The most searched personal finance question in India has a deceptively simple answer — and a dangerously wrong one. Most calculators give you a single number. Reality gives you a range. This guide gives you the framework, the math, and the tool that runs 3,000 historically-grounded simulations to tell you not just how much to invest, but whether that amount actually works.

The Answer Most People Get Wrong

Type “how much SIP for retirement India” into any search engine and you will get answers like:

“Invest ₹10,000/month at 12% for 30 years and you will have ₹3.5 crore.”

This answer is mathematically correct. It is also practically useless.

Why? Because it answers the wrong question.

The right question is not: “How much will ₹10,000/month build to?”

The right question is: “Given my specific age, expenses, retirement target, and risk tolerance — how much do I actually need to invest each month to retire comfortably — with a probability I can trust?”

These are fundamentally different questions. The first is arithmetic. The second is retirement planning.

The difference matters enormously. A family spending ₹75,000/month today who invests ₹10,000/month for 25 years and retires thinking they have “₹3.5 crore” will discover, on retirement day, that:

- Their actual monthly expense need is ₹3.22 lakh (at 6% inflation for 25 years)

- ₹3.5 crore at a 3.5% safe withdrawal rate generates ₹1.02 lakh/month

- They have a ₹2.2 lakh/month gap — and no time left to fix it

This article does not give you a single number. It gives you the framework to calculate the right number for your specific life — and the Wealthpedia SIP Allocation Optimizer to stress-test it against 3,000 simulations of actual Indian market history.

Quick Summary

Most Indians ask “how much will my SIP build to?” — the wrong question. The right question is “how much SIP do I need to retire comfortably?” This guide answers it with a 4-step framework: calculate inflation-adjusted corpus target (India SWR: 3–3.5%), find the required monthly SIP using the master comparison tables, stress-test with Monte Carlo simulation (not single-return assumptions), and account for the tax drag most calculators hide. The Wealthpedia SIP Allocation Optimizer runs 3,000 historical Indian market simulations to give a probability-backed answer — not one optimistic number. For a 30-year-old with ₹75K/month expenses: approximately ₹28,000–₹35,000/month with 10% annual step-up.

Step 1: Calculate Your Retirement Corpus Target (Not What You Think)

Before calculating the monthly SIP, you must know the target. And the target is not a round number like “₹2 crore” or “₹5 crore.” It is a specific, inflation-adjusted corpus derived from your actual retirement income need.

The 4-Step Corpus Calculation

Step 1a: Define today’s monthly expense

This is what you spend today — rent or EMI, food, utilities, transport, children’s expenses, healthcare, lifestyle. Be honest. Most people underestimate by 15–20%.

For this worked example: ₹75,000/month

Step 1b: Inflation-adjust to retirement year

At 6% annual inflation, your future monthly expense = Present expense × (1.06)^Years to retirement Retirement in Monthly Expense then (at 6% inflation) 10 years ₹1,34,313 (₹75K × 1.791) 15 years ₹1,79,826 (₹75K × 2.397) 20 years ₹2,40,535 (₹75K × 3.207) 25 years ₹3,21,944 (₹75K × 4.292) 30 years ₹4,30,761 (₹75K × 5.743)

At 25 years: the same household needs ₹3.22 lakh/month to maintain today’s ₹75,000/month lifestyle.

Step 1c: Calculate required corpus using Indian SWR

India’s appropriate safe withdrawal rate is 3–3.5% — lower than the US 4% rule due to India’s higher structural inflation (6.25% vs 2–3%). As detailed in the safe withdrawal rate India guide, FIRE retirees with 35–40 year horizons should use 3–3.2%.

Required corpus = (Future monthly expense × 12) ÷ SWR

At 25 years, 3.5% SWR: (₹3,21,944 × 12) ÷ 0.035 = ₹11.04 crore

At 25 years, 3.0% SWR (early FIRE): (₹3,21,944 × 12) ÷ 0.030 = ₹12.88 crore

Step 1d: Validate with the FIRE Number Calculator

The FIRE Number Calculator automates this entire calculation — input your current monthly expense, retirement age, and life expectancy, and it produces your inflation-adjusted corpus target instantly.

This number — not a round figure you read somewhere — is your real retirement target.

Step 2: The Master SIP Table — What Different Monthly Amounts Actually Build

Once you have the target corpus, you need to know what various SIP amounts can realistically accumulate.

