Millions of Indian employees contribute to EPS through their employer every month — yet most cannot answer a simple question: “Am I actually eligible for EPS pension?” The rules around eligibility are not complicated once explained clearly, but they are scattered across EPFO circulars and the EPS-95 scheme document in language that is difficult to parse.

This guide consolidates every EPS pension eligibility condition into one place — who qualifies, what the minimum requirements are, what happens in edge cases, and how the Higher Pension Scheme changes the eligibility picture.

Use the EPS Pension Calculator India to immediately check whether you qualify for monthly pension, early pension, or the Table D withdrawal benefit based on your service years and age.

Quick Summary

EPS pension eligibility in India is governed by four core conditions under EPS-95: you must be a member of an EPF-covered establishment, have completed a minimum of 10 years of EPS-covered service, have reached the eligible claim age (58 for standard pension, 50 for early pension), and not be in active EPF-covered employment at the time of drawing pension. Additional eligibility rules apply for the Higher Pension Scheme, family pension, invalidity pension, and the Table D withdrawal benefit for those with fewer than 10 years. This article explains every eligibility condition in full, with examples and exceptions. Use the EPS Pension Calculator India to check your personal eligibility instantly.

Join Now →

The Four Core Eligibility Conditions for EPS Monthly Pension

To receive a monthly EPS pension, all four of the following conditions must be satisfied simultaneously:

Condition 1 — EPS Membership

You must be (or have been) a member of the Employees’ Pension Scheme through an EPF-covered establishment. EPS membership is automatic for all employees who are enrolled in EPF and whose basic + DA is ₹15,000 or below at the time of joining. Employees earning above ₹15,000 at joining may be “excluded employees” but most still participate in EPS through their employer.

Condition 2 — Minimum 10 Years of Pensionable Service

You must have completed a minimum of 10 years of EPS-covered pensionable service. This is the most critical eligibility threshold in EPS.

- Service is counted in completed years (6+ months in final year rounds up; under 6 months is dropped)

- Service from multiple EPF-covered employers is cumulative, provided transfers were made via UAN

- Gaps in employment that were not covered by EPS do not count

- Only months in which EPS contributions were actually made count towards service

Condition 3 — Eligible Age

You must have attained one of the following ages: Pension Type Minimum Age Standard monthly pension 58 years Early monthly pension (reduced) 50 years Deferred pension (enhanced) 59–60 years

Condition 4 — Not in Active EPF-Covered Employment

You must not be employed in any EPF-covered establishment at the time of drawing pension. Employees who retire from one EPF-covered employer but immediately join another cannot draw EPS pension during the new employment period. On final cessation of EPF-covered employment, they can file for pension.

Who Is Eligible for EPS Membership?

EPS membership is mandatory for all employees who satisfy all of the following:

- Employed in an establishment covered under the EPF & Miscellaneous Provisions Act, 1952 (generally organisations with 20 or more employees in scheduled industries)

- Drawing a basic salary + DA of ₹15,000 or below at the time of joining the EPF-covered establishment

- Below the age of 58 years at the time of joining

Employees Above ₹15,000 Salary — Are They Eligible?

Employees whose basic + DA exceeds ₹15,000/month at the time of joining have the option to remain “excluded” from EPS — but most employers enrol all eligible employees in EPF, which includes EPS by default. Even for employees above ₹15,000, if they were enrolled before their salary crossed ₹15,000, they remain EPS members with a pensionable salary capped at ₹15,000.

Employees Who Are NOT Eligible for EPS

- Employees in establishments not covered under the EPF Act (typically fewer than 20 employees, or in excluded industries)

- Government employees covered under NPS or old government pension schemes

- Self-employed, freelancers, gig workers, and domestic workers

- Employees joining an EPF-covered establishment for the first time after age 58

- International workers covered under their home country’s social security (subject to bilateral SSA agreements)

Eligibility for Standard Monthly Pension (Age 58)

You are eligible for standard monthly EPS pension when:

- You have completed 10 or more years of EPS-covered service

- You have attained age 58

- You have ceased employment at all EPF-covered establishments

There is no upper age limit for claiming — you can file Form 10D at any point after turning 58 and having the required service. However, pension is paid only from the date of claim — there are no retroactive arrears beyond the date of retirement.

