Most Indians invest in SIPs the same way they order from a new restaurant menu — randomly, based on what sounds good, hoping it works out. The best SIP allocation strategy is not about picking the hottest fund. It is about engineering a portfolio where every rupee has a job, every fund has a purpose, and every goal has its own runway.

The Problem Nobody Talks About

Here is a scene that plays out thousands of times every month across India.

Someone reads that SIPs are the best way to build wealth. They open a Zerodha or Groww account, search “best mutual fund 2026,” pick three or four funds that appeared in a popular article, and set up SIPs. Done. Portfolio built.

Three years later, they look at their portfolio and find overlapping funds holding the same 40 stocks, no clear allocation between large-cap and mid-cap, no debt component, no gold exposure, and no connection whatsoever between the portfolio and the actual financial goals they were trying to achieve.

This is not bad luck. It is the predictable outcome of a portfolio built on vibes rather than strategy.

The best SIP allocation strategy is not about finding the highest-returning fund — we covered in our 30-year asset class analysis that no single asset class wins consistently year after year. The best SIP allocation is about engineering a portfolio where each goal has a dedicated allocation, each allocation is matched to a timeline, and the whole structure is robust enough to survive market crashes without you making panic decisions.

This article gives you that engineering framework. Start to finish.

Why Most SIP Portfolios Are Built Wrong

Before building the right framework, it is important to understand exactly what goes wrong with most Indian SIP portfolios.

Mistake 1: One Portfolio for Everything

The most fundamental error. You have a ₹15,000/month SIP going into a Nifty 50 index fund. You call it your “investment.” But what is it for? Emergency fund? Child’s education? Retirement? A house down payment?

When everything goes into one bucket, you create an impossible conflict. Your retirement corpus (which needs 20+ years of equity compounding) is sitting next to your house down payment corpus (which needs capital preservation in 3 years). When the market falls 30%, you face a paralysing choice: do you hold for the long-term retirement goal, or do you withdraw what remains for the house?

Goal-based investing solves this by separating each financial objective into its own dedicated SIP with its own fund selection, its own timeline, and its own risk profile. We have built the Wealthpedia Multi Goal FIRE Planner specifically to model this multi-goal approach — because a single retirement calculator cannot capture the complexity of real Indian financial life.

Mistake 2: Confusing Diversification with Over-Diversification

Many Indians think owning eight mutual funds means they are diversified. They own a Nifty 50 fund, a large-cap fund, a large and mid-cap fund, a flexicap fund, a focused fund, and a multi-cap fund. Virtually all of these funds hold the same 30–50 large-cap stocks with minor variations.

This is not diversification. This is redundancy. The actual diversification that matters — across asset classes (equity vs debt vs gold vs international), across market cap segments (large vs mid vs small), and across goal timelines — requires far fewer funds chosen with far more intention.

A properly structured SIP portfolio needs 4–6 funds maximum. Not 10–15.

Mistake 3: Ignoring Inflation in Return Assumptions

Understanding how inflation eats your SIP corpus is perhaps the most important — and most ignored — aspect of SIP planning. At 6% annual inflation:

- ₹50,000/month expenses today become ₹1,60,000/month in 20 years

- A ₹2 crore corpus that looks comfortable today generates the real purchasing power of roughly ₹62 lakh in today’s terms over a 20-year retirement at 6% drawdown

Your SIP projection showing ₹3 crore at 12% CAGR is not ₹3 crore in today’s purchasing power. It is approximately ₹93 lakh in today’s terms if inflation runs at 6% for 20 years. Most SIP calculators hide this reality. A good SIP allocation strategy accounts for inflation at every step — in the accumulation target, in the withdrawal planning, and in the fund selection itself.

Mistake 4: Step-Up SIPs Planned, Never Implemented

The most consistent finding from our SIP comparison analysis is the enormous gap between step-up and flat SIPs over long horizons. A ₹10,000/month flat SIP at 12% CAGR over 20 years builds ₹99.9 lakh. The same ₹10,000/month SIP with a 10% annual step-up builds ₹1.89 crore — almost double — with a similar total contribution.

Most Indians plan to step up their SIPs when they get their next salary hike. They never do. The best SIP allocation strategy hard-wires the step-up into the investment structure from Day 1, not as an aspiration but as an automatic instruction.

The Wealthpedia SIP Allocation Framework: The 4-Goal Architecture

The framework we use at Wealthpedia is built around a simple but powerful principle: every SIP must belong to a goal, and every goal must have its own allocation architecture.

We organise all Indian financial goals into four categories — each with a different time horizon, a different risk tolerance, and therefore a different optimal fund selection.

Goal Category 1: Emergency & Liquidity (0–1 Year Horizon)

This is not an investment goal. It is a protection goal.

Your emergency fund — whether 3 months or the updated 6–9 month standard that we recommend for Indian households — does not belong in equity mutual funds. It never did. Not even “just temporarily.”

Where it belongs:

- High-yield savings account (4–7%)

- Liquid mutual funds (6.5–7%)

- Overnight/ultra-short duration funds for the portion beyond immediate access needs

SIP for emergency fund: Set up a small automated monthly transfer to a liquid fund until you hit your target (typically 6 months of total household expenses). Once the target is hit, stop. The emergency fund does not grow like an investment — it is maintained at a fixed rupee target, adjusted annually for lifestyle inflation.

