If you have ever typed “how much EPS pension will I get” into a search engine, you have probably found the formula but not a clear worked example for your specific service years and salary. This article fixes that. Every major scenario is calculated step by step — from someone with just 10 years of service to someone with a full 33-year career, plus early claimers, late claimers, and Higher Pension Scheme members.

All calculations on this page use the official EPFO formula and Table C values. You can verify every figure using the EPS Pension Calculator India, which applies the same logic automatically and also handles partial years, the 2-year service bonus, and inflation-adjusted lifetime value projections.

Quick Summary

Using the EPS pension formula — (Pensionable Salary × Pensionable Service) ÷ 70 — this article walks through real calculation examples for every major scenario Indian employees face: 10, 15, 20, 25, 30, and 33 years of service at the ₹15,000 wage ceiling, lower-salary cases, early pension claimed at 50–57, deferred pension claimed at 59–60, and the Higher Pension Scheme. Each example shows the exact inputs, formula steps, and final monthly pension figure. Use the EPS Pension Calculator India to instantly compute your own estimate with all EPFO rules — including Table C/D adjustments — built in.

The EPS Pension Formula — A Quick Recap

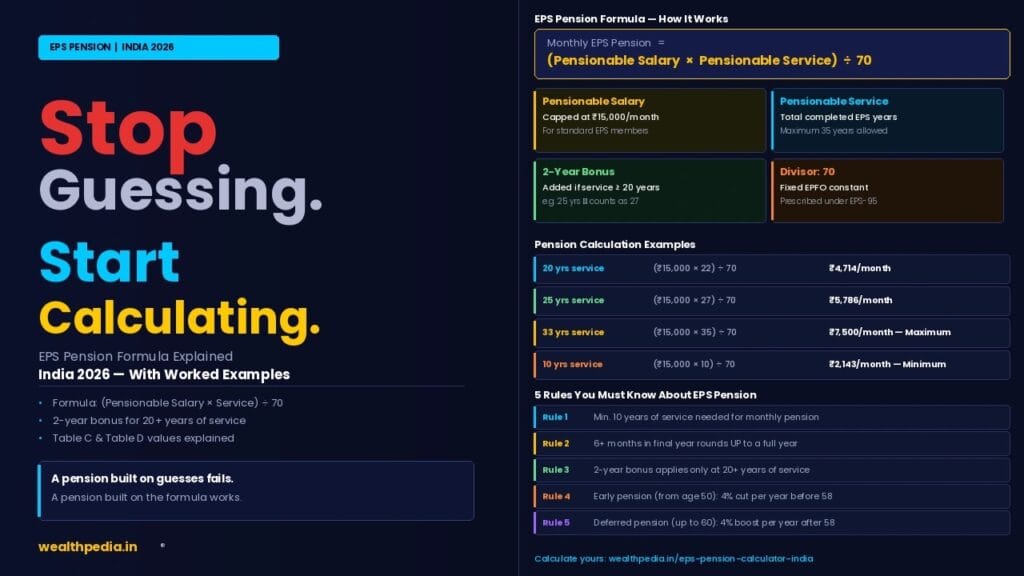

Before the examples, here is the formula every calculation on this page uses:

Monthly EPS Pension = (Pensionable Salary × Pensionable Service) ÷ 70

Three rules to remember before plugging in numbers:

- Pensionable Salary is capped at ₹15,000/month for most employees (or your actual salary if below ₹15,000)

- Pensionable Service is counted in completed years — 6+ months in the final year rounds up; under 6 months is dropped

- If total service reaches 20 years or more, EPFO adds a 2-year bonus before applying the formula

- Maximum pensionable service EPFO recognises is 35 years

For a complete breakdown of every component, see the EPS Pension Formula Explained guide.

EPS Pension Calculator Example — Standard Scenarios at ₹15,000 Salary

The majority of Indian salaried employees have a basic + DA at or above ₹15,000, which means their pensionable salary is capped at the EPFO wage ceiling. The examples below cover every major service milestone.