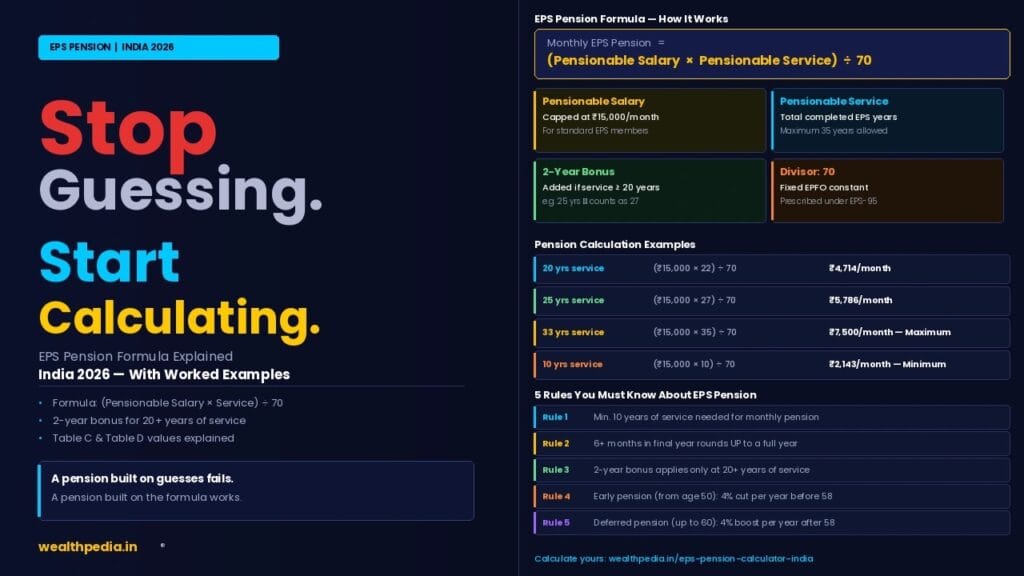

The formula that determines your pension amount:

Monthly Pension = (Pensionable Salary × Pensionable Service) ÷ 70

For a complete worked example, see EPS Pension Formula Explained.

Eligibility for Early Pension (Age 50–57)

You are eligible for early EPS pension when:

- You have completed 10 or more years of EPS-covered service

- You have attained age 50 (but not yet reached 58)

- You have ceased all EPF-covered employment

The early pension is permanently reduced by 4% for each year the claim is made before age 58. This is not a temporary reduction — it applies for the full duration of your pension lifetime.

Early pension is particularly relevant for:

- Employees who took Voluntary Retirement Scheme (VRS)

- Those who retired early for health reasons

- Employees whose employer shut down before they reached 58

For the full early pension reduction table and break-even analysis, see EPS Early Pension Before 58: Reduction Rules Explained.

Eligibility for Deferred Pension (Age 59–60)

You are eligible for deferred EPS pension when:

- You have completed 10 or more years of EPS-covered service

- You have attained age 59 or 60 (having not claimed at 58)

- You have ceased all EPF-covered employment

Deferring beyond 58 increases the pension by 4% per year, up to a maximum of age 60 (8% total increase). Beyond age 60, no further enhancement is available.

Full details and cash-flow comparison in Deferred EPS Pension After 58: Benefits Explained.

Eligibility for EPS Withdrawal Benefit (Table D) — Under 10 Years

If you have not yet completed 10 years of EPS-covered service, you are eligible for the Table D withdrawal benefit instead of monthly pension.

Conditions for Table D withdrawal eligibility:

- EPS service of at least 1 year (but less than 10 years)

- You have left the EPF-covered establishment

- A minimum 2-month waiting period has passed since the date of leaving

- You have not already claimed withdrawal benefit for this service period

- You are below age 58

The withdrawal benefit is calculated as: Table D Factor × Monthly Pensionable Salary (capped at ₹15,000). See EPS Withdrawal Benefit Calculator for the complete factor table and examples.