The critical rule: Never count your emergency fund as part of your investment portfolio. It is insurance, not wealth. Your financial health score depends significantly on having this fully funded and separated from investment assets.

Goal Category 2: Near-Term Goals (2–5 Year Horizon)

Near-term goals include house down payments, vehicle purchases, wedding expenses, or any other target you need to reach within 5 years.

The allocation reality: Near-term goals cannot afford equity’s volatility. The Nifty 500 fell 56% in 2008 and took 2+ years to recover. If you needed your down payment in 2010 and were 100% in equity, you were either waiting years or buying less house. That is the sequence risk of misaligning goals to instruments.

For 2–3 year goals:

| Instrument | Allocation | Rationale |

|---|---|---|

| Short Duration Debt Fund | 60–70% | Stable 7–7.5% with liquidity |

| Conservative Hybrid Fund | 20–30% | Modest equity upside with debt anchor |

| Arbitrage Fund | 10–20% | Equity taxation, near-FD returns |

For 3–5 year goals:

| Instrument | Allocation | Rationale |

|---|---|---|

| Conservative Hybrid Fund | 40–50% | Automatic rebalancing, stability |

| Equity Index Fund (Nifty 50) | 30–40% | Growth component as horizon lengthens |

| Short Duration Debt Fund | 20–30% | Capital preservation anchor |

For a detailed breakdown of how to build a SIP for a specific near-term target like a house down payment, the approach changes significantly based on property cost, target date, and existing savings — which is why goal-specific calculators matter more than generic allocation guides.

The glide path rule for near-term goals: Begin shifting from equity to debt 18 months before the goal date. By 6 months before the target, the allocation should be 80–90% in liquid/short-duration instruments. The goal is capital preservation at this stage, not return maximisation.

Goal Category 3: Medium-Term Goals (5–15 Year Horizon)

This is the most common category for Indian middle-class investors: child’s higher education, home upgrade, or a mid-career sabbatical fund. These goals are far enough away that equity makes sense, but close enough that you cannot ignore the downside.

The most important medium-term goal in India: Child’s Education

At current costs, a 4-year engineering or MBA programme at a private institution costs ₹15–40 lakh. At 8% education inflation, that same programme costs ₹32–86 lakh in 15 years. A child born today will need their education corpus funded in approximately 17–18 years — starting from Day 1 of their life.

As we showed in our detailed monthly SIP for child’s education guide, the SIP required to reach a ₹40 lakh education corpus in 15 years (assuming 12% CAGR):

- Starting SIP: ₹9,200/month

- With 10% annual step-up: ₹5,800/month starting SIP

The difference between starting at birth vs waiting until the child is 5 years old: an additional ₹3,800/month in required SIP — the cost of 5 years of procrastination.

Allocation for 10–15 Year Goals:

| Instrument | Allocation | Why |

|---|---|---|

| Nifty 50 Index Fund | 40% | Large-cap stability, low cost |

| Nifty Next 50 Index Fund | 20% | Growth premium over large-cap |

| Mid-Cap Index Fund | 15% | Long-horizon growth without active fund risk |

| Short Duration Debt Fund | 15% | Stability anchor and glide path destination |

| International Index Fund | 10% | Geographic diversification, USD exposure |

Allocation for 5–10 Year Goals:

| Instrument | Allocation | Why |

|---|---|---|

| Nifty 50 Index Fund | 45% | Core large-cap exposure |

| Conservative Hybrid Fund | 30% | Auto-rebalancing within a single fund |

| Short Duration Debt Fund | 25% | Higher stability as horizon is shorter |

The glide path for medium-term goals: 5 years before the goal, begin monthly rebalancing from equity to debt — shifting approximately 2–3% from equity to debt every 6 months. By the time the goal arrives, the allocation should be 80–90% in stable instruments.

This is exactly the discipline that protects a child’s education SIP from a market crash in year 14 of a 15-year plan — arguably the most common and most painful planning failure for Indian parents.

Goal Category 4: Long-Term / FIRE Goals (15+ Year Horizon)

This is where the real wealth is built. And where most Indians are dramatically under-allocated to equity.

For goals 15+ years away — primarily retirement and financial independence — time is the most powerful force in investing. A ₹10,000/month SIP at 12% CAGR over 25 years builds ₹1.89 crore. The same SIP at 10% CAGR over the same period builds ₹1.33 crore. That 2% return difference — typically the gap between an actively managed large-cap fund and a low-cost Nifty 50 index fund — costs ₹56 lakh over 25 years. This is why fund selection and cost matter enormously over long horizons.

The long-term FIRE SIP allocation:

| Instrument | Allocation | Role |

|---|---|---|

| Nifty 50 Index Fund | 35% | Core large-cap. Low cost. Bedrock holding. |

| Nifty Next 50 Index Fund | 20% | The historical return engine of Indian equity |

| Mid-Cap Index Fund | 15% | Long-horizon growth with higher volatility |

| International Index Fund (S&P 500 / Global) | 15% | USD hedge, sector diversification |

| PPF / EPF | 10% | Tax-free guaranteed debt, EEE status |

| Sovereign Gold Bond | 5% | Inflation hedge, LTCG-exempt at maturity |

This is our recommended long-term FIRE allocation for investors in their 20s and 30s — those with 15–30 years to their financial independence target.