Example 1 — EPS Pension After 10 Years of Service

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 10 years

- 2-Year Bonus: No (service below 20 years)

- Pensionable Service used in formula: 10 years

Calculation:

(15,000 × 10) ÷ 70 = ₹2,143/month

This is the minimum qualifying pension for a ₹15,000-salary employee. 10 years is also the minimum service threshold — below this, EPFO pays a withdrawal benefit (Table D) instead of monthly pension. For a full breakdown of this scenario, see How Much EPS Pension Will I Get After 10 Years?

Example 2 — EPS Pension After 15 Years of Service

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 15 years

- 2-Year Bonus: No (service below 20 years)

- Pensionable Service used in formula: 15 years

Calculation:

(15,000 × 15) ÷ 70 = ₹3,214/month

15 years of service gives a meaningfully higher pension than the 10-year minimum, but note that the 2-year bonus has not kicked in yet. Those last 5 years to 20 are especially valuable — crossing 20 years adds 2 bonus years on top. Full details in EPS Pension After 15 Years Service.

Example 3 — EPS Pension After 20 Years of Service

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 20 years

- 2-Year Bonus: Yes (service equals 20 years — bonus applies)

- Pensionable Service used in formula: 22 years

Calculation:

(15,000 × 22) ÷ 70 = ₹4,714/month

The jump from 15 years (₹3,214) to 20 years (₹4,714) is ₹1,500/month — 5 additional years of actual service but 7 additional years in the formula thanks to the 2-year bonus. This is why financial planners in India consistently advise employees to push through to 20 years of EPF-covered service before considering a career break or early retirement. See EPS Pension After 20 Years for the full analysis.

Example 4 — EPS Pension After 25 Years of Service

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 25 years

- 2-Year Bonus: Yes

- Pensionable Service used in formula: 27 years

Calculation:

(15,000 × 27) ÷ 70 = ₹5,786/month

At 25 years, you are already in the upper tier of EPS pension recipients. The monthly pension of ₹5,786 is nearly 80% of the maximum. Full example in EPS Pension After 25 Years Service.

Example 5 — EPS Pension After 30 Years of Service

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 30 years

- 2-Year Bonus: Yes

- Pensionable Service used in formula: 32 years

Calculation:

(15,000 × 32) ÷ 70 = ₹6,857/month

30 years of service takes you to ₹6,857/month — just ₹643 short of the maximum. See EPS Pension After 30 Years for a full retirement income projection combining this with your EPF corpus.

Example 6 — EPS Pension After 33 Years of Service (Maximum)

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 33 years

- 2-Year Bonus: Yes

- Pensionable Service used in formula: 35 years (maximum — capped here)

Calculation:

(15,000 × 35) ÷ 70 = ₹7,500/month

This is the maximum monthly EPS pension under the standard formula. Any service beyond 33 years does not increase the pension further since 35 years is the EPFO cap. Full details in EPS Pension After 35 Years Service.

Summary Table — Standard Calculations at ₹15,000 Salary

| Actual Service Years | Pensionable Service (after bonus) | Monthly EPS Pension |

|---|---|---|

| 10 | 10 | ₹2,143 |

| 15 | 15 | ₹3,214 |

| 20 | 22 (+2 bonus) | ₹4,714 |

| 25 | 27 (+2 bonus) | ₹5,786 |

| 30 | 32 (+2 bonus) | ₹6,857 |

| 33 | 35 (+2 bonus, capped) | ₹7,500 |

Use the EPS Pension Calculator India to compute results for any other service year in between.

EPS Pension Calculator Example — Below ₹15,000 Salary

Not all EPF-covered employees earn above the ₹15,000 ceiling. For them, the actual salary is used as pensionable salary.

Example 7 — ₹8,000 Salary, 20 Years Service

Inputs:

- Pensionable Salary: ₹8,000 (actual salary below ceiling)

- Actual Service: 20 years

- 2-Year Bonus: Yes

- Pensionable Service used in formula: 22 years

Calculation:

(8,000 × 22) ÷ 70 = ₹2,514/month

Even with the 2-year bonus, a lower pensionable salary produces a significantly lower pension. This demonstrates the importance of understanding that EPS pension is not just about years of service — the salary component matters equally.