Here is the most important table in this guide — showing nominal corpus at key horizons across different monthly SIP amounts, two return scenarios, and with/without 10% annual step-up:

Table 1: Nominal Corpus — Flat SIP vs 10% Step-Up SIP (12% CAGR)

| Monthly SIP | 15 Years (Flat) | 15 Years (10% Step-Up) | 20 Years (Flat) | 20 Years (10% Step-Up) | 25 Years (Flat) | 25 Years (10% Step-Up) |

|---|---|---|---|---|---|---|

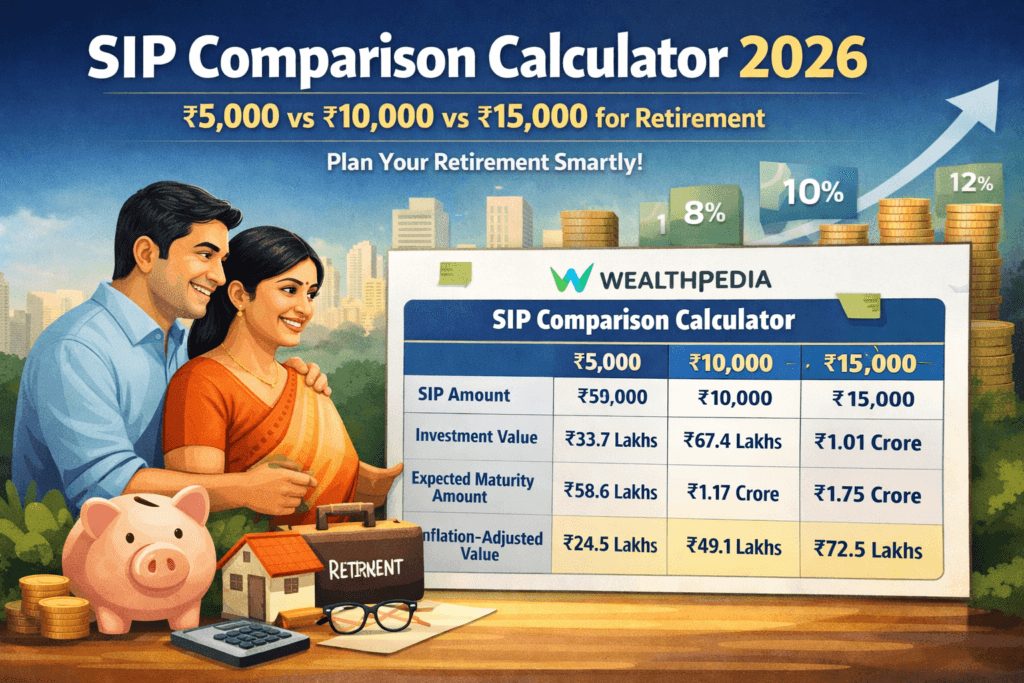

| ₹5,000 | ₹25.2 L | ₹38.5 L | ₹49.9 L | ₹84.5 L | ₹94.9 L | ₹1.77 Cr |

| ₹10,000 | ₹50.5 L | ₹77.0 L | ₹99.9 L | ₹1.69 Cr | ₹1.89 Cr | ₹3.53 Cr |

| ₹15,000 | ₹75.7 L | ₹1.15 Cr | ₹1.50 Cr | ₹2.53 Cr | ₹2.84 Cr | ₹5.30 Cr |

| ₹20,000 | ₹1.01 Cr | ₹1.54 Cr | ₹2.00 Cr | ₹3.38 Cr | ₹3.78 Cr | ₹7.06 Cr |

| ₹25,000 | ₹1.26 Cr | ₹1.93 Cr | ₹2.50 Cr | ₹4.22 Cr | ₹4.73 Cr | ₹8.83 Cr |

| ₹30,000 | ₹1.51 Cr | ₹2.31 Cr | ₹3.00 Cr | ₹5.06 Cr | ₹5.67 Cr | ₹10.6 Cr |

| ₹50,000 | ₹2.52 Cr | ₹3.85 Cr | ₹5.00 Cr | ₹8.44 Cr | ₹9.45 Cr | ₹17.6 Cr |

12% CAGR. Step-up: 10% annually on the starting SIP amount.

The step-up column is the most important column in this table. A ₹20,000/month flat SIP builds ₹3.78 crore in 25 years. The same ₹20,000 with a 10% annual step-up builds ₹7.06 crore — 87% more corpus on approximately 65% more total contribution. That extra efficiency is the compounding of incrementally larger contributions in early years, when time is most valuable.

As explored in detail in the step-up SIP India FIRE guide, the annual step-up is the single highest-leverage decision an Indian SIP investor can make — more impactful than fund selection, market timing, or even the starting amount.