We have written in detail about the full FIRE planning framework for Indians — this SIP allocation is the accumulation engine that feeds the FIRE corpus.

The Waterfall SIP Model: How to Prioritise When Money Is Limited

Most Indians cannot fund all four goal categories simultaneously from day one. The question is: which goal gets funded first?

The answer depends on urgency, irreversibility, and compounding impact. We call this the Waterfall Model — money flows down from the most critical to the next, like water over rocks.

Level 1 — Emergency Fund (Always First)

Before any investment SIP, build 3 months of expenses in a liquid fund. Without this, any market event or job disruption forces you to break long-term investments at exactly the wrong time. We have written about why even the standard 3-month emergency fund is now outdated for Indian households — targeting 6 months minimum.

Level 2 — EPF/PPF (Never Skip the Mandatory + Tax-Exempt)

Maximise EPF (it is automatic) and contribute ₹1.5 lakh/year to PPF if in a 20–30% tax bracket. The EEE status makes PPF India’s best risk-free return instrument. You are effectively getting 7.1% guaranteed, tax-free — which on an after-tax basis beats most debt instruments available to retail investors.

Level 3 — Child Education SIP (Starts Earlier = Needs Less)

If you have children under 10, the education SIP is the highest-priority medium-term goal because compounding time is finite. A ₹5,000/month SIP started at birth versus at age 8 creates a ₹15–20 lakh difference in corpus at college age. Every year of delay has a hard cost.

Level 4 — Retirement/FIRE SIP (The Compounder)

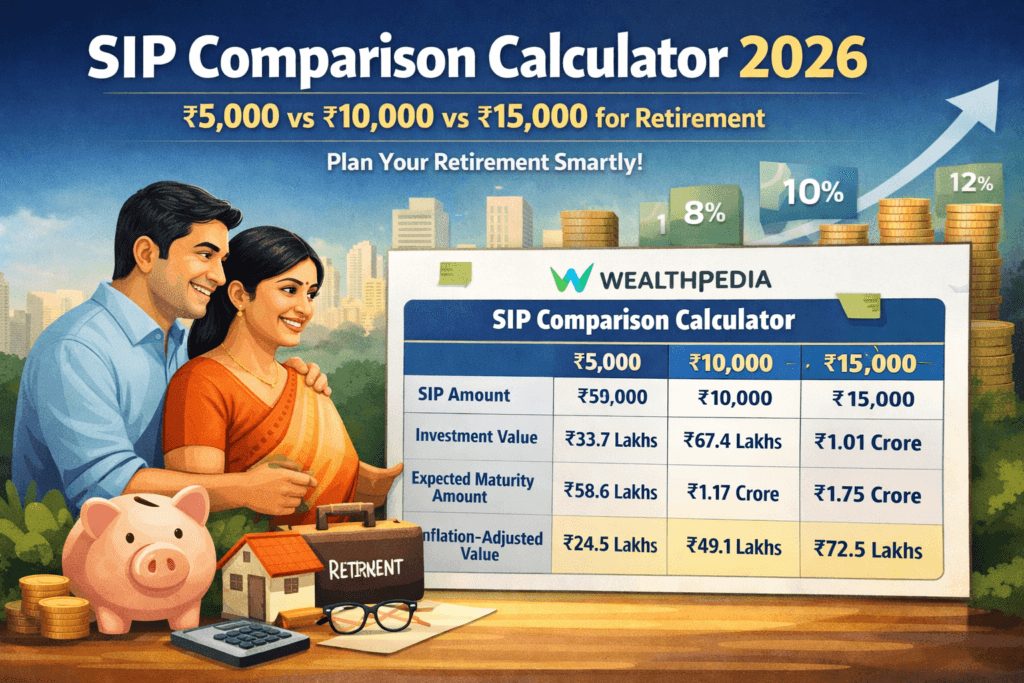

The longest-horizon goal has the longest compounding runway. As demonstrated in our ₹5K vs ₹10K vs ₹15K SIP comparison, even ₹5,000/month started at 25 becomes a meaningful retirement corpus by 55. The key is starting — not starting large.

Level 5 — Near-Term Goals (House, Vehicle)

These goals are funded last in the waterfall because they are flexible (you can delay a house purchase, not a child’s college) and because they have shorter horizons that require lower-return instruments anyway.

The Waterfall SIP Allocation approach is one of the most effective frameworks for Indian families managing multiple simultaneous goals on a limited monthly surplus.

The Step-Up SIP: The Single Most Powerful Move in Your Allocation Playbook

If there is one SIP strategy that produces disproportionate long-term results, it is the step-up SIP — and yet fewer than 20% of Indian SIP investors actually implement it.

The mathematics are unambiguous:

Flat SIP vs 10% Annual Step-Up SIP (12% CAGR, 25 Years)

| Monthly SIP | Structure | Total Investment | Final Corpus |

|---|---|---|---|

| ₹5,000 | Flat | ₹15,00,000 | ₹94.9 Lakhs |

| ₹5,000 | 10% Step-Up | ₹19,85,000 | ₹1.89 Crores |

| ₹10,000 | Flat | ₹30,00,000 | ₹1.89 Crores |

| ₹10,000 | 10% Step-Up | ₹39,70,000 | ₹3.79 Crores |

| ₹15,000 | Flat | ₹45,00,000 | ₹2.84 Crores |

| ₹15,000 | 10% Step-Up | ₹59,56,000 | ₹5.68 Crores |

The step-up SIP starting at ₹5,000/month produces the same corpus as a flat ₹10,000/month SIP — at roughly half the early-year cash outflow. This matters enormously for young investors who have limited current income but rapidly growing earnings ahead.

