India now has over 9 crore active SIP accounts and ₹81.92 lakh crore in mutual fund AUM. Yet most of those investors are still calculating their SIPs wrong — using tools that ignore inflation, ignore goal timelines, and ignore the one variable that matters most: whether the number at the end is actually enough.

The Number That Looks Good but Means Nothing

Here is a scene that happens every single day in India.

Someone opens a standard SIP calculator. They type in ₹10,000 per month, 12% expected returns, 20 years. The calculator spits back a number: ₹99.9 lakh.

They feel good. Nearly ₹1 crore. Not bad.

They close the tab and do nothing else.

What that calculator did not tell them:

- At 6% inflation, ₹99.9 lakh in 2046 has the purchasing power of approximately ₹31 lakh in today’s money

- If their retirement needs ₹50,000/month in today’s terms, they will need roughly ₹1.6 crore in 2046 just for the first year of expenses

- That corpus runs out in under 13 years if withdrawn at the inflation-adjusted rate with no equity growth post-retirement

- Their actual shortfall is not zero — it is ₹60+ lakh

This is what a standard SIP calculator does. It shows you a large number, makes you feel financially responsible, and sends you off with false confidence.

A SIP portfolio calculator does something fundamentally different. It connects your monthly investment to your actual goals, accounts for what money will genuinely be worth in the future, and tells you not just what you will accumulate — but whether that accumulation is actually sufficient for the life you are planning.

This article explains exactly how a SIP portfolio calculator works, what inputs it needs, what outputs to trust, and how to use it to build a portfolio that maps to your real financial life — not the sanitised version that fits neatly into a single-input tool.

The State of SIP Investing in India: A ₹81 Lakh Crore Paradox

Before getting into calculators, the scale of what is happening in Indian mutual funds needs to be understood — because it frames precisely why better tools matter.

As of April 2026, the Indian mutual fund industry manages ₹81.92 lakh crore in AUM — a figure that was just ₹14.22 lakh crore a decade ago. That is nearly a 6x increase in ten years, driven largely by retail SIP investors.

Monthly SIP contributions crossed ₹29,361 crore in September 2025 — up from just ₹8,023 crore in January 2021. The number of active SIP accounts has crossed 9 crore, with over 10 crore accounts registered by October 2024. AMFI projects that by 2047, industry AUM could expand to ₹2,791 lakh crore — a 35x increase — with over 26 crore investors.

The mutual fund industry has grown at a 20% CAGR over the past decade. 90% of transactions now happen online. Fintech platforms and smartphones have brought SIP investing to Tier 2 and Tier 3 cities in ways that were impossible five years ago.

This is the good news.

The concerning part: most of those 9 crore SIP investors are using basic calculators that treat every ₹10,000 SIP as identical — regardless of whether it is meant for retirement, a child’s education, or a house down payment three years away. The tool being used to plan a 25-year financial life is the same tool used to calculate a 5-year car fund.

That mismatch is where most Indian financial plans fail — not at the investing stage, but at the planning stage.

Understanding how inflation silently destroys your SIP corpus is the first step toward using a SIP portfolio calculator correctly. The second step is building a portfolio structured around goals, not just around a lump monthly number.

What Is a SIP Portfolio Calculator — and How Is It Different?

A basic SIP calculator answers one question: If I invest ₹X per month for Y years at Z% return, how much will I accumulate?

A SIP portfolio calculator answers a fundamentally different set of questions:

- How much corpus do I need for each of my financial goals?

- Given that corpus target, what monthly SIP is required today?

- How does inflation change that corpus target and required SIP?

- What happens to my corpus if I step up the SIP by 10% each year?

- Am I currently on track — or behind — for each goal separately?

- If I am behind, how much more do I need to invest, or how many more years do I need to stay invested?

The difference is the direction of calculation. A basic calculator goes forward (input → output). A SIP portfolio calculator goes backward from the goal (goal → required input). One tells you what you will get. The other tells you what you need.

The Wealthpedia SIP Comparison Calculator lets you run multiple SIP scenarios side by side — a fundamental feature missing from most basic tools. The Multi-Goal FIRE Planner goes further, modelling all your goals simultaneously and showing you whether your total portfolio is on track across every objective.

The Five Inputs That Actually Matter in a SIP Portfolio Calculator

Most SIP calculators ask for three inputs: monthly amount, return rate, tenure. A proper SIP portfolio calculator needs five critical inputs — and the last two are the ones that most Indians skip.

Input 1: Monthly SIP Amount

The most visible input and the most obvious. But there is an important distinction: are you entering a flat amount or a step-up amount?

A flat ₹10,000 SIP at 12% CAGR over 25 years builds ₹1.89 crore. That same ₹10,000 with a 10% annual step-up builds ₹3.79 crore — exactly double — with a total contribution of only ₹39.7 lakh versus ₹30 lakh for the flat SIP. The additional ₹9.7 lakh of extra contributions produced ₹1.90 crore of additional corpus.

Any SIP portfolio calculator that does not support step-up projections is telling you half the story. As we showed in the best SIP allocation strategy guide, the step-up SIP is the single most powerful lever in long-term wealth creation — not fund selection, not timing, not which AMC you choose.

Input 2: Expected Rate of Return

The return assumption is where most calculators — and most investors — go wrong in two opposite directions.

Too optimistic: Using 18–20% returns based on recent mid-cap or small-cap fund performance. Historical data from the Nifty 500 TRI shows a 30-year CAGR of 15.2% — but this includes two catastrophic crashes (2001–2002 and 2008) and multiple 20%+ down years. For planning purposes, 12% for equity, 7.5% for debt, and 10–11% for blended portfolios are appropriate conservative assumptions.