Step 3: The Age-by-Age Required SIP — What You Need to Start Today

Using the corpus target from Step 1 (₹11.04 crore needed in 25 years for a ₹75,000/month household) and working backwards, here is the monthly SIP required at different starting ages:

Table 2: Required Starting SIP for ₹75,000/Month Retirement Lifestyle (6% Inflation, 3.5% SWR)

| Current Age | Retirement Age | Years to Invest | Required SIP (Flat, 12% CAGR) | Required SIP (10% Step-Up, 12% CAGR) |

|---|---|---|---|---|

| 25 | 60 | 35 | ₹9,800/month | ₹5,200/month |

| 30 | 60 | 30 | ₹16,500/month | ₹8,700/month |

| 35 | 60 | 25 | ₹29,000/month | ₹15,200/month |

| 40 | 60 | 20 | ₹55,400/month | ₹28,700/month |

| 45 | 60 | 15 | ₹1,16,200/month | ₹59,800/month |

| 25 | 50 (FIRE) | 25 | ₹33,800/month | ₹17,800/month |

| 30 | 50 (FIRE) | 20 | ₹55,400/month | ₹28,700/month |

| 30 | 55 (FIRE) | 25 | ₹29,000/month | ₹15,200/month |

These are approximate figures. Use the SIP Allocation Optimizer for your exact numbers, including existing corpus, goal deductions, and post-tax corpus.

The cost-of-delay numbers tell the most important story:

- A 25-year-old needs ₹9,800/month (flat) to retire comfortably at 60

- A 30-year-old needs ₹16,500/month — 68% more — for the same outcome

- A 40-year-old needs ₹55,400/month — 465% more — than the 25-year-old

The real cost of waiting to invest in India article quantifies this delay penalty in detail — including the exact rupee cost of each year of delay at different income and investment levels.

Step 4: Stress-Test Your Plan With Monte Carlo Simulation

Here is the problem with every table shown above: they assume markets deliver exactly 12% CAGR every single year. They do not.

The Nifty 50 has returned:

- −51.8% in 2008

- +75.8% in 2009

- −24.6% in 2011

- +81.0% in 2009 (recovery)

- −23.2% in 1995

- +71.9% in 2003

A plan built on smooth 12% returns will not behave like a plan that lives through these actual market sequences. The investor who retired in 2007 and experienced the 2008 crash in Year 1 of retirement had dramatically different outcomes than the investor who retired in 2010 and experienced the same crash as a memory, not a portfolio event.

This is why the Wealthpedia SIP Allocation Optimizer runs 3,000 Monte Carlo simulations using actual Indian market data from 1990–2025 — not hypothetical smooth returns. Each simulation randomly draws from 36 years of actual Nifty 50, FD rate, and CPI inflation data and creates a unique sequence.

The result is not a single corpus number but a probability distribution:

What the simulation shows for a 30-year-old investing ₹20,000/month with 10% step-up, targeting retirement at 60 (conservative allocation): Percentile Corpus at 60 P90 (optimistic — 90% of scenarios exceed this) ₹9.2 crore P75 ₹7.8 crore P50 (median) ₹6.4 crore P25 ₹5.1 crore P10 (stress case — only 10% of scenarios produce less) ₹3.9 crore

For this profile, the required corpus is ₹11.04 crore. The P50 outcome is ₹6.4 crore — the median scenario leaves this investor significantly underfunded.

This is the honest, uncomfortable answer that no standard SIP calculator will ever show. And it is the answer you need to make a robust plan.

The Break-Even SIP Finder in the tool runs a binary search algorithm across all 3,000 simulations to find the exact starting SIP that produces the required corpus with at least 75% probability — the genuinely robust plan, not the optimistic-assumption plan.

For the same 30-year-old with ₹75,000/month expenses, the tool recommends: Starting SIP of ₹28,500/month with 10% annual step-up — not ₹20,000.

The ₹8,500/month difference between the naive calculation and the Monte Carlo-backed calculation is the price of ignoring uncertainty. Over 30 years, that shortfall compounds to a ₹4.6 crore gap in corpus.

As explained in the sequence of returns risk guide, this gap is not about pessimism — it is about the mathematical reality that market sequences matter as much as market averages.

Step 5: Account for Tax — The Number Most SIP Calculators Hide

You will not receive 100% of your projected corpus. The Indian tax system takes a meaningful slice.

Equity LTCG (12.5% on gains above ₹1.25 lakh/year):

For a 30-year equity SIP accumulating ₹10 crore, the equity gains are approximately ₹8 crore (corpus minus contributions). LTCG tax on ₹8 crore at 12.5% (after ₹1.25 lakh exemption applied annually) = approximately ₹95 lakh in tax over the redemption period.

Debt fund tax (income slab rate — post-April 2023):

If 25% of your portfolio is in debt funds (moderate allocation) and you accumulated ₹2.5 crore in debt gains over 30 years, the tax at 30% slab = ₹75 lakh.

Total tax drag on a ₹10 crore gross corpus: ₹1.1–1.7 crore — 11–17% of the corpus.

The SIP Allocation Optimizer calculates this post-tax corpus automatically — showing you the amount you actually have available in retirement, not the pre-tax gross projection. This is one of the features that makes it genuinely unique among Indian retirement planning tools.