Alternative — Scheme Certificate

Instead of withdrawing, members with less than 10 years of service can apply for a Scheme Certificate, which preserves the EPS service for a future EPF-covered employer. This is often the better financial choice for those who plan to continue in organised employment. See Scheme Certificate vs EPS Withdrawal for a detailed comparison.

Eligibility for the 2-Year Service Bonus

You are eligible for the 2-year bonus addition to your pensionable service if your total EPS service is 20 years or more.

- 19 years service → no bonus — formula uses 19 years

- 20 years service → 2-year bonus — formula uses 22 years

- 25 years service → 2-year bonus — formula uses 27 years

- 33 years service → 2-year bonus — formula uses 35 years (maximum)

The 2-year bonus is a significant financial milestone — it adds a minimum of ₹429/month to the pension for life. For employees near the 19-year mark, pushing to 20 years is strongly advisable.

Eligibility for Higher Pension Scheme

The Higher Pension Scheme has specific eligibility conditions, separate from the standard EPS eligibility rules:

To have been eligible for the Higher Pension Scheme:

- The employee must have been an EPFO member before November 1, 2022

- The employer must have been contributing on the actual salary above ₹15,000 (not just on the ₹15,000 ceiling)

- A joint application by the employee and employer must have been submitted before the EPFO deadline

- The employee must deposit the contribution shortfall (the additional contribution that should have been made on the higher salary, with interest) as a lump sum to EPFO

The application window for the Higher Pension Scheme has closed. Members who have received EPFO approval use their actual 60-month average salary as pensionable salary — eliminating the ₹15,000 cap and dramatically increasing the monthly pension.

Full details, eligibility check, and pension calculation examples in EPS Higher Pension Scheme: Eligibility & Calculation.

Eligibility for Family Pension (Survivor Pension)

Family pension is available regardless of how many years of EPS service the member had completed — even a single day of EPS-covered employment qualifies the family.

Who Is Eligible as a Family Pension Beneficiary?

Widow or Widower:

- The legally married spouse of the deceased EPS member

- Pension continues for life or until remarriage

- Same-sex spouses and common-law partners are not currently recognised under EPS-95

Children:

- Legitimate children of the deceased member

- Up to a maximum of 2 children simultaneously

- Must be below age 25 at the time of claim

- Disabled children receive pension beyond age 25 — for life

Orphans:

- If both parents are deceased, children qualify for orphan pension (75% of member’s pension instead of child pension at 25%)

- Same age cap of 25 applies (except disabled children)

Dependent Parents:

- If no widow/widower and no eligible children, dependent parents of the deceased member may be eligible for a dependent parent pension

For the complete family pension rules with examples, see EPS Family Pension Rules Explained.

Eligibility for Invalidity Pension

An EPS member who suffers permanent and total disablement while in EPS-covered service is eligible for invalidity pension — with no minimum service requirement.

Conditions:

- The disablement must occur while in service (not after leaving employment)

- The disablement must be permanent and total — certified by a medical board

- The member must no longer be capable of the work they were employed for

The pension amount is calculated using the standard formula, but EPFO treats the member as having completed at least 2 years of pensionable service for calculation purposes. This ensures even very short-tenured members receive a meaningful invalidity pension.

Eligibility for Death-in-Service Pension

If an EPS member dies while in active service, the family qualifies for survivor pension regardless of service duration.

Even if the employee died on the first day of work, EPFO treats the case as if the member had completed a minimum pensionable service — ensuring the family receives a survivable pension. This is distinct from standard family pension (which requires the member to have reached retirement and claimed pension), though in practice both result in the same survivor benefit structure.

Eligibility Conditions — Edge Cases and Exceptions

Edge Case 1 — Service of 9 Years and 6+ Months

EPFO’s rounding rule: 6+ months in the final partial year rounds up to a full year. So 9 years and 6 months of service is counted as 10 years — crossing the pension eligibility threshold. This is the most important rounding edge case in EPS. See EPS Pension After 10 Years for the full analysis.

Edge Case 2 — Multiple Employers Without Transfer

If you worked for Employer A for 5 years without EPS transfer, then Employer B for 5 years, your total EPS service is 10 years — but only if the old service was preserved via a Scheme Certificate and submitted to Employer B. If neither a transfer nor a Scheme Certificate was obtained, the old 5-year service may be lost, leaving you with only 5 years from Employer B — below the 10-year minimum.