Too pessimistic: Using 8–9% returns for an all-equity portfolio because you have been burned before. At 8%, a ₹10,000/month SIP over 25 years builds ₹95.1 lakh — not enough for most retirement scenarios. The conservative assumption becomes self-defeating.

The right approach: use scenario analysis — calculate your corpus at 10%, 12%, and 14% CAGR, and plan to be sufficient at the 10% scenario. That way, anything above 10% is a bonus, not a requirement.

Input 3: Investment Tenure

The most underestimated input. Most investors focus obsessively on return rate (which they cannot control) and neglect tenure (which they completely control).

The mathematics are unforgiving. A ₹10,000/month SIP at 12% CAGR:

| Tenure | Total Invested | Final Corpus | Wealth Created |

|---|---|---|---|

| 10 years | ₹12,00,000 | ₹23.2 lakh | ₹11.2 lakh |

| 15 years | ₹18,00,000 | ₹50.5 lakh | ₹32.5 lakh |

| 20 years | ₹24,00,000 | ₹99.9 lakh | ₹75.9 lakh |

| 25 years | ₹30,00,000 | ₹1.89 crore | ₹1.59 crore |

| 30 years | ₹36,00,000 | ₹3.53 crore | ₹3.17 crore |

From Year 20 to Year 30 — one additional decade — the corpus almost quadruples from ₹99.9 lakh to ₹3.53 crore, on only ₹12 lakh of additional contributions. This is the compounding curve effect. Every year of delay at the beginning, or early termination at the end, costs disproportionately more than the middle years.

This is precisely why starting a SIP for a child’s education from birth — rather than waiting until the child is 5 or 8 — can save ₹15–20 lakh in additional contributions for the same corpus target.

Input 4: Inflation Rate

The most skipped input in Indian SIP calculators — and the one that changes everything.

India’s average CPI inflation from 1995 to 2025 has been approximately 6.25%. Healthcare inflation runs at 12–15% (as highlighted by retirement planners quoted in Business Standard). Education inflation in India runs at 10–12% annually, consistently above general CPI.

At 6% general inflation, your financial targets change dramatically:

| Today’s Monthly Need | In 10 Years | In 20 Years | In 30 Years |

|---|---|---|---|

| ₹30,000 | ₹53,726 | ₹96,214 | ₹1,72,304 |

| ₹50,000 | ₹89,542 | ₹1,60,357 | ₹2,87,174 |

| ₹75,000 | ₹1,34,313 | ₹2,40,535 | ₹4,30,761 |

| ₹1,00,000 | ₹1,79,085 | ₹3,20,714 | ₹5,74,349 |

A family spending ₹75,000/month today will need ₹2.40 lakh/month in 20 years just to maintain the same lifestyle. The retirement corpus required to sustain ₹2.40 lakh/month for 25 years at a 4% safe withdrawal rate is ₹7.22 crore — not the ₹2–3 crore that most standard SIP calculator results suggest.

The SIP Calculator with Inflation at Wealthpedia addresses this gap directly — displaying both nominal and inflation-adjusted returns side by side, so you see what your corpus actually buys, not just what it nominally accumulates to.

Input 5: Goal-Specific Target Corpus

The final and most important input: what are you actually trying to achieve?

Most Indians use SIP calculators without a specific corpus target. They pick an arbitrary round number (₹1 crore) and work backwards. But ₹1 crore means very different things depending on:

- Whether it is targeted for 2030 or 2045

- Whether it is meant to fund retirement, education, or a down payment

- What inflation rate applies to that specific goal

- What safe withdrawal rate is assumed for ongoing expenses

A proper SIP portfolio calculator starts with the goal — uses the FIRE Number Calculator for retirement, the child education SIP planner for education goals, the Retirement Corpus Calculator for the overall picture — and then works backward to the required monthly SIP.

The Three SIP Portfolio Calculator Scenarios Every Indian Investor Must Model

Theory is useful. Numbers are more useful. Here are three detailed scenarios that illustrate exactly how a SIP portfolio calculator changes the planning conversation.

Scenario 1: Rohan, 28, IT Professional in Bengaluru, ₹1.2 lakh/month in-hand

Goal: Retire at 52 with enough corpus to sustain ₹80,000/month in today’s terms.

Step 1 — Find the inflation-adjusted retirement expense:

₹80,000/month today at 6% inflation for 24 years = ₹3.24 lakh/month at retirement.

Step 2 — Calculate the required corpus:

At a 4% safe withdrawal rate for a 30-year retirement, corpus needed = ₹3.24 lakh × 12 ÷ 0.04 = ₹9.72 crore.

Step 3 — Calculate the required SIP:

To accumulate ₹9.72 crore in 24 years at 12% CAGR (flat SIP): ₹67,000/month — clearly out of reach at ₹1.2 lakh income.

Step 4 — Model the step-up SIP:

Starting SIP of ₹20,000/month with 15% annual step-up over 24 years at 12% CAGR = ₹9.8 crore. Achievable.

Step 5 — Validate sustainability:

Using the Safe Withdrawal Rate Calculator: ₹9.8 crore at 3.5% withdrawal rate = ₹28.8 lakh/year = ₹2.4 lakh/month. Adjusting for the equity component of the corpus continuing to grow, sustainability exceeds 30 years with high probability.

What changed: Rohan discovered that a flat ₹20,000 SIP builds only ₹3.5 crore — a ₹6.2 crore shortfall — while a step-up SIP starting at the same ₹20,000 gets him to his goal. The step-up makes the impossible achievable. Without a proper SIP portfolio calculator, Rohan would have invested ₹20,000 flat, felt responsible, and discovered the shortfall only at age 48 — too late to meaningfully course-correct.