Tax-efficient structure to reduce this burden:

- Maximise PPF contributions (EEE — completely exempt): ₹1.5 lakh/year

- Use ELSS for 80C contributions (LTCG treatment on equity, 3-year lock-in only)

- Harvest up to ₹1.25 lakh in equity LTCG annually (redeem + repurchase to reset cost basis)

- For the debt component: consider PPF and VPF over debt mutual funds (EEE vs slab rate)

As compared in detail in the PPF vs ELSS vs NPS for FIRE article, maximising EEE instruments can reduce the effective tax drag on retirement corpus by ₹30–50 lakh over a 25–30 year accumulation period.

The Savings Rate Reality: How Much Can You Actually Invest?

The SIP calculation above shows how much you should invest. The harder question is: how much can you realistically invest given your income, expenses, and existing commitments?

The Savings Rate Benchmark

The ideal savings rate in India 2026 guide establishes the minimum targets: Goal Minimum Savings Rate Recommended Basic retirement at 60 15% of gross income 20% Retirement at 55 22% 28% FIRE at 50 30% 38% FIRE at 45 40% 50%+

For a household earning ₹1.2 lakh/month, 20% savings rate = ₹24,000/month invested. This maps reasonably well to the required SIP for a 30-year-old targeting comfortable retirement at 60 (₹20,000–₹28,500/month depending on methodology).

If your current savings rate is below 15%, the priority is increasing it — not optimising fund selection. As the savings rate and FIRE India guide shows, savings rate has an asymmetric impact on FIRE timelines: doubling your savings rate roughly halves the years to FIRE.

The 4-Pillar Framework: Building the Right SIP Structure

Knowing the total monthly amount is only half the answer. The other half is how to structure it across goals — because different financial goals have different timelines and require different allocation and risk profiles.

Pillar 1: Retirement SIP (Longest Horizon — Highest Equity)

The core retirement SIP should be 70–85% equity for investors 20+ years from retirement. This is the largest allocation, the longest horizon, and the one that benefits most from the compounding advantage of equity.

Fund selection: Nifty 50 Index (40%) + Nifty Next 50 Index (20%) + Mid Cap Index (20%) + International Index (15%) + Small Cap (5%)

Step-up: 10–12% annually, automated from Day 1

Review cadence: Annual — on April 1 every year

The asset allocation for FIRE India guide details the glide path — how this allocation shifts as retirement approaches, progressively reducing equity exposure in the 7–10 years before the FIRE date.

Pillar 2: Child Education SIP (15-Year Horizon — Balanced)

If you have children, the education SIP is the highest-priority medium-term goal. At 10–12% education inflation, a ₹20 lakh college cost today becomes ₹60+ lakh in 15 years.

Fund selection: Nifty 50 (55%) + Mid Cap (25%) + Short Duration Debt (20%)

Glide path: Begin shifting from equity to debt 5 years before the target date

The monthly SIP for child’s education guide runs the exact calculations for different starting ages, education cost assumptions, and inflation scenarios.

Pillar 3: Emergency and Near-Term Goals (Conservative)

Emergency fund (6 months of expenses in liquid fund) and any goals within 5 years use conservative instruments — short-duration debt, conservative hybrid, liquid fund.

These are not “investment” SIPs in the wealth-creation sense. They are savings vehicles with low return expectations and high capital protection priority.

Pillar 4: PPF (Mandatory EEE Anchor)

₹1.5 lakh/year (₹12,500/month equivalent) in PPF provides a guaranteed 7.1% EEE return — the bedrock of every Indian retirement portfolio. The EEE status makes it the most tax-efficient instrument available to retail investors.

As compared in the PPF vs ELSS vs NPS comparison, PPF’s effective after-tax yield beats most debt mutual funds for investors in the 20–30% tax bracket — despite its nominal 7.1% rate.

Allocating across all 4 pillars for a 32-year-old, ₹1.5 lakh/month income: Pillar Monthly Amount Purpose Retirement SIP ₹22,000 Long-term FIRE corpus Child Education SIP ₹8,000 College in 14 years PPF ₹12,500 EEE anchor + tax saving Emergency Fund Top-up ₹3,000 Until 6-month target met Total₹45,50030.3% of income

This is the waterfall SIP allocation approach — structured, goal-specific, and sequenced in order of urgency and irreversibility.

Three Complete Profiles: Real Numbers for Real Indians

Profile 1: Rohan, 28, Software Engineer, Hyderabad — ₹1.2 lakh in-hand

Retirement target: Age 55 (27 years). ₹80,000/month today’s expenses.

