Widow pension is one of the most important — and most under-claimed — benefits under the Employees’ Pension Scheme. Many widows of EPS members are unaware they are entitled to a lifetime monthly pension, separate from any EPF corpus their late husband may have accumulated. This guide provides a complete, dedicated explanation of every rule governing widow pension under EPS-95.

Use the EPS Pension Calculator India to estimate the member’s underlying pension, which forms the basis of the 50% widow pension calculation.

Quick Summary

Widow pension under EPS provides the surviving spouse of a deceased EPS member with 50% of the member’s monthly pension for life, or until remarriage. There is no minimum service requirement — even a member who worked just one day in EPS-covered employment qualifies their widow for this benefit. The minimum guaranteed widow pension is ₹1,000/month. This article covers complete eligibility rules, the exact calculation methodology, what happens if the member had claimed early or deferred pension, the remarriage rule, required documents, and the step-by-step claim process. Use the EPS Pension Calculator India to estimate the underlying member pension that determines the widow pension amount.

Join Now →

What Is Widow Pension Under EPS?

Widow pension is a monthly survivor benefit paid by EPFO to the legally married surviving spouse of a deceased EPS member, equal to 50% of the member’s pension, payable for the widow’s lifetime or until remarriage.

This benefit applies regardless of:

- How many years the deceased member had worked

- Whether the member had already started drawing pension or died while still in service

- The widow’s own age, income, or financial status

Widow Pension Eligibility — Who Qualifies?

To qualify for widow pension under EPS, the following conditions must be met:

Condition 1 — Legal Marriage

The claimant must have been the legally married spouse of the deceased EPS member at the time of death. EPS-95 does not currently recognise common-law partnerships or live-in relationships for widow pension purposes.

Condition 2 — Member Was an EPS Contributor

The deceased husband must have been an EPS member — meaning EPS contributions were made on his behalf during his employment, even briefly. There is no minimum service requirement for widow pension eligibility.

Condition 3 — Death Occurred During Membership or While Drawing Pension

Widow pension applies in three scenarios:

- The member died while in active EPF-covered service (regardless of tenure)

- The member died after retirement, while already drawing monthly pension

- The member had left service with 10+ years of pensionable service but died before claiming pension (before reaching the eligible age or before filing Form 10D)

For the complete eligibility framework across all EPS benefits, see EPS Pension Eligibility Rules.

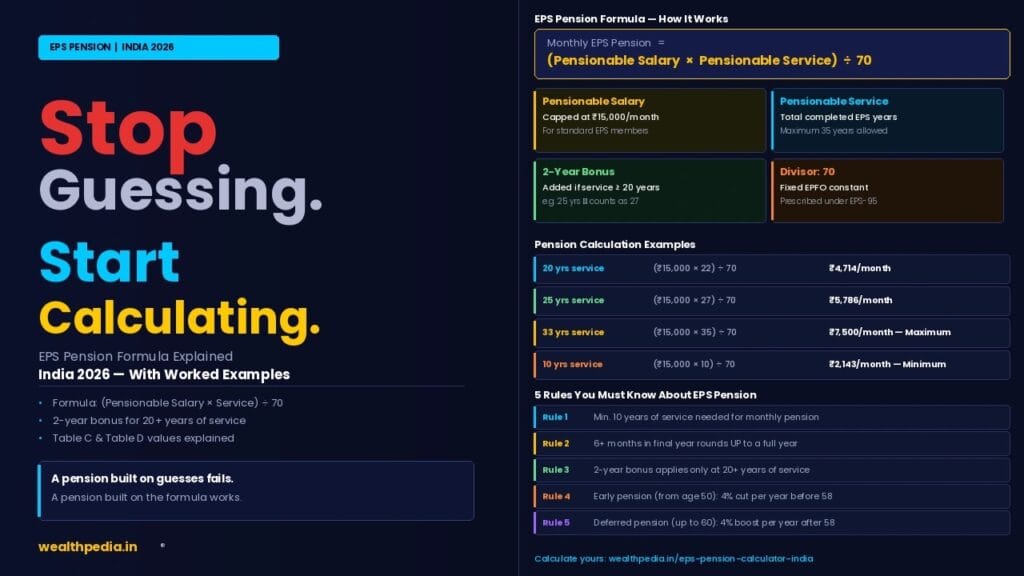

How Widow Pension Is Calculated

Widow Pension = 50% of the Member’s Monthly Pension

The “member’s pension” used in this calculation depends on the scenario: Scenario Member’s Pension Used for 50% Calculation Member died while in active service Notional pension based on actual service (or 2-year minimum notional service if actual service was shorter), using salary at time of death Member died after starting to draw pension The actual sanctioned pension amount (including any early/deferred adjustment) Member died after 10+ years service but before claiming Standard pension calculated based on service and salary at exit, as if claimed at the appropriate age

