India’s private sector workforce — spanning IT services, manufacturing, retail, financial services, startups, and countless other industries — represents the largest segment of EPS members nationwide. Yet private sector employees often face a uniquely fragmented relationship with EPS: frequent job changes, payroll structures designed to minimise statutory contributions, and employers ranging from meticulous multinational corporations to under-resourced small businesses with inconsistent compliance.

This guide addresses the EPS pension considerations that are most relevant specifically to private sector employees — the practical realities that differ from a single-employer government career.

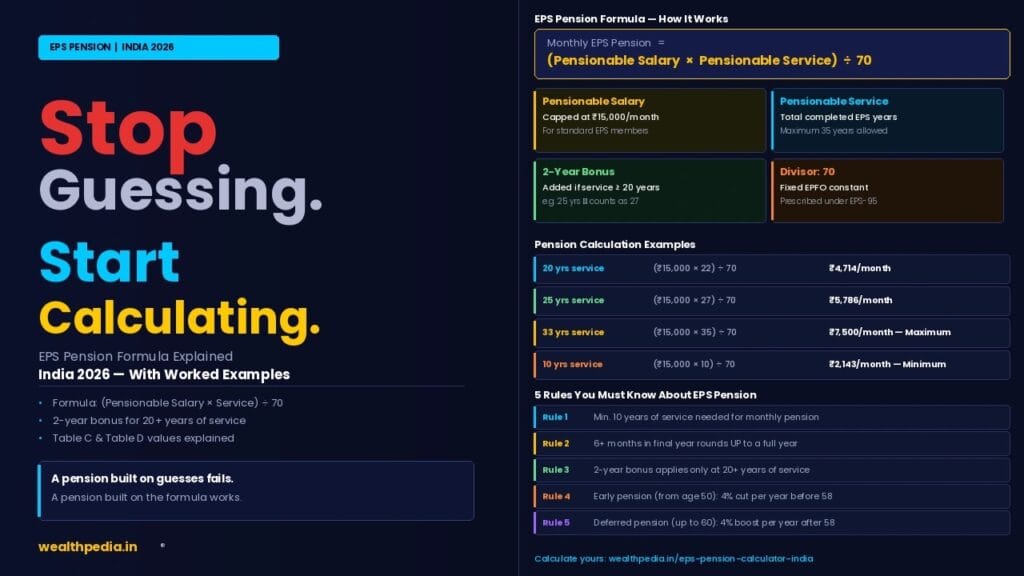

Use the EPS Pension Calculator India to compute your expected pension based on your actual employment history across multiple employers.

Quick Summary

Private sector employees form the overwhelming majority of EPS members in India, yet face unique challenges not always shared by public sector or PSU employees — frequent job changes, payroll structures with low basic salary, and limited awareness of EPS rules compared to EPF. This guide covers everything private sector employees need to know: how EPS membership works at private companies, the impact of job-hopping on pensionable service, why salary structuring matters, how startups and smaller companies handle EPS differently, and practical steps to maximise pension outcomes. Use the EPS Pension Calculator India to compute your expected pension based on your actual career.

Join Now →

EPS Eligibility for Private Sector Employees

Private sector employees are covered under EPS the same way as any other EPF-covered employee — through mandatory enrollment when joining an establishment covered under the EPF & Miscellaneous Provisions Act, 1952.

When Does a Private Company Need to Register for EPF/EPS?

- Establishments with 20 or more employees in scheduled industries are mandatorily covered

- Some establishments with fewer employees can voluntarily opt in

- Once registered, EPF/EPS coverage applies to nearly all employees (with limited exclusions for very high earners joining after a certain salary threshold)

Private Sector Employees Who Are NOT Covered

- Employees at very small establishments (under 20 employees) that have not voluntarily registered

- Contract workers whose contractor/principal employer has not registered them under EPF

- Employees explicitly categorised as “excluded employees” (typically those earning above ₹15,000 at the time of joining, who chose to opt out — though most employers still enrol them)

For the complete eligibility framework, see EPS Pension Eligibility Rules.

The Defining Private Sector Challenge — Job Mobility

Unlike government employees who often spend an entire career with one employer, private sector employees in India change jobs far more frequently — industry surveys consistently show average tenures of 2–4 years in sectors like IT, e-commerce, and startups.