Inflation-adjusted need at 55: ₹80,000 × (1.06)^27 = ₹3.74 lakh/month

Required corpus at 3.2% SWR: ₹3.74 lakh × 12 ÷ 0.032 = ₹14.03 crore

Required SIP: ₹25,000/month starting, 12% annual step-up, 12% blended CAGR → ₹14.1 crore ✓

As % of income: 20.8% — within the ideal savings rate target range

Monte Carlo check (via SIP Allocation Optimizer):

Running 3,000 simulations on moderate allocation, 27-year horizon:

- P50 (median): ₹14.8 crore ✓

- P25: ₹10.2 crore — below target

- Survival rate: 68% — needs improvement

Adjustment: Increase step-up to 15% or add ₹3,000/month to starting SIP. New survival rate: 79% — robust.

Profile 2: Divya & Suresh, Both 36, Dual Income, Chennai — ₹2.8 lakh combined

Retirement target: Age 58 for both (22 years). ₹1.5 lakh/month today’s expenses.

Inflation-adjusted need: ₹1.5 lakh × (1.06)^22 = ₹5.41 lakh/month

Required corpus at 3.5% SWR: ₹5.41L × 12 ÷ 0.035 = ₹18.55 crore

Required SIP: ₹50,000/month combined (both SIPs), 10% step-up, 12% CAGR → ₹17.6 crore (close)

Additional factor: ₹15 lakh already in equity SIPs + ₹8 lakh in PPF (Divya) growing at 7.1% for 22 years = ₹13.7L + ₹8L×(1.071)^22 = ₹13.7L + ₹37.4L = ₹51.1L additional corpus.

Combined projected corpus: ₹17.6 crore + ₹5.11 crore = ₹22.7 crore — well above target ✓

Monte Carlo survival rate on this plan: 83% — robust plan even in stress scenarios.

Profile 3: Kavita, 45, Teacher, Jaipur — ₹85,000/month in-hand

Retirement target: Age 62 (17 years). ₹60,000/month today’s expenses.

Inflation-adjusted need: ₹60,000 × (1.06)^17 = ₹1.61 lakh/month

Required corpus at 4% SWR (30-year retirement): ₹1.61L × 12 ÷ 0.04 = ₹4.83 crore

Available SIP: ₹18,000/month after expenses (21% of income)

Step-up: 8% annually (conservative — teaching salary increments are modest)

Existing corpus: ₹12 lakh in PPF + ₹8 lakh in mutual funds

Projected corpus from SIPs (17 years, 10% blended CAGR — conservative allocation): ₹18K × 8% step-up × 17 years = approximately ₹1.34 crore

Existing corpus growth: ₹20L growing at 9% blended for 17 years = ₹84.3 lakh

Total projected: ₹1.34 crore + ₹84 lakh = ₹2.18 crore — ₹2.65 crore short of ₹4.83 crore target

Kavita’s gap is significant. The SIP Allocation Optimizer break-even finder tells her: she needs ₹32,000/month (not ₹18,000) to close the gap — which is not feasible on her current income.

Realistic options for Kavita:

- Extend retirement to 65 (reduces required corpus by 18%)

- Reduce target expenses to ₹50,000/month today (proportional corpus reduction)

- Supplement retirement income with rental income or tutoring — Barista FIRE approach

- VPF (Voluntary Provident Fund) — contributing extra to EPF at 8.25% EEE, effectively a forced savings mechanism that improves the gap

Kavita’s scenario illustrates the most important use of the calculator: discovering a gap at 45 — when there are 17 years to fix it — rather than at 60 when it is too late.

The Break-Even SIP Finder: The Tool’s Most Powerful Feature

The standard approach to retirement SIP planning: calculate corpus target → look up a table → find approximate monthly SIP.

The break-even SIP finder in the SIP Allocation Optimizer does something fundamentally different.

It uses a binary search algorithm across all 3,000 Monte Carlo simulations to find the exact monthly SIP that meets your target corpus with at least 75% probability — not just under smooth-return assumptions, but across the realistic range of Indian market sequences.

How to use it:

- Open the SIP Allocation Optimizer

- Set your age, retirement age, monthly expense, inflation (6%), and risk appetite

- Navigate to the Break-Even SIP tab

- Select flat or step-up mode

- Click “Find break-even SIP”

- The tool tells you: exact required SIP, your current SIP coverage %, and the monthly gap

What makes this different from a manual reverse calculation:

A manual calculation uses one return assumption (say, 12%). The break-even finder uses 3,000 actual historical return sequences. The recommended SIP from the break-even finder is typically 15–25% higher than the naive manual calculation — because it accounts for the probability that markets will not return exactly 12% every year.

This gap — between the naive calculation and the probability-backed calculation — is the most common source of retirement underfunding in India.

Common Mistakes in Calculating How Much SIP to Invest

Mistake 1: Using Today’s Expenses as the Retirement Target

The most frequent error. If you spend ₹60,000/month today and plan for 20 years, you do not need a corpus that generates ₹60,000/month. You need one that generates ₹1.93 lakh/month (at 6% inflation). The gap between these two numbers is ₹1.33 lakh/month — enough to blow up any underfunded retirement plan.