Example 8 — ₹12,000 Salary, 25 Years Service

Inputs:

- Pensionable Salary: ₹12,000

- Actual Service: 25 years

- 2-Year Bonus: Yes

- Pensionable Service used in formula: 27 years

Calculation:

(12,000 × 27) ÷ 70 = ₹4,629/month

Example 9 — ₹10,000 Salary, 15 Years Service

Inputs:

- Pensionable Salary: ₹10,000

- Actual Service: 15 years

- 2-Year Bonus: No

- Pensionable Service used in formula: 15 years

Calculation:

(10,000 × 15) ÷ 70 = ₹2,143/month

Note that this gives the same pension as Example 1 (₹15,000 salary, 10 years) because the formula treats the two variables symmetrically — a higher salary partially compensates for shorter service and vice versa.

EPS Pension Calculator Example — Partial Year Rounding

Example 10 — ₹15,000 Salary, 22 Years and 8 Months Service

EPFO rounding rule: 8 months > 6 months → rounds up to 1 full year.

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 22 years + 8 months → counted as 23 years

- 2-Year Bonus: Yes (service ≥ 20 years)

- Pensionable Service used in formula: 25 years

Calculation:

(15,000 × 25) ÷ 70 = ₹5,357/month

Example 11 — ₹15,000 Salary, 22 Years and 4 Months Service

EPFO rounding rule: 4 months < 6 months → dropped.

Inputs:

- Pensionable Salary: ₹15,000

- Actual Service: 22 years + 4 months → counted as 22 years

- 2-Year Bonus: Yes

- Pensionable Service used in formula: 24 years

Calculation:

(15,000 × 24) ÷ 70 = ₹5,143/month

The difference between 4 months and 8 months in your final year of service is ₹214/month for life — over 20 years of retirement, that is over ₹51,000. This is why timing your EPF exit to avoid dropping a partial year matters.

EPS Pension Calculator Example — Early Pension (Before Age 58)

EPS allows pension claims from age 50, but applies a 4% per year reduction for every year before 58. The base pension is first calculated using the standard formula, then the early pension reduction is applied.

Example 12 — Claiming at Age 56 (2 Years Early)

Inputs:

- Pensionable Salary: ₹15,000

- Service: 25 years → Pensionable Service: 27 years

- Base Pension = (15,000 × 27) ÷ 70 = ₹5,786/month

- Years before 58: 2

- Reduction: 2 × 4% = 8%

Early Pension:

₹5,786 × (1 − 0.08) = ₹5,786 × 0.92 = ₹5,323/month

Lifetime cost of claiming 2 years early: assuming 25 years of retirement, the total reduction versus waiting until 58 is approximately ₹1,38,000.

Example 13 — Claiming at Age 53 (5 Years Early)

Inputs:

- Base Pension: ₹5,786/month (same as above)

- Years before 58: 5

- Reduction: 5 × 4% = 20%

Early Pension:

₹5,786 × 0.80 = ₹4,629/month

Example 14 — Claiming at Age 50 (8 Years Early, Maximum Early Claim)

Inputs:

- Base Pension: ₹5,786/month

- Years before 58: 8

- Reduction: 8 × 4% = 32%

Early Pension:

₹5,786 × 0.68 = ₹3,934/month

Claiming at 50 instead of 58 permanently reduces your pension by nearly one-third. This is a significant decision — see EPS Early Pension Before 58: Reduction Rules Explained for a full break-even analysis before making this choice.

Early Pension Summary Table (Base Pension ₹5,786/month)

| Claim Age | Years Before 58 | Reduction | Monthly Pension |

|---|---|---|---|

| 58 | 0 | 0% | ₹5,786 |

| 57 | 1 | 4% | ₹5,554 |

| 56 | 2 | 8% | ₹5,323 |

| 55 | 3 | 12% | ₹5,091 |

| 54 | 4 | 16% | ₹4,860 |

| 53 | 5 | 20% | ₹4,629 |

| 52 | 6 | 24% | ₹4,397 |

| 51 | 7 | 28% | ₹4,166 |

| 50 | 8 | 32% | ₹3,934 |

EPS Pension Calculator Example — Deferred Pension (After Age 58)

If you continue working beyond 58 or simply delay filing your pension claim, EPFO increases your pension by 4% for each year of deferment, up to a maximum of age 60.