This creates a critical EPS-specific risk: pensionable service can be lost or fragmented if not properly transferred between employers.

The Three Possible Outcomes at Each Job Change

Action Taken Effect on Pensionable Service UAN transfer completed (same UAN used at new employer) Service combines automatically — no action needed beyond ensuring transfer Scheme Certificate obtained and submitted to new employer Service preserved and combined manually No transfer, no Scheme Certificate, withdrawal taken (Form 10C) Service from that employer permanently forfeited

For private sector employees who change jobs 5, 6, or even 10 times across a career, ensuring every transition falls into one of the first two categories — never the third — is essential to accumulating meaningful pensionable service. See Scheme Certificate vs EPS Withdrawal for the complete decision framework.

Why Withdrawal Is Tempting But Often Costly

When leaving a job after a short stint (e.g., 2 years), many private sector employees are offered — and accept — the EPS withdrawal benefit (Table D) because it provides immediate cash. However, this permanently forfeits that period’s contribution toward the 10-year pension eligibility threshold and the 20-year bonus threshold.

Worked Example — The Cost of Fragmented Withdrawals

An employee works at 4 different private companies over a 22-year career:

- Company A: 5 years (withdrawal taken)

- Company B: 6 years (withdrawal taken)

- Company C: 7 years (UAN transferred)

- Company D: 4 years (current employer)

If withdrawals were taken at A and B: Only Company C + D service counts = 7 + 4 = 11 years pensionable service. Monthly Pension = (15,000 × 11) ÷ 70 = ₹2,357/month.

If all service had been preserved via UAN/Scheme Certificate: Total = 5 + 6 + 7 + 4 = 22 years. With 2-year bonus: 24 pensionable years. Monthly Pension = (15,000 × 24) ÷ 70 = ₹5,143/month.

The cost of the early withdrawals: ₹2,786/month for life — over ₹7.35 lakh in lost lifetime pension value over a 22-year retirement. This single decision pattern — taking small EPS withdrawals at each job change rather than preserving service — is likely the most financially damaging mistake private sector employees make regarding EPS.

Salary Structuring in Private Companies — The EPS Impact

Private sector companies, particularly in competitive industries, often structure compensation with a relatively low basic salary and high allowances (HRA, special allowance, performance pay) to optimise tax efficiency and reduce statutory contribution burden for both employer and employee.

The EPS Consequence

Since only basic salary + DA counts as pensionable salary (capped at ₹15,000), a low basic salary structure can directly reduce EPS pension for employees whose basic+DA falls below ₹15,000.

| Compensation Structure | Basic + DA | Pensionable Salary | Impact |

|---|---|---|---|

| High basic salary structure | ₹18,000 (CTC ₹40,000) | ₹15,000 (capped) | No EPS impact — already at ceiling |

| Low basic salary structure | ₹10,000 (CTC ₹40,000) | ₹10,000 (actual) | EPS pension reduced proportionally |

For employees whose basic+DA is already comfortably above ₹15,000, salary structuring has no effect on EPS (since the ceiling already applies). But for employees in lower salary bands — common in retail, BPO, junior roles, and many startup positions — a low basic salary structure can meaningfully reduce lifetime EPS pension.

For the complete breakdown of what counts as pensionable salary, see What Is Pensionable Salary Under EPS?

Startup and Small Company EPS Compliance Issues

Private sector employees at startups and smaller companies face a distinct risk: inconsistent or delayed EPF/EPS compliance.

Common Issues at Smaller Private Employers

- Delayed registration: Some startups delay EPF/EPS registration beyond the legally required employee threshold

- Irregular contributions: Cash flow issues at early-stage companies can lead to delayed or missed EPS contributions

- Incorrect salary reporting: Smaller companies with less sophisticated payroll systems sometimes misreport basic salary on ECR filings

How to Protect Yourself

- Verify EPF/EPS registration: Confirm your employer’s EPF establishment code and check that contributions are being made via the EPFO passbook portal (passbook.epfindia.gov.in)

- Check monthly contributions: Review your EPFO passbook every few months to ensure EPS contributions are being credited consistently