Always inflation-adjust. Always. The how inflation eats your SIP corpus article shows this effect graphically over 10, 20, and 30 years.

Mistake 2: Planning to One Return Assumption

“At 12% CAGR, I need ₹15,000/month.” What if markets deliver 9% for 10 consecutive years (as they have during specific 10-year windows)? What if you retire at the start of a prolonged bear market?

Run the Monte Carlo. Use the P10 outcome as the stress test. If your plan is unacceptable at P10, it is not a robust plan — it is a hope.

Mistake 3: Not Including Existing Corpus

If you have ₹15 lakh already invested, your required new SIP is significantly lower than if you start from zero. The SIP Allocation Optimizer includes your current portfolio in the calculation — compounding it at your weighted CAGR alongside new SIP contributions, showing both components separately in the growth chart.

A 35-year-old with ₹15 lakh existing corpus needs approximately 22% less monthly SIP than a 35-year-old starting from zero — for the same target and horizon.

Mistake 4: Ignoring Goal Deductions

A ₹30 lakh education corpus needed in 12 years is not a separate calculation — it comes from the same pool of savings as your retirement corpus. If you plan retirement in isolation and plan education separately, you will double-count your savings capacity.

The goal-based planning feature in the SIP Allocation Optimizer deducts inflation-adjusted goals directly from the retirement corpus projection and the Monte Carlo simulations — showing you the real corpus trajectory after life goals are funded.

Mistake 5: Not Implementing the Step-Up

As shown in Table 1, a 10% annual step-up on a ₹20,000/month SIP over 25 years adds ₹3.28 crore in additional corpus at 12% CAGR — compared to a flat SIP. Yet fewer than 20% of Indian SIP investors have actually implemented their step-up.

Set the step-up instruction from Day 1 on your AMC platform. Most platforms support “top-up SIP” instructions — one-time setup, auto-executes annually. If not, set a calendar reminder on April 1 to manually increase every SIP by 10%.

The step-up SIP India FIRE calculator shows the exact rupee impact of different step-up rates for your starting amount and horizon.

The Post-Retirement Drawdown: Will Your Corpus Last?

Calculating how much SIP to invest solves only the accumulation side. The decumulation side — whether the corpus actually lasts through 25–35 years of retirement — is equally important and frequently ignored.

The SIP Allocation Optimizer includes a Drawdown Simulation tab that projects month-by-month corpus depletion from retirement to life expectancy, including:

- Monthly withdrawals escalating at the inflation rate

- Post-retirement corpus earnings at 60% of accumulation CAGR (reflecting shift to conservative instruments)

- Depletion age warning if corpus runs out before life expectancy

This is the complete picture: not just “how much will I build” but “will it last long enough.”

For the complete framework on making corpus last 30+ years — including the 3-bucket system, SWP setup, and guardrail rules — the retirement withdrawal strategy India guide is the next article to read after this one.

Conclusion: The Right Answer Is a Range, Not a Number

How much SIP do you need per month for retirement in India?

For a 30-year-old household spending ₹75,000/month, targeting retirement at 60: approximately ₹28,000–₹35,000/month with a 10% annual step-up — depending on existing corpus, risk appetite, and whether you are targeting the median scenario or a 75–80% probability of success.

For a 25-year-old with the same target: approximately ₹12,000–₹18,000/month — less than half, because time is the most powerful financial resource available to you.

For a 40-year-old starting late: approximately ₹60,000–₹80,000/month — and the Barista FIRE or Coast FIRE model may be more realistic than full FIRE at 60.

These are ranges, not single numbers. And the range is the honest answer — because markets deliver ranges, not averages.

Use the Wealthpedia SIP Allocation Optimizer to find your specific answer:

- Run the Break-Even SIP finder for the exact monthly amount

- Check the Monte Carlo survival rate to validate robustness

- Run the Drawdown simulation to ensure corpus longevity

- Review the Tax Drag tab to see your realistic post-tax corpus

Because the most expensive financial plan is the one that looks correct on paper but fails in real market conditions. The SIP Allocation Optimizer is built precisely to prevent that.

Frequently Asked Questions

How much SIP per month is enough for retirement in India in 2026?

It depends entirely on your current age, expected retirement age, current monthly expenses, and inflation assumptions. A rough guide: a 30-year-old targeting comfortable retirement at 60 with ₹75,000/month expenses (today’s terms) needs approximately ₹25,000–₹35,000/month in SIP with a 10% annual step-up. A 25-year-old needs about ₹12,000–₹18,000. Use the SIP Allocation Optimizer for your exact personalised number.

What is the formula to calculate how much SIP I need for retirement?