How to implement the step-up:

Most AMCs (Mutual fund platforms) support “Step-up SIP” or “Top-up SIP” instructions — you set the base SIP amount, the step-up percentage (10% recommended), and the step-up frequency (annual recommended). It is a one-time instruction that eliminates the need for annual manual increases.

If your platform does not support automated step-up, set a calendar reminder on April 1st every year to manually increase each SIP by 10%. It takes 10 minutes annually. Over 25 years, those 250 minutes of total effort are worth ₹95 lakh in additional corpus.

Our best SIP strategy for retirement 2026 guide walks through the exact step-up implementation across different platforms and income levels.

SIP Allocation by Age: The Decade-Wise Blueprint

The right allocation does not stay constant. It evolves — both in amount (as income grows) and in composition (as goals approach).

In Your 20s: The Foundation Decade

Your 20s are the highest-leverage decade in your financial life. Not because you earn the most — you probably earn the least. But because compounding time is at its maximum. A ₹5,000 SIP at 24 has 31 years to compound to retirement at 55. That same ₹5,000 at 34 has only 21 years — it will produce less than half the final corpus despite the same investment.

Priority in your 20s:

- Emergency fund: ₹3–5 lakh in liquid fund

- PPF: Max ₹1.5 lakh/year contribution

- Long-term equity SIP: ₹5,000–₹15,000/month in 3-fund index portfolio

Recommended 20s SIP portfolio (₹10,000/month total): Fund Allocation Monthly Amount Nifty 50 Index Fund 50% ₹5,000 Nifty Next 50 Index Fund 30% ₹3,000 International Index Fund 20% ₹2,000

Simple. Low-cost. No debt needed beyond mandatory EPF. Your financial health score in your 20s is more about savings rate and emergency preparedness than about sophisticated fund selection.

In Your 30s: The Expansion Decade

Your 30s bring higher income, more goals (children, home), and growing complexity. This is when the single-portfolio error becomes most costly — because you now have multiple goals with very different timelines.

Additional SIPs launched in your 30s:

- Child education SIP: 2-fund (Nifty 50 + Mid-Cap) with 15-year horizon

- House down payment SIP: Conservative hybrid + short duration debt

- Retirement SIP: Expanded from 20s portfolio, adding mid-cap and international

Total SIP targets in your 30s: 20–25% of gross income across all goals, implemented via the Waterfall Model.

The critical 30s discipline: do not raid the retirement SIP for near-term goals. If you need money for a car or vacation, use savings — not the retirement SIP. Breaking a long-term SIP for a short-term want is the most expensive financial decision most 35-year-olds ever make.

In Your 40s: The Acceleration Decade

Your 40s typically bring peak earning years, children’s education costs approaching, and FIRE becoming a realistic target rather than a distant dream. This is when the financial mistakes Indians make in their peak earning years become most costly — because there is more money to misallocate.

Key 40s allocation shifts:

- Increase the debt allocation within the retirement SIP (the bond tent begins)

- Begin building Bucket 1 (liquid fund) for FIRE corpus separately from SIPs

- Education SIP enters the glide path — begin shifting from equity to debt 5 years before college year

- Increase step-up SIP amounts aggressively — your 40s peak income years have the largest compounding impact remaining

If you are targeting FIRE at 50, your 40s are the “last chance to accelerate” window. As we explored in our FIRE at 40 guide, reaching FIRE in this decade requires 30–40% savings rates — which means the 40s SIP allocation must be both aggressive in size and strategically structured across goals.

In Your 50s: The Transition Decade

By your 50s, most near-term goals have been funded or completed. The allocation focus narrows entirely to retirement sustainability.

50s allocation priorities:

- Complete the bond tent: gradually reduce equity from 65% to 50–55%

- Fully fund Bucket 1 (₹15–25 lakh in liquid fund — 2 years of expected monthly expenses)

- Maximise PPF extension (if eligible)

- Begin SWP (Systematic Withdrawal Plan) planning — model sustainable withdrawal rates

Our Safe Withdrawal Rate calculator and retirement withdrawal SWP calculator are both built for this transition planning — helping you model what monthly income your corpus can sustainably generate without ever running out.

Fund Selection: The Right Instruments for Each Goal

The allocation architecture means nothing without the right funds. Here is the specific fund selection logic for each component of the portfolio.

For Equity: Index Funds Win Over Long Horizons

We take a clear position on this: for long-term goals (10+ years), passive index funds consistently outperform actively managed funds after accounting for costs and survivorship bias.