- Raise grievances promptly: If contributions are missing or incorrect, raise a complaint via EPFiGMS (epfigms.gov.in) as soon as possible — delays make it harder for EPFO to recover arrears from non-compliant employers

- Don’t assume — verify: Particularly at smaller companies, do not assume EPF/EPS deductions shown on your payslip have actually been deposited with EPFO; payslip deductions and actual EPFO deposits are not always the same thing

EPS Pension for Private Sector Employees Across Multiple Industries

IT and Technology Sector

Typically higher basic salaries (often already at or above ₹15,000), frequent job changes, generally good EPF/EPS compliance at established companies. The main risk is fragmented service from job-hopping without proper transfers.

Manufacturing and Industrial Sector

Often longer average tenures, more traditional payroll structures with clearer basic salary components, generally consistent compliance at established manufacturing companies, though smaller contract manufacturing units may have compliance gaps.

Retail and BPO Sector

Frequently lower basic salaries (sometimes below ₹15,000), higher employee turnover, and a higher proportion of contract or third-party payroll arrangements that require extra verification of EPF/EPS coverage.

Startups

Variable compliance quality depending on company maturity, often higher CTC with allowance-heavy structures, equity compensation that has no bearing on EPS (since EPS uses only basic+DA, not stock options or RSUs).

Financial Services

Generally strong compliance, often higher basic salaries, but can include variable pay structures (bonuses, commissions) that do not count toward pensionable salary regardless of how large they are relative to base pay.

How Private Sector Employees Can Maximise EPS Pension

Strategy 1 — Always Transfer, Never Withdraw (If Possible)

Whenever changing jobs, prioritise UAN transfer or Scheme Certificate over EPS withdrawal — even though the lump sum may be tempting. Preserving service compounds in value, particularly as you approach the 10-year and 20-year thresholds.

Strategy 2 — Track Your Cumulative Service Across Employers

Private sector employees with multiple employers should periodically check their EPFO passbook to confirm all service periods are correctly combined under a single UAN. Use the EPS Pension Calculator India to project your pension based on cumulative service.

Strategy 3 — Negotiate Basic Salary Structure (Where Possible)

For employees in lower salary bands, negotiating a higher basic salary component (even if total CTC remains the same) can improve EPS pension outcomes — though this also increases tax and EPF deductions, so the trade-off should be evaluated holistically.

Strategy 4 — Time Career Transitions Around Key Thresholds

If approaching the 10-year or 20-year (2-year bonus) thresholds, consider delaying a planned career break, sabbatical, or move to non-EPF-covered self-employment until after crossing the threshold. See EPS Pension After 20 Years for the detailed financial case.

Strategy 5 — Verify Employer Compliance Regularly

Particularly at smaller private companies, periodically check the EPFO passbook to ensure contributions are being made consistently and accurately.

Strategy 6 — Consider the Higher Pension Scheme If Eligible

If you were an EPFO member before November 1, 2022 and your employer was contributing on actual salary above ₹15,000, check whether your HPS application was processed. See EPS Higher Pension Scheme: Eligibility & Calculation for the complete eligibility framework.

Combined Retirement Planning for Private Sector Employees

Private sector employees typically need to plan retirement income from multiple sources, since EPS pension alone (capped at ₹7,500/month standard) is rarely sufficient for a comfortable retirement, particularly in higher cost-of-living cities.

A Balanced Private Sector Retirement Stack

Component Role EPS Pension Guaranteed floor income, inflation-resistant in nominal terms, but fixed EPF Corpus Capital for deployment — SWP, annuities, or emergency fund NPS (if opted) Additional market-linked retirement corpus with tax benefits Personal investments (mutual funds, equity, real estate) Growth and inflation-beating returns Health insurance Critical given no employer coverage post-retirement

For private sector employees building a comprehensive retirement plan, the Multi-Goal FIRE Planner and Financial Health Score tools can help model how EPS pension fits alongside other retirement assets.

Family Pension Considerations for Private Sector Employees

Family pension rules are identical for private sector employees as for any other EPS member — no minimum service requirement, with widow pension at 50% and child pension at 25% of the member’s pension. This is particularly important for private sector employees with fragmented careers, since family pension eligibility does not depend on having crossed the 10-year threshold.