Edge Case 3 — Break in Service

A break in employment reduces EPS service by the gap period. EPFO may condone breaks of up to 2 years under certain conditions. Breaks beyond 2 years typically cannot be condoned — the service before and after the break is treated separately. If the pre-break service was less than 10 years and no Scheme Certificate was obtained, that period’s contribution to pension eligibility may be limited.

Edge Case 4 — Joining After Age 50

An employee who joins an EPF-covered establishment for the first time after age 50 but before 58 can still become an EPS member. However, completing 10 years of service before age 58 is impossible (maximum service would be less than 8 years). In this case:

- The employee would be eligible for Table D withdrawal benefit, not monthly pension

- Alternatively, if they had prior EPS service from an earlier employer (via Scheme Certificate), the combined service might cross 10 years

Edge Case 5 — Employees in Exempted Establishments

Some large organisations have EPFO-exempted provident fund trusts. Employees in these trusts are still covered under EPS — the EPS contribution flows to the central EPFO pool even when the EPF contribution stays in the private trust. Such employees follow the same EPS eligibility rules as any other member.

Edge Case 6 — International Workers (SSA Countries)

India has Social Security Agreements (SSAs) with several countries. International workers from SSA countries who work in India may be exempt from EPS contributions under the bilateral agreement. Such workers are not eligible for EPS pension in India — they are covered under their home country’s social security scheme.

EPS Pension Eligibility — Quick Reference Checklist

Use this checklist to assess your EPS pension eligibility:

| Question | Condition |

|---|---|

| Are you enrolled in EPF through your employer? | Must be Yes |

| Is your Basic + DA ₹15,000 or below at joining? | Must be Yes (or enrolled before salary exceeded ceiling) |

| Have you completed 10+ years of EPS service? | Must be Yes for monthly pension |

| Have you reached age 50? | Must be Yes for any pension claim |

| Have you ceased all EPF-covered employment? | Must be Yes at time of claim |

| Service from multiple employers transferred? | Must be Yes for cumulative count |

| Service below 10 years? | Table D withdrawal or Scheme Certificate |

| Service 10+ years but below age 50? | Preserve claim — file on reaching 50 |

| 20+ years of service? | 2-year bonus applies to pensionable service |

How to Verify Your EPS Eligibility

Step 1 — Check Your EPS Service on EPFO Passbook

Log in to passbook.epfindia.gov.in with your UAN. The EPS contribution column shows monthly credits. Count the months across all employment periods to determine total EPS service.

Step 2 — Verify Your Age

Ensure EPFO has your correct date of birth on record. If there is a discrepancy, get it corrected before filing — incorrect DOB can block pension claims. Use the EPFO portal under Member Details to check and correct DOB with Aadhaar.

Step 3 — Check for Service Transfers

If you worked for multiple employers, verify that all EPS service periods are showing under your UAN. Missing periods indicate a transfer was not completed — you may need to submit old Scheme Certificates or raise a grievance via EPFiGMS.

Step 4 — Compute Your Pension Amount

Use the EPS Pension Calculator India to enter your service details and salary and instantly compute your monthly pension amount, early pension options, and Table D withdrawal benefit if applicable.

Step 5 — File the Correct Form

- Monthly pension (10+ years, age 58): Form 10D online at EPFO UAN portal

- Early pension (10+ years, age 50–57): Form 10D (same form, different claim age selected)

- Withdrawal benefit (under 10 years): Form 10C (select Withdrawal Benefit)

- Scheme Certificate (under 10 years): Form 10C (select Scheme Certificate)

For complete filing guides, see Form 10D Explained and Form 10C Explained.

Frequently Asked Questions — EPS Pension Eligibility

What is the minimum service required to be eligible for EPS pension?

The minimum EPS-covered service required to qualify for a monthly pension is 10 years. Below 10 years, you receive a Table D withdrawal benefit or a Scheme Certificate. The 10-year count includes cumulative service across all EPF-covered employers, provided transfers were made correctly via UAN.