Scenario 2: Priya & Karthik, Both 36, Dual Income Family in Chennai, 1 Child Age 4

Goal 1: Child’s engineering/MBA education in 15 years (private institution, target ₹50 lakh in today’s terms at 10% education inflation = ₹2.09 crore in 2041).

Goal 2: Retire at 58 with ₹1.2 lakh/month in today’s terms.

Goal 3: House upgrade in 8 years (need ₹30 lakh own contribution in today’s terms = ₹47.9 lakh at 6% inflation in 8 years).

Child’s Education SIP:

Required corpus: ₹2.09 crore in 15 years.

Required SIP at 12% CAGR with 10% step-up starting ₹7,500/month = ₹2.11 crore.

House Upgrade SIP:

Required: ₹47.9 lakh in 8 years.

Mix of conservative hybrid (8% blended return) = SIP of ₹33,000/month required.

Or: ₹20,000/month SIP with ₹10 lakh lump sum parked today at 8% = ₹47.6 lakh.

Retirement SIP:

Retirement in 22 years. ₹1.2 lakh/month in today’s terms = ₹4.32 lakh/month at retirement at 6% inflation.

Corpus required for 30-year retirement at 4% SWR: ₹12.96 crore.

Required SIP: ₹25,000/month starting with 12% annual step-up over 22 years = ₹13.2 crore.

Total starting monthly SIP requirement: ₹7,500 (education) + ₹20,000 (house) + ₹25,000 (retirement) = ₹52,500/month — approximately 23% of combined income. Achievable at dual income of ₹2.25 lakh+ combined, and reduces sharply once the house goal is funded in 8 years.

Without a SIP portfolio calculator treating each goal separately, Priya and Karthik would have pooled everything into one or two SIPs — then faced the impossible decision of whether to withdraw for the house down payment in 2031, knowing it might derail the education goal or retirement corpus.

Scenario 3: Vikram, 45, Business Owner in Mumbai, Starting Late

The scenario many Indians dread — but which is more common than anyone admits.

Vikram is 45. He has been meaning to invest seriously “once things settle down” since he was 35. He has ₹25 lakh in FD, ₹18 lakh in PPF (accumulated over years), and wants to retire at 60 with ₹1 lakh/month in today’s terms.

Reality check:

₹1 lakh/month today at 6% inflation for 15 years = ₹2.4 lakh/month at retirement.

Corpus required for 25-year retirement at 3.5% withdrawal rate: ₹8.23 crore.

What he already has (projected to age 60):

- ₹25 lakh FD reinvested at 7% for 15 years = ₹68.8 lakh

- ₹18 lakh PPF compounded at 7.1% for 15 years = ₹50.7 lakh

- Subtotal: ₹1.19 crore

Gap: ₹8.23 crore − ₹1.19 crore = ₹7.04 crore to be built through SIPs in 15 years.

Required SIP: ₹7.04 crore at 12% CAGR over 15 years requires approximately ₹1.56 lakh/month — flat. Not feasible.

With 15% annual step-up starting at ₹60,000: Accumulates approximately ₹6.9 crore over 15 years. Combined with existing corpus: ₹8.09 crore — close enough with modest lifestyle adjustments.

But there is a better path: Vikram can also use Voluntary Provident Fund (VPF) — at 8.25% EEE, contributing an extra ₹50,000/month through his business reduces his effective SIP requirement while generating better risk-adjusted returns than taxable debt funds.

Revised plan: ₹50,000 VPF + ₹50,000 SIP (equity index, 15% step-up) + ₹20,000 SIP (conservative hybrid, flat) = ₹1.2 lakh/month.

This scenario illustrates precisely why the question is not whether you can retire comfortably on ₹2 crore or ₹5 crore — it depends on your specific expenses, inflation exposure, retirement duration, and withdrawal rate. A SIP portfolio calculator makes these dependencies visible.

How to Use a SIP Portfolio Calculator: The 6-Step Framework

Step 1: List All Your Financial Goals with Timelines

Before opening any calculator, write down every financial goal:

- Emergency fund: ₹X lakh (when: immediately, if not already built)

- Child education: ₹X lakh in today’s terms (when: Year 2038, 2041, etc.)

- House down payment: ₹X lakh in today’s terms (when: Year 2029, 2030, etc.)

- Retirement/FIRE: ₹X lakh/month in today’s terms (when: Age 50, 55, 60)

- Healthcare corpus: ₹X lakh (when: ongoing, growing with medical inflation)

- Any other goal: wedding, legacy, travel sabbatical, etc.

This step is the most skipped. And it is the only step that actually matters. Everything else — fund selection, SIP amount, allocation split — is secondary to knowing what you are trying to achieve and when.

Use the Goal-Based Investment Calculator to formalise each goal with its own corpus target, timeline, and required SIP.

Step 2: Apply the Correct Inflation Rate to Each Goal

Not all goals inflate at the same rate: Goal Type Inflation Rate to Use General lifestyle / retirement income 6–7% Child education (engineering/MBA) 10–12% Healthcare / medical expenses 12–15% Real estate / housing costs 6–8% Travel / leisure 5–6% Wedding expenses 8–10%

Using 6% inflation for an education goal that is inflating at 12% produces a corpus target that is 50–70% too low over a 15-year horizon. This is the silent planning error that causes parents to discover — in the child’s Class 11 — that the education SIP they have been running for a decade is ₹15 lakh short.