Worked Example 1 — Member Died While Drawing Standard Pension

- Member’s pension: ₹5,786/month (25 years service, ₹15,000 salary, claimed at 58)

- Widow Pension = 50% × ₹5,786 = ₹2,893/month

Worked Example 2 — Member Died While in Active Service (Short Tenure)

- Member’s actual service at death: 4 years

- EPFO applies a notional minimum of 2 years for calculation if actual service is shorter — but since 4 years > 2 years, actual service (4 years) is used

- Notional pension = (15,000 × 4) ÷ 70 = ₹857/month → floor applies → ₹1,000/month

- Widow Pension = 50% × ₹1,000 = ₹500/month → floor applies → ₹1,000/month (the ₹1,000 minimum floor applies independently to the widow pension itself)

Worked Example 3 — Member Had Claimed Early Pension Before Death

- Member claimed early pension at age 52 (24% reduction applied)

- Base pension (would have been at 58): ₹5,786/month

- Early pension actually drawn: ₹5,786 × 0.76 = ₹4,397/month

- Widow Pension = 50% × ₹4,397 = ₹2,199/month (not 50% of the un-reduced ₹5,786 base)

This last example illustrates a critical point: if the member claimed early pension with a reduction, the widow pension is calculated on the reduced amount — not the original, un-reduced base pension. This is an important consideration for members deciding whether to claim early pension, particularly if their spouse is significantly younger and likely to outlive them by a wide margin.

Worked Example 4 — Member Had Deferred Pension Before Death

- Member deferred pension to age 60 (8% enhancement applied)

- Base pension: ₹5,786/month → Deferred pension actually drawn: ₹6,249/month

- Widow Pension = 50% × ₹6,249 = ₹3,125/month

Deferral benefits flow through to widow pension as well — see Deferred EPS Pension After 58 for the complete deferral analysis.

Widow Pension at Different Member Service Levels

| Member’s Service | Member’s Pension | Widow Pension (50%) |

|---|---|---|

| 10 years | ₹2,143 | ₹1,072 |

| 15 years | ₹3,214 | ₹1,607 |

| 20 years | ₹4,714 | ₹2,357 |

| 25 years | ₹5,786 | ₹2,893 |

| 30 years | ₹6,857 | ₹3,429 |

| 33+ years (maximum) | ₹7,500 | ₹3,750 |

The Minimum Widow Pension Guarantee

EPFO guarantees a minimum widow pension of ₹1,000/month, regardless of how low the formula-based calculation works out to be. This floor is applied independently to the widow pension — it is not simply 50% of the member’s own ₹1,000 minimum pension floor, but a separate ₹1,000 minimum specifically for the widow benefit.

This ensures that even widows of members with very short service or low pensionable salary receive a meaningful guaranteed monthly income.

Duration of Widow Pension — When Does It Start and Stop?

When Widow Pension Starts

Widow pension is payable from the date of the member’s death (for death-in-service or pre-claim death cases) or from the date the widow files Form 10D (in cases of significant delay). See EPS Pension Arrears: Meaning and Calculation for the important distinction between processing-delay arrears and permanently-lost pre-claim periods — the same “file promptly” principle applies to widow pension claims.

When Widow Pension Stops

Event Effect Widow remarries Pension stops immediately — must be reported to EPFO Widow dies Pension stops; no further transfer (unless eligible children remain, who continue receiving child pension separately) No triggering event Pension continues for the widow’s entire lifetime

Important: There is no age limit on widow pension. A widow who was 28 years old when her husband died continues receiving pension for the rest of her life (or until remarriage), potentially for 50+ years.