The evidence from Indian markets:

- Over 10 years, fewer than 15% of actively managed large-cap funds beat the Nifty 50 TRI after fees

- The average expense ratio of active large-cap funds: 1.5–2.0%. Nifty 50 index fund: 0.1–0.2%

- That 1.5–1.8% annual cost difference compounds to ₹22–28 lakh over 25 years on a ₹10,000/month SIP

Recommended index funds by category: Category Fund Type Why Large Cap Core Nifty 50 Index Fund Bedrock. Lowest cost. Most liquid. Large Cap Growth Nifty Next 50 Index Fund Historically 2–4% higher CAGR than Nifty 50 Mid Cap Nifty Midcap 150 Index Fund Mid-cap without active fund manager risk Small Cap Nifty Smallcap 250 Index (use sparingly) Only for 15+ year horizons, max 10% International Nifty 50 equivalent in US: S&P 500 index fund or Parag Parikh Flexicap Geographic diversification

Exception for active funds: For the mid-cap and small-cap allocation, a proven active fund with a 10+ year track record and consistent manager tenure can outperform index alternatives in Indian markets — because mid/small-cap markets are less efficiently priced than large-cap. However, keep it to one active fund maximum in each category.

For Debt: Match the Instrument to the Timeline

Duration Best Instrument Avoid 0–6 months Liquid Fund, Overnight Fund FD (premature penalty), equity (volatility) 6 months–2 years Low Duration / Ultra Short Duration Fund Active debt funds with credit risk 2–5 years Short Duration Fund Long duration funds (interest rate risk) 5+ years PPF, EPF, Conservative Hybrid Fund FD (tax-inefficient in high brackets) Inflation hedge Sovereign Gold Bond (8-year) Gold ETF (no interest income)

The debt-to-income ratio framework also informs how much of your monthly surplus should go to debt investments versus equity — investors with high EMI obligations naturally have lower equity SIP capacity and should model this explicitly.

For Gold: Sovereign Gold Bonds, Not Physical Gold

Physical gold jewellery as an investment is an Indian cultural habit, not a financial strategy. Making charges of 10–25%, GST, storage costs, and illiquidity make jewellery a poor investment.

Sovereign Gold Bonds (SGBs) are categorically superior:

- 2.5% guaranteed semi-annual interest (taxable)

- Gold price appreciation on maturity

- Zero making charges, zero storage cost

- LTCG completely exempt on maturity (8 years)

- Can be traded on exchange if needed before maturity

For a FIRE-focused SIP portfolio, SGBs are the gold component — purchased during RBI issuance windows (typically 4–6 per year) and held to 8-year maturity for maximum tax efficiency.

The SIP Allocation Optimiser: Putting It All Together

The question every Indian investor eventually asks: “Given my specific income, goals, and timeline, what exactly should my SIP breakdown look like?”

Here are three complete, practical SIP allocation blueprints for different investor profiles.

Blueprint 1: The Young Professional (Age 27, ₹80,000/month in-hand, Single)

Goals:

- Emergency fund: ₹3 lakh (already partially built)

- FIRE at 55 (28-year horizon)

- House in 7 years (₹20 lakh down payment target)

Monthly SIP capacity: ₹20,000

| Goal | Fund Type | Fund Name / Category | SIP Amount | Notes |

|---|---|---|---|---|

| Emergency Fund | Liquid Fund | HDFC Liquid or equivalent | ₹2,000 | Until ₹3L target is reached |

| House Down Payment | Short Duration Debt | ICICI Pru Short Term | ₹3,000 | Stable, low-risk allocation |

| House Down Payment | Conservative Hybrid | HDFC Balanced Advantage | ₹2,000 | Moderate growth + stability |

| FIRE / Retirement | Nifty 50 Index | UTI / Nippon Nifty 50 | ₹7,000 | Core large-cap exposure |

| FIRE / Retirement | Nifty Next 50 Index | UTI Nifty Next 50 | ₹4,000 | Higher growth potential |

| FIRE / Retirement | International Index | Motilal S&P 500 / PPFAS | ₹2,000 | Global diversification |

| Total | — | — | ₹20,000 | — |

Plus: PPF ₹1.5 lakh/year (₹12,500/month equivalent) — handled as annual lump sum or monthly.

Step-up: 10% annually on FIRE SIPs. 0% on house down payment SIPs (amount stays fixed as goal approaches).

Expected FIRE corpus at 55 (28 years, ₹13,000 FIRE SIP + step-up + PPF): ₹3.8–4.5 crore.

Blueprint 2: The Dual-Income Family (Both 35, Combined ₹2,50,000/month, 1 Child Age 3)

Goals:

- Child’s engineering/MBA education in 15 years (target: ₹50 lakh inflation-adjusted)

- FIRE at 55 (20-year horizon)

- Upgrade home in 8 years (₹30 lakh own contribution)

Monthly SIP capacity:

| Goal | Fund Type / Category | Fund Name / Index | SIP Amount |

|---|---|---|---|

| Child Education | Nifty 50 Index | UTI Nifty 50 | ₹8,000 |

| Child Education | Mid-Cap Index | Motilal Midcap 150 | ₹4,000 |

| Home Upgrade | Conservative Hybrid | Balanced Advantage Fund | ₹8,000 |

| Home Upgrade | Short Duration Debt | ICICI Pru Short Term | ₹4,000 |

| FIRE (Spouse 1) | Nifty 50 Index | UTI Nifty 50 | ₹10,000 |

| FIRE (Spouse 1) | Nifty Next 50 | UTI Next 50 | ₹6,000 |

| FIRE (Spouse 2) | Mid-Cap Index | Motilal Midcap 150 | ₹8,000 |

| FIRE (Spouse 2) | International Index | Motilal S&P 500 | ₹6,000 |

| — | Gold (SGB Proxy SIP) | Quarterly Lump Sum Equivalent | ₹6,000 |

| Total | — | — | ₹60,000 |

Plus: Both EPFs (auto), both PPFs (₹3 lakh/year combined).