Example 15 — Claiming at Age 59 (1 Year Deferred)

Inputs:

- Base Pension: ₹5,786/month

- Years after 58: 1

- Enhancement: 1 × 4% = 4%

Deferred Pension:

₹5,786 × 1.04 = ₹6,017/month

Example 16 — Claiming at Age 60 (2 Years Deferred, Maximum)

Inputs:

- Base Pension: ₹5,786/month

- Years after 58: 2

- Enhancement: 2 × 4% = 8%

Deferred Pension:

₹5,786 × 1.08 = ₹6,249/month

Waiting just 2 extra years after 58 permanently boosts your monthly pension by ₹463. Over 20 years of retirement that is an additional ₹1,11,000. See Deferred EPS Pension After 58: Benefits Explained for the full break-even and cash-flow analysis.

EPS Pension Calculator Example — Higher Pension Scheme Members

For employees who successfully applied for and received EPFO approval under the Higher Pension Scheme, the pensionable salary in the formula is replaced by the average actual basic + DA over the last 60 months before retirement. The formula structure is otherwise identical.

Example 17 — ₹40,000 Average Salary, 25 Years Service

Inputs:

- Pensionable Salary: ₹40,000 (actual 60-month average — Higher Pension opted)

- Actual Service: 25 years

- 2-Year Bonus: Yes

- Pensionable Service: 27 years

Calculation:

(40,000 × 27) ÷ 70 = ₹15,429/month

Compared to ₹5,786/month under the standard formula — the Higher Pension Scheme adds ₹9,643/month for the same service length. See EPS Higher Pension Scheme: Eligibility & Calculation for the full opt-in process and cost calculation.

Example 18 — ₹60,000 Average Salary, 30 Years Service

Inputs:

- Pensionable Salary: ₹60,000

- Actual Service: 30 years

- 2-Year Bonus: Yes

- Pensionable Service: 32 years

Calculation:

(60,000 × 32) ÷ 70 = ₹27,429/month

This is approximately 3.7× the maximum standard EPS pension of ₹7,500/month.

Example 19 — ₹80,000 Average Salary, 33 Years Service

Inputs:

- Pensionable Salary: ₹80,000

- Actual Service: 33 years

- 2-Year Bonus: Yes

- Pensionable Service: 35 years (capped)

Calculation:

(80,000 × 35) ÷ 70 = ₹40,000/month

Under the Higher Pension Scheme, there is no salary cap — so high-earning, long-tenure employees can receive a pension well beyond ₹7,500/month. However, the trade-off is a significant lump-sum deposit to EPFO for the contribution shortfall on the higher salary over all past years, including interest.

EPS Pension Calculator Example — Table D Withdrawal (Under 10 Years)

For members who have not yet completed 10 years of EPS-covered service, EPFO pays a lump-sum withdrawal benefit calculated using Table D factors, not the monthly pension formula.

Example 20 — 5 Years Service, ₹15,000 Salary

Table D Factor at 5 years: 5.28

Withdrawal Benefit = 5.28 × ₹15,000 = ₹79,200

Example 21 — 7 Years Service, ₹15,000 Salary

Table D Factor at 7 years: 7.46

Withdrawal Benefit = 7.46 × ₹15,000 = ₹1,11,900

Example 22 — 9 Years Service, ₹15,000 Salary

Table D Factor at 9 years: 9.72

Withdrawal Benefit = 9.72 × ₹15,000 = ₹1,45,800

Note: At 9 years and 6+ months, EPFO rounds up to 10 years — making this person eligible for monthly pension instead of the withdrawal benefit. Timing the exit carefully around this threshold can significantly affect lifetime retirement income.

The EPS Withdrawal Benefit Calculator gives you the exact Table D figure for any service year. If you are torn between withdrawing and preserving your service, the Scheme Certificate vs EPS Withdrawal comparison will help you decide.