The Remarriage Rule — What Widows Need to Know

If a widow receiving EPS widow pension remarries, the pension stops immediately from the date of remarriage. This is a strict, non-negotiable rule under EPS-95.

Obligations on Remarriage

- The widow is required to inform EPFO of her remarriage

- Continuing to draw widow pension after remarriage without disclosure is considered a violation and may result in recovery of wrongly paid amounts

- Child pension (if applicable) is not affected by the widow’s remarriage — children continue receiving their 25% share independently, up to age 25

No Reinstatement Provision

If a widow remarries and her pension stops, and the second marriage later ends (through death or divorce), EPS-95 does not currently provide for reinstatement of the original widow pension from the first husband’s EPS account.

Widow Pension and Multiple Marriages — Special Cases

In rare cases where a deceased member had more than one legally recognised spouse (where applicable under personal law), EPFO follows specific rules for apportioning the 50% widow pension among eligible widows — typically dividing the amount among them rather than paying the full 50% to each. Consult your regional EPFO office for these specific circumstances, as they involve case-by-case legal determinations.

How to Claim Widow Pension — Form 10D Process

Step 1 — Gather Required Documents

- Original or attested death certificate of the deceased member

- Marriage certificate establishing the relationship

- Widow’s own Aadhaar card

- Widow’s bank account details (account must be in her own name)

- Deceased member’s UAN, if available

Step 2 — File Form 10D

Widow pension is claimed via Form 10D, filed in the widow’s own name (not the deceased member’s name). For family pension claims, physical submission at the regional EPFO office is often required alongside the online application, particularly for document verification.

Step 3 — EPFO Verification

EPFO verifies the death certificate, marriage certificate, and the deceased member’s service records. This typically takes 15–30 working days for complete documentation.

Step 4 — PPO Issuance and First Payment

Once approved, a Pension Payment Order (PPO) is issued in the widow’s name, and monthly pension begins crediting to her bank account.

For the complete Form 10D filing process, see Form 10D Explained: How to Claim EPS Pension.

What If the Widow Was Not Aware of EPS Family Pension for Years?

There is no statutory time limit for claiming widow pension — a widow can file Form 10D even years after her husband’s death. However, consistent with the EPS arrears rules, pension is only payable from the date of filing, not retroactively to the date of death (in most cases where significant time has passed). The longer the delay in filing, the more lifetime pension income is permanently lost. Widows who discover this entitlement late should file immediately rather than further delaying.

Widow Pension Is Independent of EPF Corpus

A common point of confusion: widow pension (EPS) and the deceased member’s EPF corpus are completely separate benefits.

- EPF corpus: Paid as a one-time lump sum to the nominee (who may or may not be the widow, depending on nomination) via Form 20

- EPS widow pension: A separate, recurring monthly benefit paid specifically to the legal widow, regardless of EPF nomination details

A widow should claim both — the EPF lump sum (if she is the registered nominee, or as per succession rules if not) and the EPS widow pension (which goes to her by virtue of being the legal spouse, regardless of EPF nomination). See EPF vs EPS: Key Differences Explained for the complete distinction between the two funds.

Is Widow Pension Taxable?

Yes. Widow pension is taxable as “Income from Other Sources” under the Income Tax Act, added to the widow’s total income at her applicable slab rate. However, for most widow pension amounts (typically ₹1,000–₹3,750/month, or ₹12,000–₹45,000/year), this falls within or close to the basic exemption limit, meaning many widows pay little or no tax on this income alone.

Widow Pension — Quick Reference Summary

Aspect Detail Pension rate 50% of member’s pension Minimum service required None Minimum widow pension ₹1,000/month Duration Lifetime, or until remarriage Stops on Remarriage (immediate) Affected by member’s early pension? Yes — calculated on the reduced amount Affected by member’s deferred pension? Yes — calculated on the enhanced amount Claim form Form 10D (filed in widow’s name) Processing time 15–30 working days Taxable Yes, as income from other sources Independent of EPF corpus Yes — separate claim, separate benefit

Frequently Asked Questions — Widow Pension Under EPS

How much widow pension does a wife get under EPS?