Expected education corpus at 15 years (12% CAGR, 10% step-up): ₹56.4 lakh — inflation-adjusted target hit.

Expected FIRE corpus at 55 (20 years, ₹30K FIRE SIPs + EPF + PPF + step-up): ₹5.8–₹7.2 crore. Well into Fat FIRE territory.

Blueprint 3: The Late Starter (Age 45, ₹1,80,000/month, Kids in College Soon)

Many Indians reach 45 having under-invested for retirement. The question is not “why didn’t I start earlier?” — that time is gone. The question is: what is the most efficient allocation with 10–15 years remaining?

Reality check: With a 10-year horizon to retirement at 55, dramatic equity exposure is no longer appropriate. But completely abandoning equity is equally wrong — you still need 20–30 years of retirement funded from this corpus.

Monthly SIP capacity:

| Goal | Fund Type / Category | Fund Name / Index | SIP Amount |

|---|---|---|---|

| FIRE Corpus | Nifty 50 Index | UTI Nifty 50 | ₹15,000 |

| FIRE Corpus | Conservative Hybrid | Balanced Advantage Fund | ₹12,000 |

| FIRE Corpus | Short Duration Debt | ICICI Pru Short Term | ₹10,000 |

| FIRE Bucket 1 (Safety) | Liquid Fund | HDFC Liquid | ₹8,000 |

| Gold Allocation | SGB (Lump Sum Proxy) | — | ₹5,000 |

| Total | — | — | ₹50,000 |

Allocation: 55% equity, 35% debt, 10% gold — appropriate for a 10-year horizon with bond tent beginning.

Plus: Maximise VPF (Voluntary Provident Fund) through employer — at 8.25% EEE, every extra rupee here compounds tax-free.

Expected corpus at 55 (10 years, ₹50K SIP, 15% step-up for 3 years then flat): ₹1.15–₹1.4 crore from SIPs alone, plus EPF corpus. Likely total: ₹2.2–₹2.8 crore. Sufficient for Lean FIRE or Barista FIRE with supplemental income.

As we showed in the can I retire with ₹2 crore guide, ₹2 crore is achievable for a comfortable retirement for many Indian households — especially with reduced expenses post-retirement and passive income sources.

The Annual SIP Review Checklist

A SIP allocation strategy is not set-and-forget. It requires annual review to ensure goals, allocations, and market performance remain aligned.

Once per year, on a fixed date (April 1 or January 1), review:

1. Are all goals still valid? Goals change — a divorce, a second child, a job change, a windfall — any of these might require restructuring.

2. Has your savings rate changed? If your income increased by 20%, has your total SIP amount also increased? Use the ideal savings rate guide to verify you are on track for your income level.

3. Has any fund significantly underperformed its benchmark for 3+ consecutive years? If yes, it is a candidate for replacement — but only after confirming the underperformance is structural, not temporary.

4. Are near-term goals on glide path? Goals within 5 years should have begun the equity-to-debt shift. Run the numbers: is the current corpus + remaining contributions sufficient to hit the target without equity risk?

5. Has life insurance kept pace with corpus growth? As your corpus builds, your family’s dependency on insurance decreases. But until FIRE is achieved, term insurance coverage should be maintained at approximately 15–20x annual income.

6. Check your financial health score. The Wealthpedia Financial Health Score gives a structured assessment across 7 pillars — emergency preparedness, insurance, debt management, investment rate, goal alignment, tax efficiency, and net worth trajectory. A score below 60 needs action regardless of how your SIPs look on paper.

The Single Biggest SIP Allocation Mistake in 2026

We will end with the one mistake that, if you are making it, costs more than all other mistakes combined.

Investing without knowing your FIRE number.

If you do not know how much corpus you need to retire, you cannot know whether your current SIP allocation is sufficient, too aggressive, or laughably inadequate. You are driving without a destination.

The FIRE number calculator takes your expected monthly expenses, inflation rate, expected retirement duration, and safe withdrawal rate — and tells you exactly how large a corpus you need. Once you have that number, every SIP decision becomes a calculation, not a guess.

The Multi Goal FIRE Planner goes further — it lets you model multiple goals simultaneously, test different monthly SIP amounts, run a step-up SIP projection, and see whether your current trajectory reaches your FIRE number by your target date.

Without this number, your SIP allocation is just an activity. With it, it becomes a plan.

Conclusion: SIP Allocation Is Not a Product Decision — It Is an Engineering Decision

Choosing between two Nifty 50 index funds from different AMCs is a product decision. Worth 5 minutes.

Deciding how much equity vs debt to hold, how to split across four goal categories, how aggressively to step up, how to glide-path near goals to safety, and how to structure the transition from accumulation to withdrawal — that is an engineering decision. Worth as much time as it takes to get right.

The best SIP allocation strategy for Indians in 2026 is not a list of recommended funds. It is a framework:

- Every goal gets its own dedicated SIP

- Every SIP is matched to a timeline and risk profile

- Every rupee has a job

- Every year the allocation evolves toward its target

- And every 12 months you review, rebalance, and step up

Get this right and the fund selection becomes almost secondary. Get this wrong and even the best funds cannot save you.