How to Use the EPS Pension Calculator India

The EPS Pension Calculator India on Wealthpedia is built on the same EPFO formula and Table C/D values used throughout this article. Here is what you need to enter and what it outputs:

What You Input

- Date of birth — used to calculate current age and pension start age

- Date of joining EPS — starting point for pensionable service calculation

- Expected retirement date — used to compute final pensionable service

- Monthly pensionable salary — enter your basic + DA (the calculator caps at ₹15,000 automatically unless you select Higher Pension)

- Higher Pension opted? — toggle Yes/No

- Desired pension start age — between 50 and 60

What You Get

- Monthly pension at your chosen start age

- Comparison of pension at 50, 55, 58, 59, and 60

- Table D withdrawal benefit if your service is under 10 years

- Inflation-adjusted lifetime pension value (total pension income assuming 6% inflation and life expectancy of 80)

- Visual Chart.js graphs showing pension trajectory

The calculator auto-applies the 2-year service bonus, partial-year rounding, and the 4%/year early or deferred pension adjustment — no manual calculation required.

Side-by-Side Comparison — All Scenarios at a Glance

| Scenario | Pensionable Salary | Actual Service | Pensionable Service | Monthly Pension |

|---|---|---|---|---|

| 10 yrs, standard | ₹15,000 | 10 | 10 | ₹2,143 |

| 15 yrs, standard | ₹15,000 | 15 | 15 | ₹3,214 |

| 20 yrs, standard | ₹15,000 | 20 | 22 | ₹4,714 |

| 25 yrs, standard | ₹15,000 | 25 | 27 | ₹5,786 |

| 30 yrs, standard | ₹15,000 | 30 | 32 | ₹6,857 |

| 33 yrs, standard (max) | ₹15,000 | 33 | 35 | ₹7,500 |

| 20 yrs, ₹8,000 salary | ₹8,000 | 20 | 22 | ₹2,514 |

| 25 yrs, claimed at 56 | ₹15,000 | 25 | 27 | ₹5,323 |

| 25 yrs, claimed at 50 | ₹15,000 | 25 | 27 | ₹3,934 |

| 25 yrs, claimed at 60 | ₹15,000 | 25 | 27 | ₹6,249 |

| 25 yrs, Higher Pension | ₹40,000 | 25 | 27 | ₹15,429 |

| 30 yrs, Higher Pension | ₹60,000 | 30 | 32 | ₹27,429 |

Key Takeaways from These Examples

Crossing 20 years is the single biggest milestone. The 2-year bonus means your pensionable service jumps from 19 to 22 in one step — a 3-year gain in the formula for just 1 year of additional actual service.

Early pension has a permanent, compounding cost. Claiming at 50 instead of 58 reduces your pension by 32% for life. Unless you have a compelling reason (health, financial distress), waiting until 58 or beyond is almost always financially superior.

The Higher Pension Scheme changes the arithmetic entirely. For employees who qualify, the pension can be 3–5× the standard amount — but requires careful cost-benefit analysis of the lump-sum contribution required.

Partial-year timing matters near the 6-month boundary. If you are 1–2 months away from crossing the 6-month threshold in your final year, staying on can add a full year to your pensionable service — worth hundreds of rupees per month for life.

Table D withdrawal forfeits lifetime pension income. Withdrawing at 7 years gives you ₹1,11,900 today. Waiting until 10 years gives you ₹2,143/month for life — break-even in about 4.4 years of retirement. The math almost always favours patience.

Frequently Asked Questions — EPS Pension Calculator Examples

How is EPS pension calculated with an example?

EPS pension is calculated using the formula: Monthly Pension = (Pensionable Salary × Pensionable Service) ÷ 70. For example, an employee with ₹15,000 pensionable salary and 25 years of service gets: (15,000 × 27) ÷ 70 = ₹5,786/month (27 years because the 2-year bonus applies for 20+ years of service).

What is the EPS pension for 20 years of service?

With ₹15,000 pensionable salary and 20 years of service, the EPS pension is ₹4,714/month. The calculation is: 20 years + 2-year bonus = 22 years; (15,000 × 22) ÷ 70 = ₹4,714. Use the EPS Pension Calculator to verify this instantly.

What is the maximum EPS pension in India?