Step 3: Calculate Inflation-Adjusted Corpus Targets for Each Goal

With your goals listed and the correct inflation rate applied, calculate what each goal actually costs in future rupees:

Formula: Future Value = Present Cost × (1 + Inflation Rate)^Years

Example: Child’s education today costs ₹30 lakh. At 10% education inflation for 15 years:

₹30 lakh × (1.10)^15 = ₹30 lakh × 4.177 = ₹1.25 crore — more than four times the present cost.

If you planned for ₹30 lakh, you are planning to fund roughly 24% of the actual requirement.

Step 4: Work Backwards to the Required Monthly SIP

For each goal, use the reverse SIP calculator to find the monthly investment needed:

Formula: Monthly SIP = [FV × r] / [((1 + r)^n − 1) × (1 + r)]

Where:

- FV = Future Value (inflation-adjusted corpus target)

- r = Monthly expected return rate (Annual rate ÷ 12)

- n = Number of months

For step-up SIPs, the formula is more complex — this is where digital tools become essential. The SIP Allocation Optimizer handles this calculation automatically, adjusting for step-up percentages and providing the starting SIP amount needed.

Step 5: Validate Against Your Monthly Surplus

Add up all the required SIPs from Step 4. Compare to your actual monthly investible surplus. If the total required SIP exceeds your surplus:

Option A: Increase step-up percentage. A 12% annual step-up instead of 10% significantly reduces the starting SIP requirement. The difference compounds over 20 years.

Option B: Extend goal timelines where flexible. A house purchase delayed by 3 years dramatically reduces the monthly SIP needed because both the accumulation timeline lengthens and the glide path to safe instruments reduces volatility risk.

Option C: Revisit corpus targets. Not all lifestyle assumptions are fixed. A retirement plan targeting ₹2 lakh/month at 60 may be achievable at ₹1.6 lakh/month with specific expense planning. This is the difference between Lean FIRE and Fat FIRE — and both are valid depending on your priorities.

Option D: Use the Waterfall Model. Prioritise goals by urgency and irreversibility. Emergency fund first. Child education next (smallest window for compounding). Retirement last (longest runway). As income grows, cascade the surplus down to lower-priority goals.

Step 6: Set Up the Actual SIPs and Review Annually

Calculation without implementation is zero. Once the numbers are validated:

- Set up separate SIP mandates for each goal with the correct fund

- Enable automatic annual step-up (top-up SIP) from Day 1

- Block a recurring date (first day of each financial year) for annual review

- At each review: check actual vs. projected corpus, rebalance if allocation has drifted, and verify that the remaining SIP contribution is still on track to hit the inflation-adjusted target

The Financial Freedom Calculator and the Portfolio Allocation Calculator together form an annual review toolkit — giving you a snapshot of where you stand relative to every goal, every year.

The Compounding Tables That Will Change How You Think About SIP Timing

One of the most powerful features of a good SIP portfolio calculator is compounding projection tables. Here are the ones worth bookmarking:

The Cost of a 5-Year Delay (₹10,000/month, 12% CAGR)

| Start Age | Retirement Age | Final Corpus | Lost by Waiting |

|---|---|---|---|

| 25 | 60 | ₹6.74 crore | — |

| 30 | 60 | ₹3.53 crore | ₹3.21 crore |

| 35 | 60 | ₹1.89 crore | ₹4.85 crore |

| 40 | 60 | ₹98.9 lakh | ₹5.75 crore |

| 45 | 60 | ₹49.9 lakh | ₹6.24 crore |

A 5-year delay at age 25 costs ₹3.21 crore. A 5-year delay at age 40 costs ₹49 lakh. The earlier the delay, the more catastrophic — because early years have the longest compounding runway.

This is the data that should make every 28-year-old Indian professional stop postponing their SIP by another “one more year.”

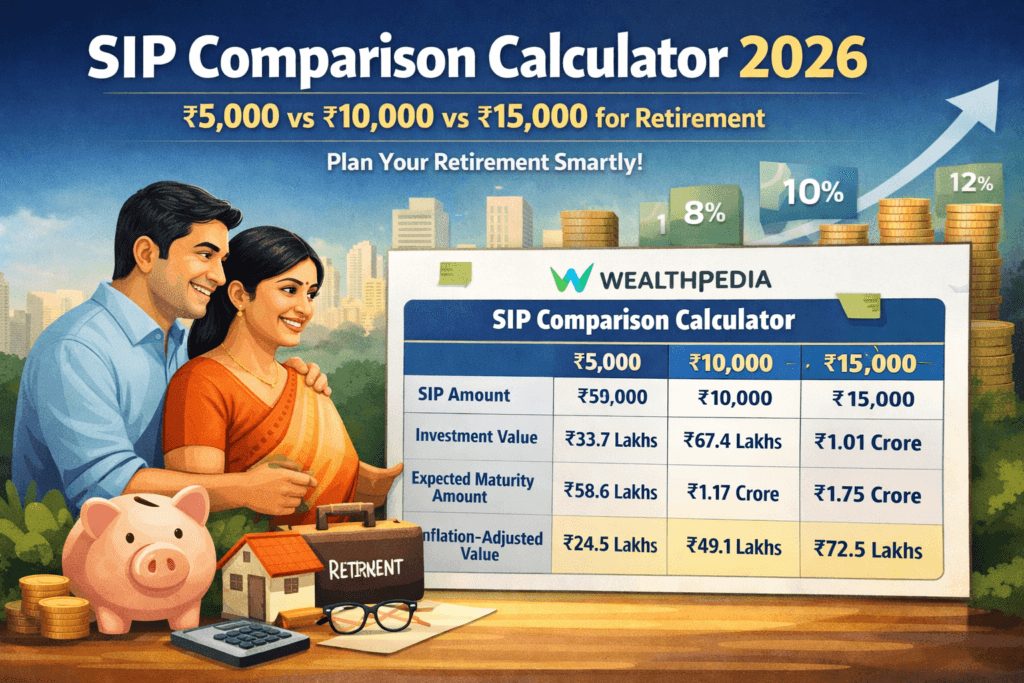

What ₹5,000, ₹10,000, and ₹15,000 SIPs Actually Build (12% CAGR, 25 Years)