The widow receives 50% of the deceased member’s monthly EPS pension, for life or until remarriage. Example: if the member’s pension was ₹5,786/month, the widow receives ₹2,893/month. The minimum guaranteed widow pension is ₹1,000/month.

Is there a minimum service requirement for widow pension?

No. Widow pension is payable regardless of how long the deceased member had worked — even 1 day of EPS-covered employment qualifies the widow for this benefit, subject to the ₹1,000/month minimum floor.

Does widow pension stop if I remarry?

Yes. Widow pension stops immediately upon remarriage. You are required to inform EPFO of your remarriage. There is no provision to reinstate the original widow pension even if the second marriage later ends.

Is there an age limit on widow pension?

No. Widow pension continues for the widow’s entire lifetime (or until remarriage), regardless of her age when the member died or her current age. A widow who was 25 when widowed continues receiving pension indefinitely.

How do I claim widow pension after my husband’s death?

File Form 10D in your own name at the regional EPFO office (or online where applicable), with the death certificate, marriage certificate, and your bank account details. Processing typically takes 15–30 working days. See Form 10D Explained.

If my husband claimed early pension before he died, does that affect my widow pension?

Yes. Widow pension is calculated as 50% of the pension the member was actually receiving — including any early pension reduction. If he claimed early pension at a 24% reduction, your widow pension is 50% of that reduced amount, not 50% of the original un-reduced base pension.

What is the widow pension if my husband died while still working (not yet retired)?

If the member dies while in active EPF-covered service, EPFO calculates a notional pension based on his actual service (with a 2-year minimum notional service if his actual service was shorter), using his salary at the time of death. The widow then receives 50% of this notional pension, subject to the ₹1,000/month minimum.

Can I get both EPF corpus and EPS widow pension?

Yes. They are completely independent benefits. EPF corpus is a one-time lump sum paid to the nominee via Form 20. EPS widow pension is a separate recurring monthly benefit paid to the legal widow. Claim both separately. See EPF vs EPS: Key Differences Explained.

Is widow pension under EPS taxable?

Yes, as “Income from Other Sources” at the widow’s applicable income tax slab rate. Most widow pension amounts fall within or near the basic exemption limit, meaning many widows owe little or no tax on this specific income.

What documents are needed to claim widow pension?

The deceased member’s death certificate, the marriage certificate establishing the relationship, the widow’s Aadhaar card, and her bank account details (in her own name). The deceased member’s UAN, if known, speeds up verification.

If my husband had deferred his pension to age 60 before passing away, do I get a higher widow pension?

Yes. Widow pension is calculated on the actual pension the member was receiving, including any deferred-pension enhancement. If he deferred to 60 and received an 8% enhanced pension, your widow pension is 50% of that enhanced amount — higher than if he had claimed at the standard age of 58.

Can I claim widow pension years after my husband’s death if I only just found out about it?

Yes — there is no statutory deadline to file. However, pension is generally payable only from the date you file Form 10D, not retroactively to the date of death (especially after significant delay). File as soon as possible to minimise permanently lost pension income.

What happens to widow pension if I have children who are also eligible for pension?

Widow pension (50%) and child pension (25% per child, up to 2 children) are paid simultaneously and independently. Your remarriage stops your own widow pension but does not affect your children’s ongoing child pension, which continues until each child turns 25.

Is there a difference in widow pension calculation for Higher Pension Scheme members?

Yes. If the deceased member was approved under the Higher Pension Scheme, the underlying member pension (used as the base for the 50% calculation) is based on actual salary rather than the ₹15,000 ceiling — resulting in a substantially higher widow pension. See EPS Higher Pension Scheme.

Where can I estimate what my widow pension would be?

Use the EPS Pension Calculator India on Wealthpedia to estimate the member’s pension based on service years and salary, then apply the 50% widow pension rate to that figure for an estimate of your entitlement.

Disclaimer: The information on this page is for educational purposes only and does not constitute investment or financial advice. Widow pension rules under EPS are governed by EPFO regulations under EPS-95 and may be updated by the Government of India. For personalised guidance, consult a SEBI-registered financial planner or visit your nearest EPFO office. Wealthpedia™ (Trademark Reg. No. 4910385) is not a SEBI-registered investment advisor. All mutual fund references on this site are for Direct Plan, Growth option only.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up