See EPS Family Pension Rules Explained for the complete rules.

Frequently Asked Questions — EPS Pension for Private Sector Employees

Are private sector employees eligible for EPS pension?

Yes. Private sector employees at EPF-covered establishments (generally 20+ employees) are eligible for EPS the same way as any other employee, provided their basic+DA was ₹15,000 or below at the time of joining (or they were enrolled before crossing this threshold).

How does job-hopping affect EPS pension for private sector employees?

If EPS service is properly transferred (via UAN) or preserved (via Scheme Certificate) at each job change, it combines cumulatively across all employers. If withdrawal benefit (Form 10C) is taken at any point, that period’s service is permanently forfeited. Frequent job changes without proper transfers can significantly reduce lifetime pension.

Why is my EPS pension lower than expected despite a high salary?

Standard EPS pension is capped at the ₹15,000 wage ceiling regardless of actual salary. If your basic+DA exceeds ₹15,000, your EPS pension is identical to someone earning exactly ₹15,000 with the same service years — your higher salary contributes to a larger EPF corpus, not a higher EPS pension (unless you are HPS-approved).

What should I do when leaving a private sector job after only 3-4 years?

Strongly consider obtaining a Scheme Certificate (via Form 10C) rather than taking the EPS withdrawal benefit, especially if you plan to continue in EPF-covered employment. This preserves your service for combination with your next employer, working toward the 10-year and 20-year thresholds. See Scheme Certificate vs EPS Withdrawal.

Do startups have to register for EPF/EPS?

Yes, once they reach 20 or more employees (in most scheduled industries), EPF/EPS registration is mandatory. Some startups voluntarily register earlier. Employees should verify their employer’s registration status and check the EPFO passbook regularly, since smaller companies sometimes have compliance gaps.

How can I check if my private employer is making EPS contributions correctly?

Log in to the EPFO Member Portal at passbook.epfindia.gov.in with your UAN. The EPS contribution column shows monthly credits. If contributions appear missing, delayed, or incorrect, raise a grievance via EPFiGMS at epfigms.gov.in.

Does a low basic salary structure at my private company reduce my EPS pension?

Yes — if your basic+DA is below ₹15,000, a lower basic salary directly reduces your pensionable salary and therefore your EPS pension. If your basic+DA already exceeds ₹15,000, further reductions in basic (relative to allowances) have no EPS impact since the ceiling already applies.

Is EPS pension enough for retirement for a private sector employee?

Generally not on its own. Standard EPS pension (maximum ₹7,500/month) is best viewed as a guaranteed floor income, to be combined with EPF corpus, personal investments, and potentially NPS for a complete retirement plan. See EPF vs EPS: Key Differences Explained and use the Multi-Goal FIRE Planner for comprehensive planning.

What happens to EPS pension if my private company shuts down?

Your accumulated EPS service is preserved regardless of the company’s status — it remains on record under your UAN. If the company failed to update your exit date in EPFO records before shutting down, raise a grievance via EPFiGMS with supporting documents (resignation letter, salary slips) to have your exit date administratively updated, then proceed with your pension claim as usual.

Can I combine EPS service from a private sector job with a later government job?

If the government role is also EPF-covered (such as certain PSUs), service can combine via UAN transfer. If the government role follows a separate pension scheme (such as the old pension scheme or NPS for most government positions), it does not combine with EPS — your EPS service remains frozen at whatever you accumulated during private sector employment, claimable from the eligible age.

Where can I calculate my expected EPS pension as a private sector employee with multiple employers?

Use the EPS Pension Calculator India on Wealthpedia. Enter your total combined service across all employers (verified via your EPFO passbook) along with your pensionable salary to get an accurate pension projection, including the 2-year bonus and rounding rules.

Disclaimer: The information on this page is for educational purposes only and does not constitute investment or financial advice. EPS rules are governed by EPFO regulations under EPS-95 and may be updated by the Government of India. For personalised guidance, consult a SEBI-registered financial planner or visit your nearest EPFO office. Wealthpedia™ (Trademark Reg. No. 4910385) is not a SEBI-registered investment advisor. All mutual fund references on this site are for Direct Plan, Growth option only.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up