Use the Wealthpedia SIP Allocation Optimizer and the Multi Goal FIRE Planner to build your personalised allocation — not based on what a magazine recommended, but based on your actual goals, your actual income, and your actual FIRE target.

That is the only SIP strategy that actually works.

Frequently Asked Questions: SIP Allocation Strategy India

What is the best SIP allocation strategy for retirement in India?

The best strategy is goal-based allocation: separate SIPs for retirement (equity-heavy, 75–85% equity index funds), education (balanced, 60% equity shifting to debt over time), near-term goals (debt-heavy), and emergency fund (liquid funds only). Within the retirement SIP, prioritise Nifty 50 Index Fund (35–40%), Nifty Next 50 (20%), Mid-Cap Index (15%), International Index (15%), and Gold/Debt (10%).

How should I split my SIP between equity and debt?

The split depends on your goal horizon. For goals 15+ years away: 75–85% equity, 10–20% debt, 5% gold. For 7–15 year goals: 60% equity, 30% debt, 10% gold. For 3–7 year goals: 40% equity, 50% debt, 10% gold. For goals under 3 years: 0–20% equity, 80–100% in stable debt instruments. Age-based rules (like 100 minus age) are oversimplified and do not account for Indian inflation levels.

Should I invest in a single SIP or multiple SIPs?

Multiple SIPs — one per goal category. A single SIP creates goal-timeline conflicts (your 3-year house goal and 25-year retirement goal cannot coexist in the same equity fund without creating dangerous decisions during market downturns). Separate SIPs for separate goals prevent the most costly behavioural mistakes.

How much should I step up my SIP every year?

10% annual step-up is the standard recommendation. It roughly tracks salary growth for most Indians, keeps the investment burden proportional, and produces dramatically better outcomes — as shown in our analysis, a 10% step-up on ₹10,000/month doubles the final corpus versus a flat SIP over 25 years. Implement it as an automated instruction, not a manual annual reminder.

Is Nifty 50 index fund enough for SIP or do I need more funds?

Nifty 50 alone is a valid starting portfolio — better than most actively managed multi-fund portfolios. But adding Nifty Next 50 (for historical growth premium) and an international index fund (for geographic diversification) significantly improves long-term outcomes without adding complexity. Three index funds plus debt (PPF/EPF) is a complete long-term SIP portfolio.

How do I build a SIP for my child’s education?

Start as early as possible. Use a two-fund structure: Nifty 50 Index Fund (60%) and Mid-Cap Index Fund (40%) for a 15+ year horizon. With a 10% annual step-up, ₹5,000–₹8,000/month started at birth is typically sufficient for ₹40–₹60 lakh education corpus at 18 years. Begin the equity-to-debt glide path 5 years before college. Our detailed child education SIP guide has the complete scenario analysis.

What is the minimum SIP amount to start with?

As low as ₹500/month on most platforms. But ₹1,000–₹5,000/month is a more practical minimum to build meaningful compounding. The amount matters less than the commitment to step up 10% every year. A ₹2,000/month SIP with 10% annual step-up for 25 years at 12% CAGR builds ₹37.8 lakh — more than a ₹5,000 flat SIP (₹28.5 lakh) over the same period.

How many funds should I have in my SIP portfolio?

4–6 funds maximum for most investors. More than this creates portfolio overlap (multiple large-cap funds holding the same stocks), complexity in tracking, and emotional over-monitoring. A well-structured 4-fund portfolio (Nifty 50 + Nifty Next 50 + Mid-Cap + International) covers the equity spectrum comprehensively.

Should I use active funds or index funds for SIP?

For large-cap (Nifty 50, Nifty Next 50): index funds decisively. Data shows fewer than 15% of active large-cap funds beat the index after fees over 10 years. For mid-cap and small-cap: a case exists for quality active funds with long track records and stable fund management. The cost advantage of index funds (0.1% vs 1.5–2% expense ratio) compounds to lakhs over 20+ years.

What happens to my SIP during a market crash?

The right answer: nothing changes. Continue all SIPs without modification. A market crash during SIP accumulation is a buying opportunity — you are purchasing more units at lower prices, improving your average cost of acquisition. The worst action during a crash is stopping or redeeming SIPs. The second worst is doing nothing — the correct action is to actively consider increasing the SIP amount if cash flow allows.

How should I rebalance my SIP portfolio?

Once per year, on a fixed calendar date. Check actual vs target allocation for each goal. If any asset class has drifted more than 5% from target, redirect new SIP contributions to the underweight class (no selling needed during accumulation, which avoids tax events). In retirement, use bucket replenishment as the rebalancing mechanism.

What is the ideal SIP allocation for someone earning ₹50,000/month?

Invest 20–25% of income (₹10,000–₹12,500/month) across goals. Suggested: ₹2,000 emergency fund top-up, ₹6,000 retirement SIP (Nifty 50 + Nifty Next 50), ₹2,000 near-term goal SIP (debt), ₹2,000–₹2,500 PPF annual contribution (monthly equivalent). See our full guide on achieving FIRE on ₹50K salary.

Should mid-cap and small-cap funds be part of my SIP?

Mid-cap: yes, for goals 12+ years away (10–20% allocation). Small-cap: optional, only for goals 15+ years away, limited to 5–10% maximum. Both mid and small-cap add return potential but significantly increase volatility. A first-time investor should establish Nifty 50 + Nifty Next 50 before adding mid or small-cap exposure.