The maximum monthly EPS pension under the standard formula is ₹7,500/month, achieved with 33+ years of service at the ₹15,000 wage ceiling: (15,000 × 35) ÷ 70 = ₹7,500. Under the Higher Pension Scheme, the ceiling is effectively removed — high-salary employees can receive ₹30,000–₹40,000+/month or more.

How much EPS pension will I get after 15 years?

With ₹15,000 pensionable salary and 15 years of service (no 2-year bonus since service is below 20 years): Monthly Pension = (15,000 × 15) ÷ 70 = ₹3,214/month. For a full breakdown, see EPS Pension After 15 Years Service.

Does EPS pension calculator use Table C values?

Yes. The EPS Pension Calculator India uses EPFO’s Table C values, which are the pre-computed pension amounts for each combination of pensionable salary and pensionable service (with the 2-year bonus applied). The formula and Table C values produce identical results.

How is early EPS pension calculated?

Early pension is calculated by first computing the base pension using the standard formula, then reducing it by 4% for each year the claim is made before age 58. Formula: Early Pension = Base Pension × (1 − 0.04 × years before 58). For example, claiming at 55 (3 years early): Base Pension × 0.88.

Can I use an EPS pension calculator for the Higher Pension Scheme?

Yes. The EPS Pension Calculator India has a Higher Pension Scheme toggle. When enabled, you enter your actual average pensionable salary (instead of the ₹15,000 default), and the calculator applies the formula to that higher salary. See EPS Higher Pension Scheme Explained for who qualifies.

What happens to EPS pension if I worked for two companies?

Your pensionable service from both companies is combined, provided you transferred your EPF/EPS account via UAN when switching jobs. The cumulative service is used in the formula. If you did not transfer, the two service spells may be treated separately, potentially affecting eligibility for the 2-year bonus or the 10-year minimum.

Is EPS pension calculated on basic salary or gross salary?

EPS pension is calculated on basic salary + Dearness Allowance (DA), not on gross salary. Allowances like HRA, conveyance, and special pay are excluded. The pensionable salary is then capped at ₹15,000 (unless you are under the Higher Pension Scheme).

How do I calculate my EPS pension if my salary changed over the years?

EPFO uses the last drawn pensionable salary (subject to the ₹15,000 ceiling) — not a career average — for the standard pension formula. So only your salary at the time of retirement matters for pensionable salary. For the Higher Pension Scheme, the average of the last 60 months is used. The EPS Pension Calculator handles both methods.

What is the EPS pension for ₹15,000 salary after 30 years?

Pensionable Salary = ₹15,000. Actual Service = 30 years. 2-year bonus applies → Pensionable Service = 32 years. Monthly Pension = (15,000 × 32) ÷ 70 = ₹6,857/month. Full details in EPS Pension After 30 Years.

Is EPS pension the same as EPF corpus?

No. EPS and EPF are two separate funds under EPFO. EPS gives a monthly pension for life based on the formula; EPF accumulates a lump-sum corpus (your contributions + employer EPF contribution + interest) paid at retirement. The EPS formula has no bearing on your EPF balance and vice versa. See EPF vs EPS Explained for the full comparison.

Can I get both EPF lump sum and EPS pension at retirement?

Yes. At retirement, you receive your full EPF corpus (employee + employer EPF contributions + accumulated interest) as a lump sum, and separately you receive monthly EPS pension for life. These are independent — receiving one does not reduce the other.

What is the EPS pension for ₹15,000 salary with 33 years of service?

Pensionable Service = 33 + 2 bonus = 35 years (maximum). Monthly Pension = (15,000 × 35) ÷ 70 = ₹7,500/month. This is the maximum achievable pension under the standard EPS formula. See EPS Pension After 35 Years Service.

How much pension does an EPS member get if they claim at 60?

Claiming at 60 (2 years after the normal pension age of 58) increases the pension by 8%. Formula: Deferred Pension = Base Pension × 1.08. Example: Base Pension ₹5,786 → Deferred Pension = ₹5,786 × 1.08 = ₹6,249/month. See Deferred EPS Pension After 58.

Is there an online tool to calculate EPS pension?

Yes. The EPS Pension Calculator India on Wealthpedia is free to use and covers all scenarios — standard pension, early pension, deferred pension, Higher Pension Scheme, and Table D withdrawal benefit — with EPFO rules built in.