| Monthly SIP | Flat 10% | Step-Up 10% | Step-Up 15% |

|---|---|---|---|

| ₹5,000 | ₹94.9 lakh | ₹1.89 crore | ₹2.84 crore |

| ₹10,000 | ₹1.89 crore | ₹3.79 crore | ₹5.68 crore |

| ₹15,000 | ₹2.84 crore | ₹5.68 crore | ₹8.52 crore |

The ₹5K vs ₹10K vs ₹15K SIP analysis on Wealthpedia goes deeper into what each of these amounts builds toward specific retirement scenarios — including whether ₹5,000/month is enough to reach the FIRE number for a 25-year-old with a 30-year horizon (spoiler: with step-up, it is, for many scenarios).

Inflation-Adjusted Real Value of SIP Corpus (6% Inflation)

| Nominal Corpus | Years from Now | Real Value (Today’s ₹) |

|---|---|---|

| ₹50 lakh | 10 | ₹27.9 lakh |

| ₹50 lakh | 20 | ₹15.6 lakh |

| ₹1 crore | 15 | ₹41.7 lakh |

| ₹2 crore | 20 | ₹62.4 lakh |

| ₹3 crore | 25 | ₹69.8 lakh |

| ₹5 crore | 25 | ₹1.16 crore |

This table is the most sobering. The ₹3 crore corpus you project for retirement in 25 years buys the equivalent of ₹69.8 lakh in today’s purchasing power. For a household spending ₹60,000/month today, that is less than 10 years of expenses — not the comfortable 30-year retirement they imagined.

SIP Calculator vs. SIP Portfolio Calculator: A Side-by-Side Comparison

Feature Basic SIP Calculator SIP Portfolio Calculator Direction of calculation Forward (input → corpus) Backward (goal → required SIP) Number of goals supported 1 Multiple simultaneously Inflation adjustment Usually no Yes, goal-specific rates Step-up SIP support Rarely Yes, with optimisation Goal-timeline alignment No Yes Surplus vs. required SIP comparison No Yes Retirement sustainability check No Yes (SWR integration) Rebalancing guidance No Yes Output One number Full financial roadmap

The Multi-Goal FIRE Planner and the SIP Comparison Calculator together replicate the functionality of a professional SIP portfolio calculator — at no cost, with Indian-specific benchmarks and tax treatment.

The Asset Allocation Dimension: Why Your SIP Calculator Must Know What You Are Investing In

A SIP portfolio calculator that assumes 12% CAGR uniformly across all goals is giving you false precision. The return rate changes based on what you are actually investing in — and what you are investing in must change based on your goal timeline.

Here is how asset allocation interacts with SIP calculator inputs:

Goal horizon under 3 years: SIP into liquid funds, short-duration debt, or conservative hybrid funds. Expected return: 7–8%. Using 12% here will dramatically overstate the final corpus.

Goal horizon 3–7 years: SIP into balanced advantage funds, aggressive hybrid funds, or large-cap index + short-duration debt split. Expected return: 9–11%.

Goal horizon 7–15 years: SIP into Nifty 50 + Nifty Next 50 + mid-cap index. Expected return: 11–13%.

Goal horizon 15+ years (FIRE): SIP into diversified equity index portfolio (Nifty 50 + Nifty Next 50 + international). Expected return: 12–14%.

When you enter a blended return assumption into a SIP portfolio calculator, you implicitly encode your asset allocation. Getting this right is not optional — it is the difference between planning with real constraints and planning with fictional numbers.

The Asset Allocation FIRE guide walks through exactly how to set the return assumption for each goal tier based on the appropriate fund mix — including how the allocation shifts as goals approach (the glide path).

Common SIP Calculator Errors and How to Fix Them

Error 1: Using Past Returns as Future Return Assumptions

The Nifty 500 returned 97% in 1999 and 91% in 2003. No SIP calculator should use these as future return assumptions. The appropriate planning return for a Nifty 50 index fund is 10–12% — the long-run post-cost CAGR adjusted for realistic averaging.

Fix: Use conservative scenario (10%), base scenario (12%), and optimistic scenario (14%) and plan to be sufficient at 10%.

Error 2: Ignoring the Post-Retirement Phase

Most SIP calculators stop at accumulation. They tell you what you will build, not whether it lasts. A 30-year retirement starting at age 55 is as long as most people’s entire working careers. The corpus must survive sequence-of-returns risk, healthcare cost escalation, and sustained inflation — none of which a simple future value formula captures.

The Safe Withdrawal Rate Calculator and Retirement Withdrawal SWP Calculator pick up where the SIP corpus calculator ends — modelling whether the corpus sustains 25, 30, or 35 years of withdrawals under various return and inflation scenarios.

Error 3: Treating EPF/PPF as “Already Handled”

Many Indian salaried investors mentally exclude EPF from their SIP portfolio planning because “it is automatic.” This is an expensive error of omission.

EPF at 8.25% EEE on a salary of ₹80,000/month (both employer and employee contributions combined: ₹9,600/month) accumulates to approximately ₹95.4 lakh in 25 years at 8.25% — more than many investors’ entire planned SIP corpus.

Including EPF and PPF in your SIP portfolio calculator reduces the required equity SIP meaningfully — and prevents over-investment that constrains current lifestyle unnecessarily.