At what age can I claim EPS pension?

Standard pension: from age 58. Early pension (with 4% per year reduction): from age 50. Deferred pension (with 4% per year enhancement): from age 59 or 60. In all cases, you must have completed 10 years of EPS service and must not be in active EPF-covered employment.

Can I get EPS pension if I worked for multiple employers?

Yes — provided your EPS service was transferred between employers via UAN, the total cumulative service counts. If you left an employer without transferring EPS, you can still preserve that service by obtaining a Scheme Certificate and submitting it to your next employer. See Scheme Certificate vs EPS Withdrawal.

Is there an EPS pension for employees earning above ₹15,000?

Yes. Employees earning above ₹15,000 who are enrolled in EPS receive pension calculated on a pensionable salary capped at ₹15,000. Those who successfully applied for the Higher Pension Scheme receive pension on their actual salary. Employees who were never enrolled in EPS (excluded employees) are not eligible.

Am I eligible for EPS pension if I left my job at 45 after 15 years of service?

Yes — you qualify for monthly EPS pension since you have 15 years of service (above the 10-year minimum). However, you cannot claim the pension until you reach age 50 (for early pension with reduction) or 58 (for standard pension). Your pension amount is preserved from your exit date — it does not grow during the waiting period. See EPS Pension After 15 Years.

What is the EPS eligibility for family pension?

Family pension is available to the spouse and children of any deceased EPS member, regardless of how many years of service the member completed. Even 1 day of EPS-covered employment qualifies the family for survivor pension. Full details in EPS Family Pension Rules.

Can I get EPS pension if I worked for 9 years and 8 months?

Yes. EPFO’s rounding rule counts 8 months as rounding up to a full year — so 9 years and 8 months = 10 years of pensionable service. You qualify for monthly pension. This is one of the most important edge cases in EPS eligibility.

Is there EPS pension for contract workers?

It depends on the employment structure. Contract workers engaged through registered contractors may be covered under the principal employer’s EPF, which includes EPS. If EPF contributions were made on their behalf, they are EPS members. Pure gig or freelance workers with no EPF registration are not eligible.

What happens if my employer did not contribute to EPS?

If your employer failed to make EPS contributions, you may not have EPS service for those periods. However, if your employer registered you under EPF, EPFO can compel the employer to pay arrears. Raise a grievance via EPFiGMS at epfigms.gov.in if you believe contributions are missing.

Can I be eligible for both EPF withdrawal and EPS pension?

Yes. At retirement, you receive your full EPF corpus (via Form 19) and separately claim EPS monthly pension (via Form 10D). They are independent entitlements from separate funds — claiming one does not affect the other.

Am I eligible for EPS pension if I was an NRI working in India?

If you worked in an EPF-covered establishment in India and contributions were made to EPS on your behalf, you are eligible for EPS pension under the same rules as resident Indians. If you are from an SSA country, bilateral agreement provisions may affect your eligibility — check with EPFO.

What is the age eligibility for Higher Pension Scheme?

The Higher Pension Scheme eligibility is based on EPFO membership before November 1, 2022 — not on age. Members who were EPS contributors before this date and whose employer contributed on actual salary above ₹15,000 were eligible to apply. The application window has closed. See EPS Higher Pension Scheme.

Can I lose EPS pension eligibility after meeting the 10-year threshold?

Once you have completed 10 years of EPS service and attained the eligible age, your pension eligibility is secure — it cannot be taken away. However, if you re-join EPF-covered employment, you cannot draw pension during that period. On final retirement from all EPF employment, your full service (including the new period) is used for the pension calculation.

What if I have 8 years with one employer and 4 years with another?

Combined service = 12 years — well above the 10-year minimum — provided the EPS accounts were transferred between employers. If not transferred, you have separate spells of 8 years and 4 years, neither of which individually meets the 10-year threshold. Resolve this by submitting the Scheme Certificate from the first employer to the second employer (or raising a transfer request via the EPFO portal).

Is there any income or wealth eligibility criterion for EPS pension?

No. EPS pension eligibility is based purely on service years, age, and EPS membership — not on income, assets, or any means-test. Even if a member has substantial wealth or income from other sources, they receive full EPS pension without reduction.