What is the EPS pension for 10 years and ₹10,000 salary?

Pensionable Salary = ₹10,000 (below ₹15,000 ceiling, actual salary used). Pensionable Service = 10 years (no bonus). Monthly Pension = (10,000 × 10) ÷ 70 = ₹1,429/month. Since this is below the EPFO minimum pension of ₹1,000/month, the government floor applies and the member receives ₹1,429/month.

Does the EPS pension formula change after the 2024 EPFO update?

The core EPS pension formula — (Pensionable Salary × Pensionable Service) ÷ 70 — has remained unchanged under EPS-95. The significant recent development was the Supreme Court ruling on the Higher Pension Scheme in 2022–23, which affected how pensionable salary is calculated for opted-in members. The EPS Pension Rules 2026 article covers the latest applicable rules.

How do I verify my EPS pension calculation against EPFO records?

Log into the EPFO Member Portal at passbook.epfindia.gov.in with your UAN. Check the EPS contribution column in your passbook to verify your total EPS-covered service months and pensionable salary history. Cross-check using the EPS Pension Calculator India.

What is the EPS pension for someone retiring at 58 with 28 years of service?

Actual Service = 28 years. 2-year bonus applies → Pensionable Service = 30 years. Pensionable Salary = ₹15,000. Monthly Pension = (15,000 × 30) ÷ 70 = ₹6,429/month.

Why does EPS pension not increase beyond ₹7,500?

Under the standard formula, both the pensionable salary (capped at ₹15,000) and the maximum pensionable service (capped at 35 years) are fixed. So the theoretical maximum is (15,000 × 35) ÷ 70 = ₹7,500. Service beyond 33 years adds no further pension because the 35-year cap is already reached at 33 years after the 2-year bonus. The only way to exceed ₹7,500 is via the Higher Pension Scheme.

Is the EPS pension calculation different for employees who joined before 2014?

The formula is the same. However, the pensionable salary ceiling was ₹6,500 before September 2014 and ₹15,000 thereafter. For employees who joined before 2014 and retired after 2014, EPFO applies the ₹15,000 ceiling to the current salary (or actual salary if below ₹15,000) as the pensionable salary — not a blended average of the pre- and post-2014 ceilings.

How is pensionable service calculated if I took a break of 3 years mid-career?

A 3-year break in EPS contributions is generally not condonable under EPFO rules (breaks up to 2 years may be condoned in some cases). The service before and after the break would be counted separately. If the pre-break service was under 10 years and you had not obtained a Scheme Certificate, that earlier spell may be lost for pension purposes. See Scheme Certificate vs EPS Withdrawal for options if you have a career gap.

What does the EPS pension calculator show for someone with 19 years and 8 months of service?

EPFO rounding: 8 months > 6 months → rounds up to 1 full year. So 19 years and 8 months counts as 20 years of pensionable service. The 2-year bonus then applies → Pensionable Service = 22 years. Monthly Pension = (15,000 × 22) ÷ 70 = ₹4,714/month. This is a critical data point — if you have 19+ years, staying until the 6-month mark in year 20 could unlock the full 2-year bonus.

What is the lifetime pension value from EPS?

Lifetime pension value depends on your monthly pension amount and how long you live post-retirement. At ₹5,786/month (25 years service, claimed at 58), over 22 years of retirement (life expectancy 80) the total nominal pension received is approximately ₹15.27 lakh. Adjusted for 6% inflation, the present value is considerably lower — but the pension’s value as an inflation-stable guaranteed income stream is its primary advantage over a lump sum. The EPS Pension Calculator India computes lifetime value with inflation adjustment automatically.

Disclaimer: The information on this page is for educational purposes only and does not constitute investment or financial advice. EPS rules are governed by EPFO regulations and may be updated by the Government of India. All calculations on this page use the standard EPS-95 formula and EPFO Table C/D values as of 2026. For personalised guidance, consult a SEBI-registered financial planner or visit your nearest EPFO office. Wealthpedia™ (Trademark Reg. No. 4910385) is not a SEBI-registered investment advisor. All mutual fund references on this site are for Direct Plan, Growth option only.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up