Error 4: Not Accounting for Tax on Withdrawals

Long-term capital gains (LTCG) on equity mutual funds above ₹1.25 lakh/year are taxed at 12.5% from 2024 onwards. For large retirement corpora, the annual LTCG liability can be significant. A SIP portfolio calculator that ignores post-withdrawal tax will overstate the net corpus available for spending.

Ballpark adjustment: For equity mutual fund SIPs, reduce the effective post-tax CAGR by approximately 0.5–0.8% to account for annual LTCG on portfolio rebalancing and withdrawal. For PPF (EEE) and EPF (EEE), no adjustment needed.

Error 5: Single Lump-Sum Goal, No Ongoing Income Planning

Many Indians plan for a corpus target (₹2 crore, ₹5 crore) without modelling what that corpus generates monthly. A ₹2 crore corpus at a 4% SWR generates ₹6.67 lakh/year or ₹55,556/month. At a 3.5% SWR (more appropriate for 30-year horizons), it generates ₹5.83 lakh/year or ₹48,611/month.

If you need ₹1 lakh/month in retirement, ₹2 crore is not enough — even though it “sounds like a lot.” The Retirement Corpus Calculator and the retirement planning guide both address this confusion directly, connecting the corpus number to the actual monthly income it sustains.

The SIP Portfolio Calculator for Special Situations

For FIRE Aspirants (Target: Retire Before 50)

FIRE planning in India requires a more aggressive SIP calculator framework:

- Accumulation phase is shorter (20–25 years vs 35 years for traditional retirement)

- Withdrawal phase is longer (40–50 years vs 25 years)

- Required corpus is therefore much larger relative to income

- Sequence-of-returns risk is amplified because you retire before most market cycles complete

The key calculation difference: use a 3–3.5% SWR (not 4%) for FIRE planning in India due to longer withdrawal horizons and higher Indian inflation. This means you need 28–33x annual expenses as your corpus — not the 25x that Western 4% SWR advocates suggest.

For someone spending ₹60,000/month (₹7.2 lakh/year), the FIRE corpus at 3.5% SWR = ₹7.2 lakh ÷ 0.035 = ₹2.06 crore in today’s rupees — but this must be inflation-adjusted to the retirement year. If retirement is 20 years away at 6% inflation, the required corpus in 2046 rupees is ₹2.06 crore × 3.207 = ₹6.61 crore.

This is the real FIRE number — not ₹2 crore. Use the FIRE Number Calculator to run this calculation for your specific situation.

For NRIs Planning India Retirement

NRIs face an additional complexity: currency risk. An NRI earning in USD who plans to retire in India must account for INR/USD exchange rate movements over their accumulation horizon.

The historical trend: INR has depreciated approximately 4–5% annually against USD over the past 30 years. For an NRI with USD income investing in Indian mutual funds, the effective returns are the Indian fund return minus the USD appreciation — not a simple addition of returns.

The appropriate framework for NRIs: maintain a portion of the retirement corpus in global (USD-denominated) assets and a portion in Indian equity — balancing currency risk with the India-specific growth premium.

For Late Starters (Starting Investment at 40+)

The most common question on personal finance forums: “I am 42 with no investments. Is it too late?”

It is not too late. But the SIP portfolio calculator will be honest with you about the constraints.

As shown in the Vikram scenario, a 45-year-old starting with zero investments can still build a meaningful corpus by 60 — but it requires:

- Higher savings rates (30–40% of income)

- More aggressive step-ups (15% annual)

- Maximising tax-advantaged instruments (VPF, NPS 80CCD(1B))

- Potentially a retirement at 62–65 instead of 55

The Barista FIRE model — where you partially retire with supplemental income — is often the most practical path for late starters: build a corpus sufficient to reduce full-time work by age 55, with passive income covering 50–60% of expenses while part-time work covers the rest.

Building Your SIP Portfolio Calculator Dashboard: A Practical Setup

Here is a practical way to use the tools available to build your own ongoing SIP portfolio tracking system:

Monthly snapshot (5 minutes):

- Check that all SIP debits have processed

- Log any top-ups or additional lump sum investments

Quarterly snapshot (30 minutes):

- Check actual corpus vs. projected corpus for each goal using your original projections

- If any goal’s actual corpus is more than 10% below projection, investigate (fund underperformance, SIP missed, market correction)

Annual review (2–3 hours, on April 1 or January 1):

- Run the Financial Health Score — this gives a structured 7-pillar assessment across emergency preparedness, insurance, debt management, investment rate, goal alignment, tax efficiency, and net worth trajectory

- Update inflation assumptions if CPI has meaningfully shifted

- Update goal costs with the latest information (new college fee structures, property price changes)

- Rebalance: if equity has significantly outperformed and is now overweight vs. target allocation, redirect new SIP contributions to debt until allocation normalises

- Implement the annual SIP step-up

- Check if your financial health score has improved from the previous year

Conclusion: The Calculator You Use Determines the Plan You Build

In a country where 9 crore SIP accounts collectively invest ₹29,000+ crore every month, the quality of the planning tool being used matters at a national scale.

A basic SIP calculator produces a large number and a false sense of security.

A SIP portfolio calculator produces a financial roadmap — with goal-specific corpus targets, inflation-adjusted requirements, step-up SIP projections, and a clear answer to the only question that actually matters: Am I on track?

The difference between the two is not sophistication for its own sake. It is the difference between discovering a ₹1 crore shortfall at age 28, when you have 25 years to fix it — versus discovering it at 52, when you have 8 years.