Can a disabled child receive EPS family pension beyond age 25?

Yes. Disabled children of deceased EPS members are eligible for family pension beyond age 25 — for their lifetime. The disability must be documented and verified by EPFO. Standard (non-disabled) children receive family pension only up to age 25.

What is the eligibility for EPS invalidity pension?

An EPS member who suffers permanent and total disablement while in EPS-covered service is eligible for invalidity pension regardless of service duration. No minimum service is required. The disablement must be certified by a medical board and must occur during active service — not after leaving employment.

Do I need to be retired to claim EPS pension?

You must have ceased employment in all EPF-covered establishments to draw EPS pension. You do not need to formally “retire” — simply leaving all EPF-covered employment and reaching the eligible age qualifies you. Employees who left employment years before reaching 58 can file Form 10D as soon as they turn 58 (or 50 for early pension).

My EPS passbook shows zero contributions for some months. Does this affect eligibility?

Yes. Only months with actual EPS contributions count as pensionable service. Gaps in the EPS contribution column reduce your total service count. If the gap was due to employer non-compliance (e.g., employer failed to contribute), raise a grievance via EPFiGMS. If it was due to a break in employment, those months legitimately do not count.

Is there a deadline to claim EPS pension after turning 58?

There is no statutory deadline — you can file Form 10D at any time after turning 58 (and having the required service). However, pension is only credited from the date of claim, not retroactively to your 58th birthday or retirement date. Delay in filing means delay in receiving pension — there is no financial benefit to postponing beyond the desired claim age.

Can I claim EPS pension while still working part-time?

If the part-time work is in an EPF-covered establishment (registered employer with EPF), you cannot draw EPS pension during that employment. If the part-time work is self-employment, freelance, or in a non-EPF establishment, you can draw EPS pension simultaneously.

What if my UAN has multiple EPS service periods that are not linked?

If different employer service periods show under the same UAN, they should all be visible in your EPFO passbook. If some periods are missing or appear under a different UAN, use the EPFO portal to merge UANs or raise a grievance. All verified EPS service under your merged UAN counts toward the 10-year minimum.

Does the ₹15,000 wage ceiling affect eligibility or just the pension amount?

It affects only the pension amount — not eligibility. Whether your salary is ₹12,000 or ₹1,20,000, if you are an EPS member with 10+ years of service and the right age, you are eligible for monthly pension. The ₹15,000 ceiling only determines the pensionable salary used in the formula.

Am I eligible for EPS pension if my employer was in an exempted establishment (private PF trust)?

Yes. Even in exempted establishments with private PF trusts, the EPS contribution (8.33% capped at ₹1,250/month) goes to EPFO’s central pension pool — not the private trust. Your EPS eligibility and pension calculation follow the same standard EPS-95 rules.

Where can I verify my complete EPS eligibility based on my actual service and age?

Use the free EPS Pension Calculator India on Wealthpedia. Enter your date of birth, date of joining EPS, and expected retirement or exit date. The calculator checks your service against the 10-year minimum, applies the correct formula, and shows whether you qualify for monthly pension, early pension, or Table D withdrawal — along with the exact amounts.

Disclaimer: The information on this page is for educational purposes only and does not constitute investment or financial advice. EPS eligibility rules are governed by EPFO regulations under EPS-95 and may be updated by the Government of India. For personalised guidance, consult a SEBI-registered financial planner or visit your nearest EPFO office. Wealthpedia™ (Trademark Reg. No. 4910385) is not a SEBI-registered investment advisor. All mutual fund references on this site are for Direct Plan, Growth option only.

Vishal Jhaveri is the founder of Wealthpedia and an MBA Finance professional with over 10 years of experience in financial planning, investing, and wealth creation. He specializes in FIRE (Financial Independence, Retire Early), retirement planning, investing, and personal finance education. Through Wealthpedia, he develops financial calculators and publishes evidence-based content to help Indian investors make informed financial decisions. He regularly reviews and updates Wealthpedia articles to reflect changes in tax, laws, investment regulations, and personal finance best practices.

Quick Wrap up