How do I know if my SIP amount is sufficient for retirement?

Use the FIRE Number Calculator to find your target corpus, then reverse-engineer the required SIP amount. Alternatively, enter your current SIP in the Multi Goal FIRE Planner and see whether the projected corpus meets your retirement need. If the gap is large, increasing the SIP or adding step-up is more effective than changing fund selection.

Is SIP better than lump sum investment?

For most retail investors: SIP wins for behavioural reasons. Lump sum mathematically outperforms SIP when markets are rising continuously, but most investors cannot time lump sum investments correctly and panic-sell during downturns. SIPs enforce discipline through automated deductions that remove human decision-making from the equation. For large windfalls (bonuses, inheritances), a systematic transfer plan (STP) — parking in liquid fund and transferring to equity monthly over 12 months — provides the discipline of SIP on lump sum capital.

What should I do if I cannot afford to invest right now?

Start with whatever you can — even ₹500/month. The habit of systematic investing matters more than the initial amount. Address what is stopping full participation: identify which financial mistakes are draining your monthly surplus and eliminate them. High-cost debt (credit cards, personal loans) paying 18–36% interest should be cleared before investing — guaranteed 18% return on debt repayment beats any equity market expectation.

How does PPF fit into a SIP allocation strategy?

PPF is the debt component of your long-term SIP strategy. At ₹1.5 lakh/year maximum with EEE tax status and 7.1% guaranteed return, it is India’s best risk-free instrument for investors in the 20–30% tax bracket. Think of PPF as the guaranteed bond component of your portfolio — it does not replace equity mutual fund SIPs but complements them.

Should I include international funds in my SIP?

Yes — a 10–15% allocation to international index funds (primarily US S&P 500 or global developed markets) provides genuine diversification unavailable in Indian equity. Indian markets are concentrated in financials, IT, and energy. US markets offer tech, healthcare, consumer sectors. International allocation also provides a natural USD hedge against INR depreciation over long horizons.

How long should I keep a SIP running?

For FIRE/retirement goals: until your corpus reaches the FIRE number — not a day before. A common error is stopping a well-performing SIP early because the “number looks good” without modelling whether it sustains 25–30 years of withdrawals. For education goals: until 5 years before the target date (at which point glide path to debt begins). Never stop a SIP during a market downturn.

What is the role of debt mutual funds in SIP allocation?

Debt mutual funds serve three roles: emergency buffer (liquid/overnight funds), stability anchor for near-term goals (short-duration funds), and portfolio rebalancing destination during equity overperformance (conservative hybrid funds). They do not drive wealth creation — equity does. They manage risk, provide liquidity, and smooth the volatility that equity inherently carries.

How does the Waterfall SIP model work?

The Waterfall Model prioritises goals in order of urgency and irreversibility: (1) emergency fund, (2) EPF/PPF tax-advantaged instruments, (3) child education, (4) retirement/FIRE, (5) near-term aspirational goals. Each level is funded in sequence — you do not start Level 4 retirement SIPs while Level 1 emergency fund is unfunded. Once each level is adequately funded, excess cash flow cascades to the next. Read our detailed Waterfall SIP guide for the implementation details.

Should I stop my SIP if the market falls 30%?

Never. Stopping a SIP during a market fall is locking in the panic decision. You are selling the decision to buy cheap. The investor who stopped SIPs in March 2020 (COVID crash) missed the recovery that gave 90–100% returns over the following 18 months. The investor who increased their SIP in March 2020 — even by 20% — multiplied the benefit of the recovery. Market crashes during SIP accumulation are gifts. Accept them.

Is the SIP Allocation Optimiser tool useful for my planning?

The Wealthpedia SIP Allocation Optimizer inputs your income, goals, timelines, and current savings — and outputs the optimal SIP allocation across categories. It is most useful for first-time investors building a portfolio from scratch and for existing investors who suspect their allocation is misaligned with their goals but are not sure how to fix it.

How do I build a SIP portfolio for early retirement?

The core accumulation allocation for FIRE is: 75–85% equity (Nifty 50 + Nifty Next 50 + Mid-Cap + International), 10–15% debt (PPF + EPF), 5% gold (SGB). Implement 10% annual step-up from Day 1. Review the complete early retirement calculator guide to calculate your FIRE number and the required monthly SIP. Model the full scenario in the Multi Goal FIRE Planner before finalising the allocation.

What is the one thing I should do differently in my SIP today?

Separate your goals. Take your current undifferentiated SIP and ask: which goal is this for? If you cannot answer, that is the problem. Spend one hour identifying your top 3–4 financial goals, assigning each a timeline and target corpus, and restructuring your SIP allocation so each goal has its own dedicated fund with the right risk profile for that timeline. That single act of goal-separation will do more for your financial outcome than any fund switch, any market timing decision, or any investment tip you will ever encounter.

Disclaimer: This article is for educational and informational purposes only. All return assumptions are based on historical data and are not guaranteed for future performance. SIP investments are subject to market risk. Please read all scheme-related documents carefully before investing. Wealthpedia is not a SEBI-registered investment advisor. Consult a qualified financial advisor before making investment decisions. Wealthpedia® is a registered trademark (TM No. 4910385).

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up