Use the SIP Comparison Calculator to model multiple scenarios side by side. Use the Multi-Goal FIRE Planner to model all your goals simultaneously. Use the SIP Allocation Optimizer to find the right monthly amount for each goal with step-up built in.

Build the plan with the right numbers. Then the only remaining task — the one that actually separates the investors who achieve FIRE from those who don’t — is execution.

Start. Stay in. Step up. Review annually. That is the entire playbook.

Frequently Asked Questions: SIP Portfolio Calculator

What is a SIP portfolio calculator and how does it differ from a basic SIP calculator?

A basic SIP calculator computes how much a fixed monthly investment grows to over time at an assumed return. A SIP portfolio calculator works in reverse — it starts from your financial goals, applies inflation to calculate the real corpus required, and tells you the exact monthly SIP needed today. It also supports multiple goals simultaneously and accounts for step-up SIPs, asset allocation, and goal-specific timelines.

What return rate should I use in a SIP portfolio calculator in India?

For long-term equity SIPs (15+ years): use 10–12% CAGR for conservative/base scenarios. For blended equity-debt portfolios: 9–10%. For debt-only instruments: 7–8%. Never use recent 3-year returns as your planning assumption — India’s equity markets have delivered 15%+ in some years and −56% in others. Plan conservatively and let outperformance be a bonus.

How does inflation affect my SIP calculation?

Inflation makes your corpus target larger and your SIP output smaller in real terms. A ₹1 crore corpus accumulated in 20 years has the purchasing power of approximately ₹31 lakh in today’s money at 6% inflation. Use the SIP Calculator with Inflation to see both nominal and inflation-adjusted outputs side by side.

What is the correct inflation rate to use for a child’s education SIP calculator?

Education inflation in India runs at 10–12% annually — significantly higher than general CPI. A private engineering seat costing ₹15 lakh today costs approximately ₹62.6 lakh in 15 years at 10% education inflation. Always use category-specific inflation rates for education and healthcare goals, not general CPI.

Can a SIP portfolio calculator tell me if I will run out of money in retirement?

Yes — when integrated with a safe withdrawal rate (SWR) calculator. The SIP portfolio calculator shows corpus accumulation; the SWR calculator models corpus depletion over a 25–35 year retirement under various return and inflation scenarios. Use both together: the Retirement Corpus Calculator for accumulation and the Retirement Withdrawal SWP Calculator for sustainability.

How do I calculate the SIP needed to reach ₹1 crore?

The required SIP depends on your timeline and return assumption. At 12% CAGR: 10 years needs ₹43,000/month, 15 years needs ₹19,800/month, 20 years needs ₹10,100/month, 25 years needs ₹5,320/month, 30 years needs ₹2,860/month. The 5-year delay from starting at 25 vs. 30 more than doubles the required monthly SIP for the same ₹1 crore target.

Should I include EPF in my SIP portfolio calculator inputs?

Absolutely. EPF at 8.25% EEE is one of India’s best guaranteed returns. At a combined employee + employer contribution of ₹9,600/month on a ₹80,000/month salary, EPF alone builds approximately ₹95 lakh over 25 years. Including this reduces your required equity SIP meaningfully and prevents over-investment that unnecessarily constrains current lifestyle.

What is a step-up SIP and how does it change the calculator output?

A step-up (or top-up) SIP automatically increases your monthly investment by a fixed percentage each year. At a 10% annual step-up, a ₹10,000/month starting SIP over 25 years at 12% CAGR builds ₹3.79 crore — versus ₹1.89 crore for the same SIP held flat. The step-up effectively doubles the corpus on a modest additional total contribution. It is the highest-leverage SIP decision you can make.

How many goals can I plan simultaneously with a SIP portfolio calculator?

The Multi-Goal FIRE Planner supports multiple simultaneous goals. In practice, most Indian families have 3–5 active goals: emergency fund (ongoing), child education, house (near-term), retirement (long-term), and optionally healthcare corpus. Each goal gets its own calculator inputs, fund allocation, and SIP amount — they do not share a calculation.

What is the formula used in a SIP calculator?

The standard SIP future value formula is: FV = P × [((1 + r)^n − 1) / r] × (1 + r), where P = monthly SIP amount, r = monthly return rate (annual rate ÷ 12), n = number of months. For step-up SIPs the formula is significantly more complex — requiring iterative calculation, which is why digital tools are essential.

How accurate are SIP calculator projections?

SIP calculators are planning tools, not guarantees. Actual returns vary based on market performance, fund selection, and timing. A projection at 12% CAGR is a reasonable planning assumption — actual 20-year equity returns in India have ranged from 8% to 18% depending on the specific 20-year window. The value of a SIP calculator is not precision prediction but structured planning — knowing the required SIP and tracking whether you are on course.

What is the minimum SIP amount that makes sense to invest?

Even ₹500/month has mathematical value, but ₹1,000–₹2,000/month is a more practical minimum to see meaningful compounding. More importantly, any amount started today is better than a larger amount started 2 years from now. A ₹1,000 SIP with a 15% annual step-up for 25 years at 12% CAGR builds ₹56.8 lakh. The same ₹1,000 started 5 years later builds ₹25.3 lakh — a ₹31.5 lakh difference.

Should I use a SIP calculator for debt mutual fund investments?

Yes, but use a lower return assumption (7–8% for short-duration funds, 7.5–8.5% for medium-duration funds). Debt SIPs are appropriate for near-term goals (1–5 years) where capital preservation matters more than return maximisation. Do not apply equity return assumptions to debt fund SIP projections.

How does the SIP calculator handle market crashes?