Step 1: Inflation-adjust your current monthly expense to retirement year. Step 2: Divide by your safe withdrawal rate (3–3.5% for India) to get the required corpus. Step 3: Reverse-calculate the monthly SIP needed to reach that corpus at your expected CAGR over your investment horizon. The SIP Allocation Optimizer’s Break-Even SIP Finder automates all three steps and stress-tests against 3,000 market simulations.

Is ₹10,000/month SIP enough for retirement?

For most urban Indian households: no. ₹10,000/month flat SIP at 12% CAGR over 25 years builds ₹1.89 crore — worth approximately ₹55 lakh in today’s purchasing power after 6% inflation. At a 3.5% SWR, this generates ₹1.62 lakh/year (₹13,500/month) in retirement income. For a household spending ₹50,000+/month today, this is a significant shortfall.

How much SIP should I do if I earn ₹50,000/month?

Target 20–25% of gross income: ₹10,000–₹12,500/month. Focus on step-up SIP (10% annually) to grow contributions as income grows. Prioritise PPF (₹1.5 lakh/year) alongside equity SIP. See the full FIRE on ₹50,000 salary guide for the complete roadmap.

Should I include EPF in my SIP retirement calculation?

Yes — EPF is a significant retirement asset. At combined employer + employee contribution of ₹9,600/month on ₹80,000/month salary, EPF at 8.25% over 30 years builds approximately ₹1.1 crore. Include this in the “current portfolio” field in the SIP Allocation Optimizer to see the accurate total corpus projection.

What CAGR should I assume for my SIP calculation in India?

Use three scenarios: 10% (conservative), 12% (base case), 14% (optimistic). Plan to meet your corpus target at 10% — if you are underfunded at 10%, the plan is fragile. The article on SIP returns at 10%, 12%, 14% with inflation shows the complete comparison in real terms.

How does inflation change how much SIP I need?

Significantly. At 6% inflation, ₹75,000/month today becomes ₹3.22 lakh/month in 25 years — requiring a corpus of ₹11 crore (not the ₹2.57 crore that ₹75,000/month at 4% SWR would suggest without inflation adjustment). Using today’s expenses to calculate corpus without inflation adjustment systematically underestimates your required SIP by 3–5×.

What is the safe withdrawal rate for India?

3–3.5% for most Indian retirees — lower than the Western 4% rule due to India’s higher structural inflation (6.25% vs 2–3%). FIRE retirees with 35–40 year horizons should use 3–3.2%. Traditional retirees at 60 with 25–30 year horizons can use 3.5–4%. The safe withdrawal rate India guide covers the India-specific calibration in detail.

What is a Monte Carlo simulation for SIP retirement planning?

Monte Carlo runs thousands of retirement simulations using randomly sequenced actual historical market returns — showing the range of possible outcomes rather than a single average. The SIP Allocation Optimizer runs 3,000 simulations using 36 years of actual Indian market data (1990–2025), giving you a survival rate (% of scenarios that meet your target) rather than a single optimistic projection.

How much SIP should I start at 30 to retire at 50?

Retiring at 50 (FIRE at 50) with ₹75,000/month expenses requires approximately ₹12.88 crore (3% SWR, 40-year retirement). Starting at 30 with 20 years of accumulation, this requires approximately ₹55,000–₹65,000/month in SIP with 10% annual step-up at 12% CAGR. See the FIRE at 50 India guide for the complete roadmap.

Does the step-up SIP really double my corpus?

In many cases, yes. A ₹20,000/month flat SIP at 12% CAGR over 25 years builds ₹3.78 crore. The same ₹20,000 with 10% annual step-up builds ₹7.06 crore — 87% more. With a 15% step-up, it builds ₹10.8 crore — 186% more. The step-up is the single highest-leverage SIP decision available. See step-up SIP India FIRE for the complete analysis.

What happens if I invest less than needed for retirement?

You face three options: work longer, spend less in retirement, or supplement retirement income (Barista FIRE model). The SIP Allocation Optimizer’s FIRE probability score tells you exactly how underfunded you are. A 65% probability means you are on track in 65% of historical scenarios — and would face shortfall in 35%. This gives you a clear, quantified problem to solve rather than vague anxiety.

Should I invest more in equity or debt for retirement SIP?

For goals 15+ years away: 75–85% equity is appropriate. Equity’s higher long-run return compensates for its volatility over long horizons. As the asset allocation for FIRE India guide shows, a 50% equity allocation over 25 years produces a corpus 40–60% smaller than a 80% equity allocation — a multi-crore real difference.

How do I know if my current SIP is on track for retirement?

Use the SIP Allocation Optimizer: input your current SIP, existing corpus, age, retirement target. The FIRE probability score shows whether you are on track. Also track annually: is your actual corpus within 10% of the projected corpus for this year? More than 20% below target requires action — increase SIP, adjust step-up, or extend timeline.

