EPS Pension After 25 Years.

What is the EPS pension for 20 years at ₹12,000 salary?

Pensionable Service = 22 years (with bonus). Monthly Pension = (12,000 × 22) ÷ 70 = ₹3,771/month.

If I have 18 years of service with one employer and switch jobs, do I lose the chance at the 2-year bonus?

Not necessarily — if you transfer your EPF/EPS account via UAN to your new employer, your 18 years of service carries forward and combines with future service at the new employer. Once your combined service reaches 20 years (across both employers), the 2-year bonus applies. The key is ensuring service transfer is completed correctly.

What is the maximum pension achievable starting from the 20-year bonus base?

Starting from 22 pensionable years at 20 actual years (₹4,714/month), continuing to work increases the pension by ₹214.29/month per additional year, up to the maximum of 35 pensionable years (33 actual years + 2 bonus) = ₹7,500/month. From 20 to 33 actual years (13 more years), the pension grows from ₹4,714 to ₹7,500 — an increase of ₹2,786/month.

Does the 2-year bonus apply to the Higher Pension Scheme as well?

Yes. The 2-year bonus rule is identical for HPS members — only the pensionable salary changes (60-month average instead of ₹15,000 ceiling). At 20 years of service with a ₹50,000 average salary under HPS: (50,000 × 22) ÷ 70 = ₹15,714/month — over 3 times the standard EPS amount for the same service and bonus.

What is the EPS pension for 20 years at ₹8,000 salary?

Pensionable Service = 22 years (with bonus). Monthly Pension = (8,000 × 22) ÷ 70 = ₹2,514/month.

Is 20 years the only threshold where a bonus applies?

Yes. The 2-year bonus is a one-time addition that applies once total pensionable service reaches 20 years — it does not apply again at 30, 40, or any other threshold. The bonus is added once and remains as part of the pensionable service count (capped at the 35-year maximum) for all higher service levels.

What is the annual EPS pension income at 20 years of service?

Monthly Pension = ₹4,714. Annual = ₹4,714 × 12 = ₹56,568/year. This is generally within or close to the basic exemption limit under the new income tax regime for many retirees, meaning little to no tax liability on this income alone.

How much EPF corpus typically accompanies 20 years of EPS service?

For an employee with ₹20,000 basic+DA over 20 years, the EPF corpus (employee 12% + employer 3.67%, compounded at approximately 8.25% p.a.) could be approximately ₹18–22 lakh. This is separate from and in addition to the EPS pension of ₹4,714/month. See EPF vs EPS: Key Differences Explained.

What is the EPS pension for 20 years and 4 months of service?

EPFO rounding: 4 months < 6 → dropped. Counted as 20 years. Monthly Pension = (15,000 × 22) ÷ 70 = ₹4,714/month — same as exactly 20 years, since the bonus already applies at 20 years regardless of additional months below 6.

Can I withdraw a lump sum at 20 years of EPS service instead of taking monthly pension?

No. The Table D withdrawal benefit is only available for service below 10 years. At 20 years, you are far past this threshold and must take monthly pension (from age 50 with reduction, or 58 standard, or 59–60 with enhancement). There is no lump-sum withdrawal option for EPS once past 10 years of service.

What is the orphan pension for a member with 20 years of EPS service?

If both parents are deceased, orphan pension is 75% of the member’s pension = 75% × ₹4,714 = ₹3,536/month per orphan (maximum 2 orphans simultaneously, up to age 25, or for life if permanently disabled). See EPS Family Pension Rules Explained.

Is there a difference in pensionable service calculation for someone who joined EPS before September 2014 and reached 20 years after?

No — the pensionable service counting method (months, 6-month rounding, 2-year bonus at 20 years, 35-year maximum) is identical regardless of when the member joined. The wage ceiling change in September 2014 affects pensionable salary (the ceiling applicable at the date of retirement/exit), not pensionable service counting.

What is the EPS pension for 20 years of service combined with early pension at age 55?

Base Pension = ₹4,714/month (20 years, with bonus). Claimed at 55 (3 years early, 12% reduction): ₹4,714 × 0.88 = ₹4,148/month. This is still significantly higher than the un-reduced 15-year pension (₹3,214/month) — illustrating that even with an early pension reduction, the 2-year bonus from reaching 20 years more than compensates.

Where can I check exactly how close I am to the 20-year EPS milestone?

Log in to the EPFO Member Portal at passbook.epfindia.gov.in with your UAN. The EPS contribution column shows monthly credits — count the total months and convert to years and months. If you are at 19 years 5 months or less, calculate exactly how many more months are needed to reach 19 years 6 months (the rounding threshold that unlocks the bonus). Alternatively, use the EPS Pension Calculator India by entering your joining date — it computes your current pensionable service and projects when you will cross the 20-year threshold.

Disclaimer: The information on this page is for educational purposes only and does not constitute investment or financial advice. EPS rules — including the 2-year service bonus — are governed by EPFO regulations under EPS-95 and may be updated by the Government of India. For personalised guidance, consult a SEBI-registered financial planner or visit your nearest EPFO office. Wealthpedia™ (Trademark Reg. No. 4910385) is not a SEBI-registered investment advisor. All mutual fund references on this site are for Direct Plan, Growth option only.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up