Standard SIP calculators use a constant return assumption and do not model market crashes. The actual impact of crashes depends on when they occur — crashes during accumulation are buying opportunities (you buy more units at lower prices), while crashes at retirement are catastrophic due to sequence-of-returns risk. For retirement planning, stress-test your corpus through the sequence of returns risk guide to understand whether your FIRE plan survives a 2008-style crash in Year 1 of retirement.

What is a realistic monthly income from a ₹2 crore retirement corpus?

At a 4% safe withdrawal rate: ₹8 lakh/year = ₹66,667/month. At a 3.5% SWR (more appropriate for 30+ year retirements): ₹7 lakh/year = ₹58,333/month. These are gross figures — post LTCG tax on equity withdrawals, the net is approximately 5–8% lower. Whether ₹2 crore is enough depends entirely on your expense level and retirement duration. See the detailed analysis in can I retire with ₹2 crore.

Does a SIP portfolio calculator account for tax?

Most basic ones do not. For accurate post-tax planning: equity mutual fund LTCG above ₹1.25 lakh/year is taxed at 12.5%; debt fund gains are taxed at your income tax slab; PPF and EPF are EEE (fully tax-exempt). Adjust your effective return assumptions downward by 0.5–1% for equity SIPs in the 20–30% tax bracket to account for eventual LTCG at withdrawal and annual rebalancing.

What is a SIP portfolio calculator useful for beyond retirement planning?

Beyond retirement, SIP portfolio calculators are used for: child’s education corpus planning, house down payment accumulation, vehicle purchase fund, wedding corpus, medical emergency fund building, business capital accumulation, and FIRE planning (all variants — Lean, Barista, Fat FIRE). Each goal requires a separate calculator run with goal-specific inputs.

How is the SIP calculator different for FIRE planning vs. traditional retirement?

FIRE planning requires: shorter accumulation phase (20–25 years vs. 30–35), longer withdrawal phase (35–45 years vs. 20–25), lower safe withdrawal rate (3–3.5% vs 4%), higher corpus target (28–33x annual expenses vs 25x), and more aggressive equity allocation during accumulation. The FIRE Number Calculator is calibrated for Indian FIRE scenarios specifically.

Should I use the same SIP calculator for both equity and PPF?

No. PPF has a guaranteed 7.1% return with no volatility, a 15-year lock-in, and EEE tax status. It should be modelled separately with its guaranteed rate. The PPF Calculator at Wealthpedia handles PPF-specific calculations including the 15-year maturity, 5-year extension cycles, and partial withdrawal rules — which a standard SIP calculator cannot model.

What happens to my SIP calculator projection if I miss a few months?

Missing a few months has a smaller impact than most investors fear in the early years, and a larger impact than they expect in the final years. Missing 3 months in Year 1 of a 25-year SIP costs approximately ₹1.8 lakh in final corpus (at ₹10,000/month, 12% CAGR). Missing 3 months in Year 23 costs approximately ₹35,000. Never stop a SIP — pause if absolutely necessary, then restart immediately.

How do I use a SIP calculator to check if I am on track?

Run the reverse calculation: for your current corpus + remaining SIP at the original assumed return, does the projected corpus at the goal date still meet the inflation-adjusted target? If yes, you are on track. If the projected corpus is 10% or more below target, you need to either increase the SIP, extend the timeline, or reduce the corpus target. The Financial Health Score gives a structured annual tracking framework for all goals simultaneously.

Can a SIP calculator help me plan for healthcare costs in retirement?

With the right inputs, yes. Use healthcare-specific inflation (12–15%) to calculate the future healthcare corpus required, then reverse-calculate the required SIP. A separate ₹3–5 lakh liquid fund (not equity SIP) should be maintained for immediate medical needs, while the larger healthcare corpus can be in a conservative hybrid fund SIP. The healthcare inflation FIRE guide explains why healthcare planning is the most critical — and most underplanned — component of any Indian retirement strategy.

What is the difference between a SIP calculator and a lump sum calculator?

A SIP calculator models regular periodic investments (monthly). A lump sum calculator models a one-time investment. Use the SIP calculator for regular salary-linked investments, and the lump sum calculator for windfall events (bonus, inheritance, property sale proceeds). A Systematic Transfer Plan (STP) — parking lump sum in liquid fund and transferring monthly to equity — combines both: the lump sum goes in at once, but equity exposure is taken on gradually, similar to a SIP.

How do I calculate how much SIP I need for a ₹50,000/month retirement income?

Step 1: Decide your retirement year and apply 6% inflation to find the future equivalent of ₹50,000. For 20 years: ₹1,60,357/month. Step 2: Calculate the corpus required at 3.5% SWR: ₹1,60,357 × 12 ÷ 0.035 = ₹5.50 crore. Step 3: Find the required SIP to accumulate ₹5.50 crore in 20 years at 12% CAGR = approximately ₹55,600/month flat, or ₹22,000/month with 12% annual step-up.

What is the most common mistake people make with SIP calculators in India?

Planning in nominal terms without inflation adjustment. A ₹1 crore target feels large today. In 20 years at 6% inflation, it has the purchasing power of ₹31.2 lakh — less than 3 years of current expenses for a middle-class Indian family. Set all targets in today’s rupees, apply inflation to calculate the future corpus required, and then reverse-calculate the SIP needed. Every other SIP calculator error — wrong return assumption, missing step-up, fund overlap — pales beside this one fundamental mistake.

Disclaimer: All figures and projections are illustrative calculations for planning purposes. Actual mutual fund returns depend on market performance, fund selection, and macro conditions. Past performance is not indicative of future returns. This article is for educational purposes only. Wealthpedia is not a SEBI-registered investment advisor. Please consult a qualified financial advisor before making investment decisions. Wealthpedia® is a registered trademark (TM No. 4910385).

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up