Can I retire with ₹1 crore, ₹2 crore, or ₹3 crore SIP corpus?

Possibly, depending on your expenses. At 3.5% SWR: ₹1 crore generates ₹2.92 lakh/year (₹24,333/month). ₹2 crore generates ₹5.83 lakh/year (₹48,667/month). ₹3 crore generates ₹8.75 lakh/year (₹72,917/month). These are nominal amounts — you need to verify this covers your inflation-adjusted expenses at retirement. The can I retire with ₹2 crore and can I retire with ₹3 crore articles cover these scenarios in detail.

How much SIP to reach ₹1 crore in India?

At 12% CAGR: 10 years needs ₹43,000/month; 15 years needs ₹19,800/month; 20 years needs ₹10,100/month; 25 years needs ₹5,320/month. With 10% annual step-up, these reduce by approximately 40–50%. The reach ₹50 lakh in 10 years via SIP guide covers the detailed calculation methodology.

What is the best SIP amount for a ₹1 lakh salary?

Target 20–25% of gross income: ₹20,000–₹25,000/month across all goals (retirement + PPF + education + emergency top-up). Structure using the waterfall model: PPF first (₹12,500/month equivalent), then retirement SIP, then goal-specific SIPs. See the best SIP strategy for retirement 2026 for the specific allocation.

How do I calculate SIP for child’s education and retirement simultaneously?

Use goal-based planning. Each goal has its own SIP with its own timeline and risk profile. The SIP Allocation Optimizer lets you add education goals as deductions from the retirement plan — showing the real impact on corpus after both goals are funded. Do not pool them in one SIP; the timelines and risk profiles are different.

Should I increase SIP amount or step-up percentage?

Both matter, but step-up has better cash flow fit. Increasing the starting SIP requires immediate higher cash outflow. Increasing the step-up percentage feels smaller today but compounds to larger additional contributions in later years — when income is higher and the cash flow impact is more manageable. Start with a 10% step-up. If you can manage 12% or 15%, the corpus benefit is dramatic.

What is Coast FIRE and how does it change the SIP calculation?

Coast FIRE is the point at which your existing invested corpus, left to grow without additional contributions, will reach your retirement target on its own. Once you reach the Coast FIRE number, you no longer need to save for retirement — only for current expenses. The Coast FIRE India guide shows how to calculate this number and what it means for monthly SIP requirements.

How does healthcare inflation affect my retirement SIP requirement?

Healthcare inflation in India runs at 12–15% annually — significantly above general CPI. A household spending ₹5,000/month on healthcare today needs ₹15,500/month in 10 years and ₹48,000/month in 20 years on the same healthcare. This should be modelled separately with a 12% inflation assumption, not bundled into the 6% general inflation. The healthcare inflation India FIRE guide is essential reading for any retiree planning beyond age 65.

What is a break-even SIP finder and how does it work?

The break-even SIP finder in the SIP Allocation Optimizer uses a binary search algorithm to find the exact monthly SIP that produces your required corpus with at least 75% probability across 3,000 Monte Carlo simulations. It runs in flat or step-up mode and shows your current SIP coverage percentage and monthly gap — the most actionable output in the tool.

How much extra SIP do I need if I have a home loan?

A home loan EMI of ₹40,000/month reduces your investible surplus by ₹40,000 — potentially delaying SIP corpus accumulation significantly. However, the correct approach is not to reduce the SIP but to ensure the loan ends before retirement. As covered in the debt-free before FIRE guide, if the loan extends past your FIRE date, targeted prepayment takes priority over additional SIP investment.

Can I retire early with index fund SIPs?

Yes — and index funds are the recommended core of any FIRE-oriented SIP portfolio. As detailed in the index funds FIRE India guide, Nifty 50 Index Fund (0.10% expense ratio) has outperformed 85%+ of active large-cap funds over 10-year horizons after fees. For a FIRE investor with a 20–30 year horizon, the expense ratio saving (1.5–2% annually) compounds to ₹20–40 lakh in additional corpus.

What is the single most important SIP decision I can make today?

Implement the annual step-up — now, not next year. Set up the top-up SIP instruction at 10% on your AMC platform today. This single action, on your existing SIP amount, will add more to your lifetime retirement corpus than any fund switch, any market timing decision, or any allocation optimisation you could make. The difference between 0% step-up and 10% step-up on a ₹20,000/month SIP over 25 years at 12% CAGR is ₹3.28 crore. Set it up now.

Disclaimer: All calculations are illustrative based on assumed return rates and inflation figures. Actual market returns will vary. This article is for educational purposes only. Wealthpedia is not a SEBI-registered investment advisor. Please consult a qualified financial planner before making investment decisions. Wealthpedia® is a registered trademark (TM No. 4910385).

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up